"Everything has its limit - iron ore cannot be educated into gold." -Mark Twain

"We turned at a dozen paces, for love is a dual, and looked at each other for the last time." -Jack Kerouac, On the Road

Keith and I were on the road this week and had some of the most interesting conversation we've had since I joined the firm nine months ago and we started accepting macro clients. Two key areas of discussion were the US Dollar and interest rates. On the former, the discussion centered around whether this "dollar crisis", as we are calling it, is really anything more than a trade into more risky assets globally. That is, investors are just selling the safe haven US dollar and shifting into riskier asset classes like emerging market and small capitalization equities.

The second debate centered around the next move of the Federal Reserve. The most contrarian point we heard was that the Fed may not raise rates for more than a year and a half from now.

As in the Mark Twain quote above, everything has its limits, even the US dollar. With the US dollar down dramatically in the last 3-months and the U.S. stock market one of the worst performing global equity indexes, the facts clearly suggest that what is going on globally is a vote against the U.S. economic system. That statement may sound unpatriotic, but it is simply a fact.

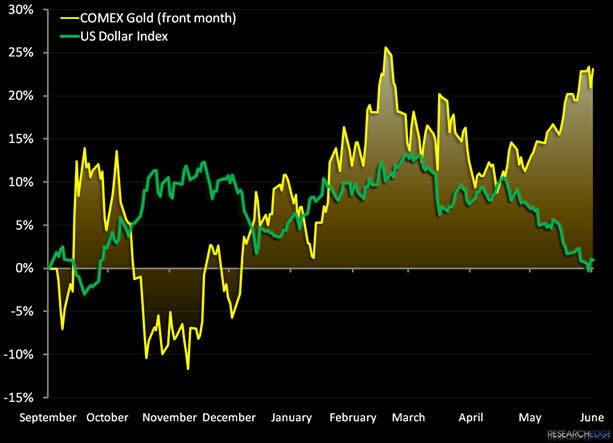

While we have seen the appetite for risk assets increase over the past couple months, it is difficult to attribute the decline in the U.S. dollar to this asset shift. There is clearly something else going on as investors have been buying gold in that period as we outline in the chart below, which is considers a safe haven in periods of heightened risk. In fact, global political rhetoric is almost as much evidence as we need to convince ourselves this is not the case. Over the past few days, there have been some public statements by Russian President Dmitry Medvedev, in particular, which highlight this point. His quotes are below:

"The dollar is not in a spectacular position, let's be frank, and its prospects cause various questions as do the prospects for the global currency system.''

And as it relates to a new global currency Medvedev said:

"This idea has potential, even though some of my G-20 colleagues aren't actively discussing it at the moment. However, for example, in the opinion of our Chinese colleagues it is quite a possible step. The most important thing is not to walk away from discussions on this topic.''

In the last statement, Medvedev is obviously appealing to The Client (China), who have voiced similar concerns as recently as this week with Treasury Secretary Geithner's visit to China. Over the past 9 - 12 months this call by the Chinese has been getting louder and louder. In a April 17th note entitled, "Is China Advocating for the Bancor?", we quoted Dr. Zhou Ziaochuan, a primary player in determining Chinese fiscal policy, who wrote the following in an essay:

"Though the super-sovereign reserve currency has long since been proposed, yet no substantive progress has been achieved to date. Back in the 1940s, Keynes had already proposed to introduce an international currency unit named "Bancor", based on the value of 30 representative commodities. Unfortunately, the proposal was not accepted. (Emphasis is Research Edge's.)"

We can theorize about why the dollar is crashing and whether it is a crisis or not, but I don't think any of us can ignore the drum beat of the people that are buying US dollars and Treasuries. A key catalyst in this political rhetoric will occur on June 16th, when Russia meets with Brazil, India, and China in the Russian city of Yekaterinburg, which is in the Ural Mountains. The Russians and Chinese have already played their cards and they will only turn up the volume on the rhetoric during and post this conference and encouraging their Indian and Brazilian "colleagues" to do the same.

Jack Kerouac, who is of course the famous beatnik author, wrote the line at the start of this note in his novel, On the Road; likely he did not intend that quote to be used as a euphemism for the global currency markets, but the quote is an apt description as any of the global currency dual that is going on. To consider this merely a shift to a higher risk assets, would be very shortsighted indeed.

We make our calls based on the facts in front of us and don't have a specific view on when rates will increase, but ultimately if the voices from abroad continue their heightened anti-dollar rhetoric this will also become a political issue in the U.S. Clearly, in the short term anyways, one of the quickest ways to strengthen the U.S. dollar is for the Fed to raise rates. To some extent, their hand will likely be forced on the inflation front in that regard as well. That is, if the U.S. dollar continues to break down, reflation will turn into inflation, and the Fed will start raising rates. As the yield curve is signaling (outlined in the chart below), this could happen much sooner than many equity investors expect. After all, as most global macro fundamental analysts already know, bond markets are not lagging indicators.

Daryl G. Jones

Managing Director