“It has exerted its pull on the West for a thousand years.”

-Scott Anderson

That’s what Scott Anderson called the “lure of the East” in a fascinating new book I just started studying about the history of the Middle East called Lawrence in Arabia (2013).

“That lure brought wave after wave of Christian Crusaders to the Near East over a three-hundred year span in the Middle Ages. More recently, it brought a conquering French general with pharaonic fantasies named Napoleon… Europe’s greatest archaeologists in the 1830s… hordes of Western oil barons… and con men to the shores of the Caspian Sea in the 1870s.” (pg 15)

While 1,000 years is a long time, the lure of central planners clipping coins and/or devaluing the currency of The People has been in motion for at least 2x that. “In 64 A.D., in a naïve attempt to deceive the populace, Nero decreased the silver content in the coins and made silver and gold coins slightly smaller” (The History of Money, pg 52). Bernanke hopes no one has read that history.

Back to the Global Macro Grind…

What is it, precisely, that gave both the Roman and Ottoman Empires the audacity to plunder the purchasing power of their people? After 200 years of operating as an independent bank, what made the British Empire so soft that it felt it had to socialize (nationalize) the Bank of England in 1946? What was the US “Free-Market” Empire and why have we empowered the Fed to change it?

My apologies in advance for thinking this morning. If you disregard the vacuum of history in which Bernanke thinks (1930s) and contextualize the moment that his Fed is in (within the construct of long-term history which will ultimately judge Bernanke when he is long gone), it’s getting scary again. But you already know that – and the sad thing is that some of his Fed heads do too.

Yesterday, Dallas Fed Head (Fisher) basically admitted two things:

- The current White House Administration has politicized the US Federal Reserve

- By not doing what they led the market to believe what they’d do (taper), the Fed is losing credibility

Check. check.

I think most people who aren’t paid not to “get” it understand this now. If you don’t understand the history of un-elected politicians devaluing currencies, you have some reading to do. Self-education is the best long-term path to not becoming a lemming.

I’m not that smart. I think most people who have seen my SAT scores get that too. But Mr. Market is a very smart cookie, and what I tend to get (on a lag) is what he (or she) is telling me to get. I don’t wake up every morning trying to bend economic gravity.

Bernanke thinks he can “smooth” gravity, cycles, etc. He’s telling the entire bond, currency, and stock markets they are wrong. #Wow, bro. So let’s rewind the tapes and go to the score – what have markets done since Bernanke didn’t taper?

- US Dollar went straight down (now bearish TREND after being bullish for the better part of the last 9-10 months)

- US Interest Rates went straight down (still bullish TREND, but lost the immediate-term TRADE momentum line of 2.80% 10yr)

- US Growth Stocks stopped going up; slow-growth Utilities stopped going down

Now isn’t that last part perfect. Great job Ben. Instead of US growth expectations accelerating, now they are slowing again.

This is the first 2013 US stock market “correction” that I will not buy because Bernanke has decided that the opposite of what I want is what he wants. To review, what I want is A) what was happening and B) what every American should want:

1. #StrongDollar

2. #RatesRising

3. #GrowthAccelerating

To be fair, there are a lot of people who are in the business of slow-growth (Gold, Bond, MLP, etc.) investing who have a pre-determined path as to what they want (more money to manage). But that’s not what The People want.

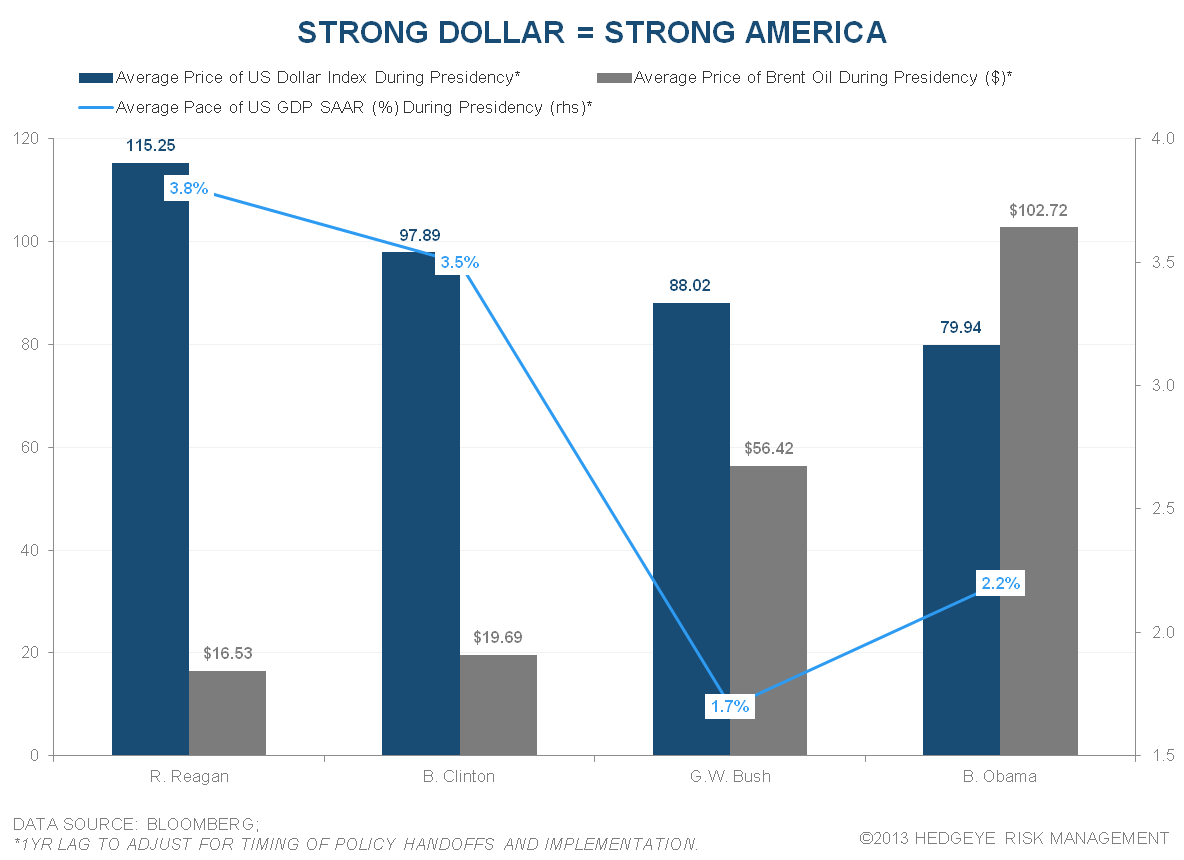

You don’t have to go back 2,000 years to get this either:

- 1983-89 US Growth > 4% GDP with #StrongDollar (Reagan’s avg = $115.25 USD) and Down Oil ($16.53/barrel avg)

- 1993-99 US Growth > 4% GDP with #StrongDollar (Clinton’s avg = $97.89 USD) and Down Oil ($19.69/barrel avg)

And maybe Hillary is smart enough to get what Obama doesn’t – and maybe that’s the only way out of this mess:

- Obama’s average USD (US Dollar Index) is the lowest in Presidential history at $79.52

- Obama’s average Oil price (Brent Oil) is the highest in Presidential history at $102.01/barrel

But that’s more than a few years away and sadly, at some point, someone in this country is going to realize that empowering both Putin and Middle Eastern kings via a Down Dollar, Up Oil policy is no different than doing the same via an un-elected Federal Reserve.

There is no doubt in my mind that the Fed is exerting its misplaced fear-mongering pull on the President. The lure is also to get you, The People, to fear the alternative (“if rates rise, housing will collapse”) when in reality it’s the government policy itself that is luring us away from the free-market system that gave America its empire to begin with.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.59-2.80%

SPX 1

VIX 12.93-14.98

USD 80.01-80.98

Euro 1.34-1.36

Brent 107.03-109.13

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer