Yesterday we hosted an expert conference call titled "Are Energy Drinks Harmful?" with Dr. Deborah Kennedy, a pediatric nutrition and expert on energy drinks. The call was very comprehensive and well received by our clients. If you missed the it, here are links to the podcast replay and presentation. We encourage you to take the time (one hour in length including a Q&A session) to listen to the call, and have included a summary of the call below.

Note: We will be putting out a subsequent post with our outlook on the energy drink space, in particular on Monster (MNST), and giving consideration to key take-aways from Dr. Kennedy’s presentation on the industry.

-Matt Hedrick

---

What are Energy Drinks?

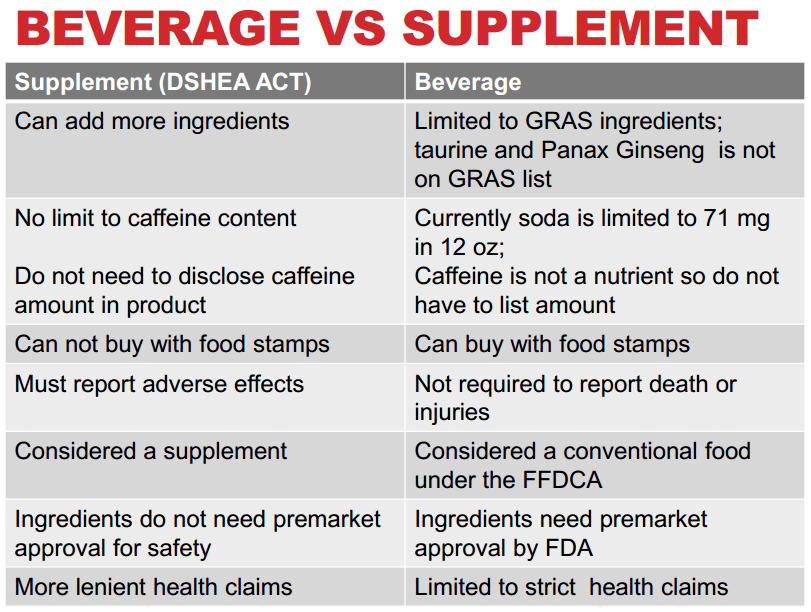

- There is no legal definition, manufacturers came up with term. FDA has not defined parameters of what may be in an energy drink.

- What can be added? Depends if labeled as a Beverage or a Supplement.

- Under the beverage label (note: all the major energy drink makers are considered a beverage, whereas only energy shots are a supplement) caffeine is considered GRAS (Generally Regarded as Safe); and under the supplement label there’s no limits to caffeine content. Therefore, manufacturers can put as much caffeine in the product as they choose and the onus is on them to determine the product’s safety.

- For ingredients other than caffeine, if a supplement: onus is on manufacturer to decide. If a beverage, need preapproval of ingredients or need to contain GRAS elements.

- Under the Food and Drug Cosmetic Act, neither a supplement nor a beverage is legally required to list the caffeine content on its products.

- When caffeine passed as a GRAS ingredient, there was a recognition of the need to put limits on the caffeine content in drinks, and the FDA decided to limit the amount of caffeine in soda to 71 mg in a can of soda (12oz.). No limits have since been put on energy drinks.

- For Beverage, what you put in the product has to be on the ingredient list, but because caffeine is not considered a nutrient by the FDA (it is considered a food and drug), caffeine does not have to be on the nutrient fact panel.

- If Beverage, can buy with food stamps. If Beverage, do not need to report if anyone dies from consumption of the product, however deaths must be reported if labeled a supplement.

- Energy drinks have been around since 1901 but only in significant quantities since 2007

- Red Bull came to the U.S .in 1997 – major forerunner in energy drink industry, then Rockstar (2001), Monster (2002); and 5-Hour Energy Shots (2004).

- 66% of energy drink consumers are between the age of 13-35 (65% of consumers are male)

- Sales of energy drinks have surpassed that of fruit and sports in U.S.

About Caffeine?

- Known to increase heart rate, blood pressure, speech rate, and motor activity

- Concern for children: unclear what impact caffeine can have on neurological and cardiovascular systems

- U.S. Avg person gets 250-300mg of caffeine per day. Moderate consumption = 1-2 cups of coffee a day (approx. 260mg caffeine). Heavy consumption = 5 cups a day (~ 500mg).

- Teens should limit to under 100mg/day. < 13 years of age = none to less than 50mg/day.

- Ability to handle caffeine varies from persons to person, including how liver metabolizes caffeine, and tolerance. Children and elderly are at greater risk for adverse events, and males are more susceptible than females for adverse events.

How much Caffeine in Energy Drinks?

- Avg 80mg/8oz., but serving sizes vary and caffeine range is wide across offerings

- Compared to Coffee? How much caffeine is in coffee depends on how strong coffee is brewed. Generic Brewed Coffee 95 -200mg per 8oz. (for reference: 12oz. Coca Cola = 30-35mg)

- Believes that media has convinced consumers that all they need to pay attention to is the amount of caffeine. (Comparing Starbucks coffee to energy drinks is false advertising. Apples to oranges. In energy drinks you can have other substances besides caffeine, that may not be counted that contribute to the total level of caffeine.

Dangers and What Experts are Saying

- Retailers are not prohibited legally from selling energy drinks to kids.

- Case of adverse affects are being reported: With Red Bull, shortness of breath, anxiety, chest pain, heart attack, convulsions, mental impairment. With Monster, 4 heart attacks, 5 deaths, chest pain, tremor, anxiety, psychotic disorder.

- Dr. Kennedy questions how we can live in a society where such products that cause these adverse affects are not pulled off the shelf. Suggests if this were an OTC drug, with similar results to consumers, that drug would be pulled off the market immediately.

- Of the 5,448 U.S. caffeine overdoses reported in 2007, 46% occurred in those younger than 19 years.

- Dr. Kennedy hopes energy drinks are put behind the counter.

- American Academy of Pediatrics says energy drinks should not be consumed or sold to kids.

Dr. Kennedy Predictions

- Dr. Kenned believes manufacturers will never give up the teen and tween market, but will give up the market <12.

- Energy drink makers say they are not marketing to this demographic (kids), but believes the events at which the manufacturers market is tells a completely opposite story.

- Thinks the FDA will look at the idea of calling caffeine GRAS (Generally Recognized as Safe) and will provide more regulation in terms of amounts allowed.

- Thinks like cigarette companies, who got caught marketing to kids, and later confess to it, energy drink manufacturers will run a similar course.

Q&A Highlights

Q) What ingredient recommendations have been made or given to the energy drink makers from doctors and/or the FDA?

A) Nothing yet. A doctor can say whatever he or she wants but the manufacturers are not listening. Now some Senators are involved and they’re asking the energy drink manufacturers to playing nice and stop marketing to kids, but until the FDA comes down on limits to caffeine levels nothing will change.

Q) Do you foresee that the FDA could pass a standard for caffeine in drinks?

A) Yes, although technically it gets complicated because of molecular differences across caffeine types. So it will take awhile to get to any standard.

Q) With respect to the cross over between age regulations for energy drinks and coffee, would you promote that a 16 year old walking into a Starbucks can’t order a grande redeye coffee drink, or needs to show identification to purchase it?

A) For a teen there needs to be a warning label on anything over 100mg of caffeine. Similar to calorie counts on food menus, the consumers need to have information so that they can make a reasonable choice. The consumer should know which beverages are over 100mg of caffeine and could potentially cause toxicity. Not looking to card minors, rather given teens the ability to make their own choices.

Q) Would you like to see the energy drink makers come up with one size of energy drink with one level of caffeine?

A) I would like to see what happened to soda. Those companies are set to a certain standard so that you know exactly what you’re buying. So yes, I agree the same should be the standard for energy drinks.