INVESTING IDEAS

Here are the latest comments from Hedgeye Sector Heads on their high-conviction stock ideas.

BNNY - Consumer Staples analyst Matthew Hedrick reiterates his positive outlook and expectations for Annies. Hedrick believes BNNY’s premium valuation is justified by higher growth rates across organic offerings, of which Annie’s is a leader, especially as it increasingly moves its products to the mainstream aisle from the organic aisle. BNNY caters to a higher income demographic that Hedrick says should continue to pay a premium for organic foods despite fluctuations in macroeconomic conditions.

Hedrick says BNNY’s strategy to innovate everyday foods and create healthier and better tasting options should sustain long-term growth, and Hedrick looks for BNNY to maintain its market leadership and gain share as it moves more of its items to the center of the store.

FDX - Hedgeye Industrials Sector Head Jay Van Sciver remains positive on the long-term potential for shares of FDX. According to Jay, “We think it is fair to say that the FedEx report on Wednesday exceeded muted expectations and added credibility to the Express restructuring program."

He adds, “FedEx continues to show that it can deliver higher Express margins and, as it does, the market should move to price in continued success. We continue to think that there is significant potential value at FedEx Express that the market is not pricing in. We would look for weakness to buy.”

Bottom line according to Van Sciver is he continues to think that FDX will prove a rewarding long-term position, as FedEx Express focuses on profitability instead of market share. FedEx is also well positioned to benefit from signs of stronger economic growth.

HCA – Hedgeye Healthcare Sector Head Tom Tobin says there are mounting fears over a government shutdown as Republicans want to defund Obamacare. In the event this does occur, Tobin sees it as a net negative to HCA Corp. since the hospital operator will not see the bad-debt relief due to less uninsured patients from Obamacare.

However, Tobin believes a government shutdown is highly unlikely for any extended period of time, and believe the HCA’s fundamentals remain intact into 2014

MD – Healthcare Sector Head Tom Tobin’s proprietary OB/GYN Tracking Survey suggests utilization trends may be slowing for Mednax in 3Q, which is concerning given the run-up in the stock lately.

However, MD has two additional growth drivers that should compensate for any softness in volume. The first is Medicaid parity, which should help drive accelerating pricing growth through at least 1Q14. The second is acquisitions, which currently have been slow to ramp through 2013, but is likely to pick up through the remainder of the year.

HOLX – Healthcare Sector Head Tom Tobin has no update on Hologic this week.

NKE – According to Retail Sector Head Brian McGough, this week, the biggest item on Nike has nothing to do with Nike whatsoever. Specifically, Adidas, Nike’s top competitor as measured by size, market share and global diversification, updated guidance for the quarter and the year following an Executive Board meeting. The announcement was simply horrible. The details are as follows…

- “Firstly, the further weakening of several currencies versus the euro throughout August and September such as the Russian rouble, Japanese yen, Brazilian real, Argentine peso, Turkish lira and Australian dollar have intensified the negative currency translation headwinds already highlighted by management during the course of the year.

- This is estimated to lead to a high-single-digit percentage point negative translation impact in Q3.

- Secondly, an unexpected short-term distribution constraint as a result of the transition to the adidas Group's new distribution facility in Chekhov, close to Moscow, is impacting the quantity of new product flow to stores.

- While the problem is expected to be resolved at the beginning of Q4, this, together with the weakness of the Russian rouble, means that the group's 2013 goals for Russia/CIS are no longer attainable.

- Finally, the continued softness in the global golf market and TaylorMade-adidas Golf's focus on maintaining healthy inventory levels in the marketplace will lead to a lower sales and profit contribution from the segment than originally forecasted.

- Taking all of these issues into account, management now expects:

- a low-single-digit currency-neutral sales increase vs prior guidance for a low- to mid-single digit increase

- an operating margin of around 8.5% vs prior guidance of "approaching 9.0%"

- net income attributable to shareholders to increase at a mid-single-digit rate to a level of €820-850M vs prior guidance €890-920M and FactSet €910M.

- In terms of phasing, a significant portion of the negative impact will be in Q3, with management continuing to expect a strong rebound in sales and profitability growth in Q4.”

The reality is that this simply does not happen at Nike. Investors often compare the two – especially in Europe – but when we see announcements like this we think it further polarizes the divide between the two companies.

NSM- Financials Sector Head Josh Steiner says that Nationstar Mortgage continues to benefit from new positive initiations of coverage from the sell side, as well as ratings upgrades from existing coverage. In fact, there have been 3 positive initiations/upgrades since just September 10th.

While this has been beneficial, we’re beginning to feel like NSM is getting closer to becoming a consensus long idea. For now, we’re still bullish in the short term as we expect the company to announce some new business wins in the form of servicing portfolio purchases. That said, with the move the stock has had and with the pressure we’re seeing elsewhere on the mortgage originations front, we’ll be keeping the NSM long idea on a shorter leash from here.

TRADE: In the short-term, we think the market will be watching for the next sizeable MSR sale.

TREND: Over the intermediate term, the stock will key off 3Q13 earnings results, deal announcements and the direction of long-term interest rates.

TAIL: In the long-term, there is still a tremendous opportunity for non-bank servicers like Nationstar to roll-up the servicing business. NSM is well positioned to be a prime beneficiary.

RH - Here’s the Hedgeye Retail ‘Visual of the Week’. We can promise that it will scare most people who see it.

What you see above is a picture of a recording artist named Edei. That’s not the scary part. The eyebrow-raiser is the massive backdrop showing that she was performing under the label RH Music.

This concert was in New York at the Highline Ballroom and was part of the RH Music private concert where it showcased its initial artists under its label. If RH starts a new kitchen business (which it is), people won’t question it for a minute. If they start an antiques and collectibles business (which they have), people will give RH a free pass.

But Music??? Seriously???

We were initially surprised by this move, but we think that people need to look at it not as an effort to gain revenue in the category as much as a way RH is redeploying marketing dollars away from traditional media (no more mailing out an 8 lb catalogue) in order to broaden out its customer base into a younger demographic. Wall Street is not used to this yet…but we think that the company will give people reason to believe.

SBUX – Hedgeye Sector head Howard Penney says Starbucks is the best growth stock in the restaurant space that he covers. He likes Starbucks on both an intermediate-term TREND and a long-term TAIL basis.

On a TREND basis, Penney says the company will show above-trend revenue growth, due in large part to U.S. and international growth as well as ongoing expansion in the Consumer Products Group (CPG). CPG refers to Starbucks’ business of selling products through grocery stores and warehouse clubs, in addition to selling other branded SBUX products worldwide.

On a TAIL basis, Penney says that Starbucks will achieve impressive long-term growth as long as it continues to focus on its core business. Moving forward, Penney sees vast opportunities for the company to expand through various channels and geographies.”

TROW - With asset management giant Blackrock (nearly $4 trillion in client assets) signaling a rotation from bonds into equities in an update this week, there’s no better time to invest in a leading equity manager who will benefit from incremental stock flows, according to Jonathan Casteleyn, Director of Financials Research.

T Rowe Price has the best investment performance in the equity business and should continue to outflank the investment management industry in generating the highest new client inflow says Casteleyn.

In addition, T Rowe’s client assets which are 70% stock based also have the opportunity to appreciate along with equity markets which increases TROW’s billable fees, an important attribute with the ongoing effort of quantitative easing by the U.S. central bank which has historically boosted stock values.

WWW - Wolverine is quiet on the news front. It just finished up a European Investor Relations tour and topped it off with a sell-side conference. And with the quarter closing in less than two weeks its quiet period is just about to begin.

The company reports EPS in the first half of October, where we’re coming in at $1.20 vs. the Street at $1.02. It goes without saying that we think it will have a great quarter. To keep the hype going, WWW is hosting an analyst day in NYC on October 15th.

Needless to say, we think that the catalyst calendar is lining up nicely.

Editor's note: In light of the Fed's surprising decision not to taper earlier this week, we would like to republish Hedgeye Founder and CEO Keith McCullough's "Morning Newsletter" from Friday morning. As Keith points out, there are major market and economic implications from this decision. Incidentally, as we're sure you know by now, Keith is no shrinking violet. His note below is no exception. For more information on how you can subscribe to Keith's Morning Newsletter, please click here.

09/20/13 07:55 AM EDT

Buffet's Fed

“The Fed is the greatest hedge fund in history.”-Warren Buffett

The Big Picture

That’s what Buffett told students at Georgetown University yesterday. He was trumpeting “how much money” the Fed makes: “it’s generating $80 billion or $90 billion a year probably… and that wasn’t the case a few years back.”

Now isn’t that just fantastic. One of the greatest financial minds in US history is now marketing a political message that is about as anti Benjamin Franklin as it gets. Anti-savings that is. Where in God’s good name do you think these said “profits” come from?

They come out of American savings accounts. Even the Fed itself (St. Louis Fed) reminds us that the “growth rate of real GDP has been higher on average when the personal savings rate is rising than when it is falling (Gilder, pg 72).” The Founding Fathers wanted our children to respect their piggy banks, not some un-elected money printer clipping our hard earned coins.

Macro Grind

As George Gilder goes on to absolutely nail this topic in his new book, Knowledge and Power, “the entrepreneur is the savior of the system because he capitalizes himself. He is his own most important capital… socialists believe their mission is to seize capital for the masses…” (Gilder, pg 77)

That’s what Mr. Buffett should be marketing. It’s time to get our money out of the Fed’s hands and back into the hands of The People. We know how to generate returns. We’re the ones who are going to be doing the hiring when we make money. All the Fed’s “profits” do at this point is tax the American consumer. It’s called Down Dollar driven inflation. It’s regressive.

Moving on… where the rubber meets the road here is in terms of the purchasing power of your hard earned currency. While I was disgusted with Bernanke’s decision to debauch the Dollar again this week, that doesn’t mean he’s going to win this war for good. In the last 24 hours, both the data (economic gravity) and Mr. Market are fighting back:

- US Dollar Index is up +0.2% this morning to $80.41 (holding long-term TAIL risk support of $79.11)

- Gold and Silver are down -1% and -2.4%, respectively (both are still bearish TREND and TAIL in our model)

- Oil (Brent) failed to breakout above our immediate-term TRADE resistance line of $110.94/barrel

Economic data? Yes, as in the stuff Bernanke has un-objectively ignored since almost every high-frequency US economic data series we follow started to accelerated in July.

- JOBS: non-seasonally adjusted rolling US Jobless claims hit yet another YTD low (-16.4% y/y) yesterday!

- ORDERS: the Philly Fed’s “New Order” component ripped a +21 SEP vs +5 in AUG

- HOUSING: US Existing Home Sales hit a 6-month high yesterday

Now most Fed apologists (which are mostly those who get paid by A) Government Power and/or B) Down Dollar) will whine about the impact of #RatesRising on the “housing’s recovery” instead of focusing on what really drives housing demand – confidence.

Although US Savings are at generational lows, US Net Worth is currently tracking at an all-time high. We’d argue that’s been largely driven by real (inflation adjusted) #GrowthAccelerating more so than anything else. US Home Prices up +12.4% y/y obviously helps, but the demand for housing won’t be impacted until the 30-yr mortgage rate blows through 6% (it’s at 3.79% today, get over it).

In other words, the greatest threat to US growth recovering is the government intervening in the economic cycle. There has never been a sustained US economic recovery that didn’t coincide with:

1. Strengthening US Dollar

2. Rising US Interest Rates

Why doesn’t every discussion about the Fed start and end with that?

While Buffett might love the impact Bernanke has on his P&L (fat net interest margins are driven by marking the short-end of the curve at 0% - that pays insurance companies (Berkshire) in size), I’d like to remind him that the “greatest hedge fund manager in history” is also the only un-elected central planner in US history to attempt to ban the economic cycle.

What is an economic cycle?

$USD/Interest Rates Higher --> Energy/Commodities/Inflation lower --> Real Consumption Growth Higher --> Pro-Growth Equities Higher

With all due respect Mr. Buffett, why don’t you and your pal, Mr. President, want the rest of us “middle classers” to have that?

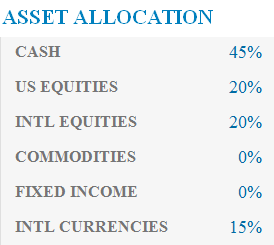

Sadly, there are very few leaders in Washington who have my back on this. That’s one of the reasons why I have the highest CASH position in the Hedgeye Asset Allocation Model since July 23rd. I don’t trust this rally to all-time highs anymore.

The biggest thing Bernanke lost this week was whatever was left of the trust I had in someone at the Fed doing the right thing. The timing was perfect. And he chose politics instead. If growth slows from here, Gold help him. Because history won’t.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer