This note was originally published September 17, 2013 at 16:43 in Consumer Staples

Last week we held an expert conference call titled, "Are Energy Drinks Harmful?" with Dr. Deborah Kennedy, a pediatric nutrition and expert on energy drinks.

Below are our main conclusions regarding regulatory concerns and evolution of the space based on Dr. Kennedy’s presentation and our own work. We also size up Monster Beverage Corp (MNST), which we’re bearish on from a quantitative perspective; however we remain bullish on the outperformance of energy drinks over the beverage category.

Key Considerations for the Industry

The FDA has left the door open for the amount of caffeine that energy drink (ED) manufacturers may put in their products. We do not see this stance changing over the near to intermediate term.

Why?

- The effects of caffeine are difficult to measure and are subjective to the consumer based on such factors as age, sex, weight, and existing medical conditions.

- There is no accepted standard for measuring caffeine.

- The FDA does not wish to open a pandora’s box until there’s more scientific evidence on caffeine: if energy drinks caffeine levels are regulated, what’s next, coffee? This is a can of worms that we do not believe will be addressed by the FDA over the intermediate term.

Longer Term Risks

- Over the longer-term, keep in mind that the FDA has put a limit on the amount of caffeine in soda drinks, 71mg. A similar limit could be placed on energy drinks over time. However, we expect the FDA to assess increased scientific studies on caffeine and energy drinks but ultimately be slow to act to issue a similar limit to soda drinks for energy drinks.

- As Dr. Kennedy suggested, we think there’s a higher probability that energy drinks are banned for sale to kids under 12 years of age.

- A ban on the marketing of energy drinks targeted at kids.

- We do not expect energy drinks to be move behind the counter.

MNST – Bearish Stock, Bullish Category

MNST is a stock that currently is set-up bearish across our quantitative intermediate term TREND price level of $57.56 (dancing below the level, up 3.5% since last Friday).

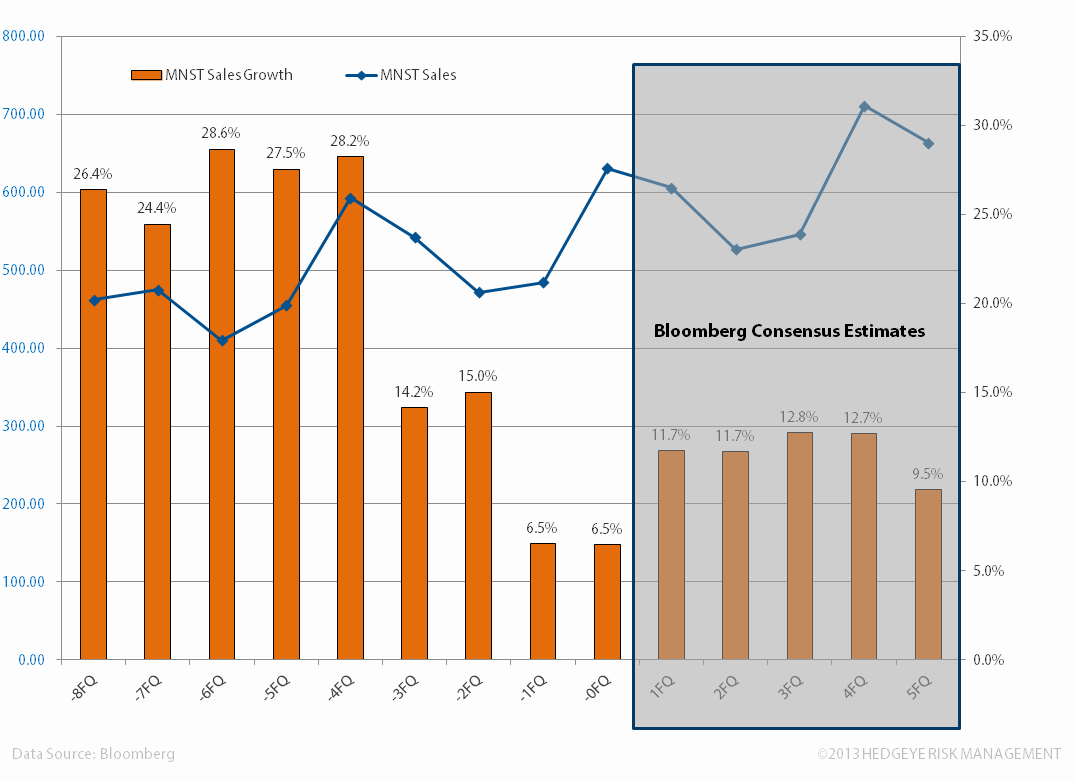

We continue to believe that energy drinks will maintain their outperformance over the beverage market. That said, MNST fundamentals have significantly eroded over the past 5 quarters. Below we show MNST’s top and bottom line Bloomberg consensus estimates for reference. We believe this slide in performance is attributable to both weak overall beverage trends, including poor weather conditions across recent quarterly results, and litigation concerns. On the last point, we think that the existing litigation is now largely behind the company, as are the associated media headlines, which should buoy sentiment. Our call with energy drink expert Dr. Kennedy only furthered our opinion that despite health concerns related to energy drinks, the FDA is not in a position to act over the near to intermediate term on caffeine content for the reasons we highlighted above. Finally on a comp basis, you’ll notice much more favorable comparisons over the next four quarters, which could prove a tailwind. We’ll be watching our quantitative levels to see if MNST can overcome its bearish intermediate term set-up before we consider it on the long side.

-Matt Hedrick