This note was originally published at 8am on August 28, 2013 for Hedgeye subscribers.

“The noise can be deafening.”

-George Gilder

When he wrote that in Knowledge and Power, Gilder was referring to government interference (in markets). He also went on to make the critical, but often overlooked, behavioral link between simple market signals (like interest rates) and central planning noise.

“Interest rates are critical for information-theory economic analysis because they are an index of real economic conditions. If the government manipulates them, they will issue false signals, breeding confusion that undermines entrepreneurial activity.” (pg 24)

That pretty much sums up what I think all of us are struggling with today. Inclusive of yesterday’s drop in interest rates (oil ripping new highs is an economic headwind), the bond market is becoming as good a leading indicator of the slope of US economic growth’s TREND as anything I can back-test. At the same time, we have to deal with the deafening impact of central planning commentary.

Back to the Global Macro Grind…

Yesterday’s 1-day drop in the US stock market was deafening too. It came on a legitimate Information Surprise (Oil ripping on Syria) and the rotation you’d expect to see when expectations for growth fall (bond yields and US growth stocks have a positive correlation).

How did that deafening drop (there was no volume) fair within the context of the Top 3 biggest 1-day drops since April?

- June 20th, 2013 = SP500 -2.5%

- April 15th,2013 = SP500 -2.3%

- August 28th,2013 = SP500 -1.6%

#EOW (end of world) type stuff, I know.

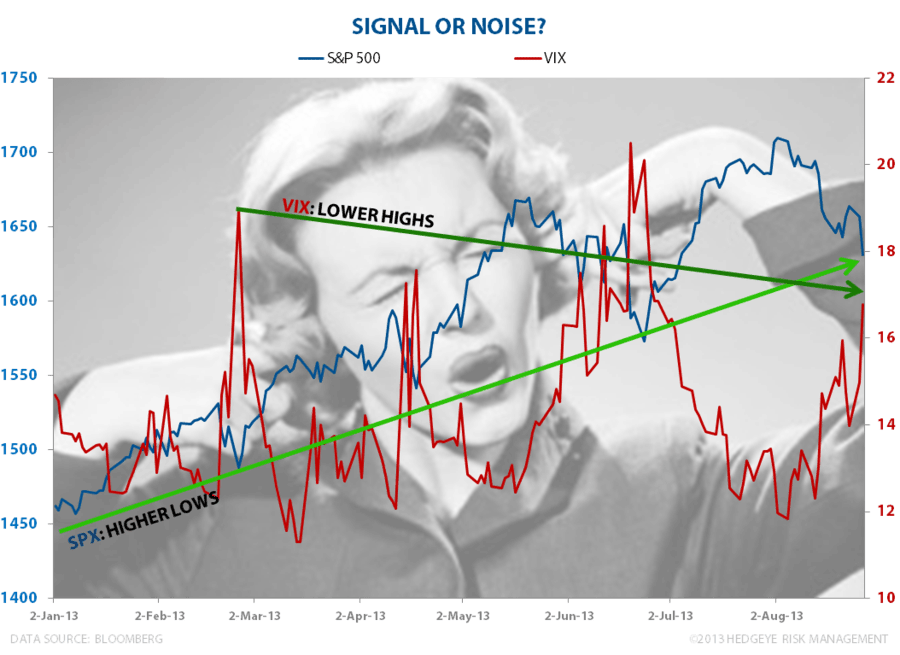

In both of the prior 1-day freak-outs (which were bigger in terms of both magnitude and volume), fear spiked (front-month VIX) to higher levels than what you saw yesterday too. In other words:

- US stocks keep making higher intermediate-term TREND lows

- US Equity Volatility keeps making lower intermediate-term TREND highs

That’s why we do the multi-duration risk management thing. How else are you going to contextualize the immediate-term TRADE noise of Mr. Market if you don’t have anything to signal the intermediate-term TREND?

Since we are raging bears on Emerging Market Equities (EEM), this morning’s discussion is more focused on how to interpret US market noise (US markets include big stuff like the currency and bond market). Here are the other two Big Macro Signals I care about most:

- US Dollar Index grinded out another higher-low (versus the recent FEB and JUN lows) and held long-term TAIL support

- US 10yr Treasury Yield (2.73% this morning) held both TRADE (2.69%) and TREND (2.44%) levels of support = higher-lows

And yes, the TREND is your less noisy friend, until he/she isn’t – I get that. I also get that Oil prices steadily rising from here could cut US consumption growth in half, sequentially. So there’s a lot to think about (including whether this will be the YTD high in oil altogether).

But while I think, I have to try hard to take the emotion out of the decisions I make on what to do next. That’s why my immediate-term TRADE signals determine my short-term risk management decisions. I’ve tried the feel thing – and it ends up not feeling good.

When running money in a bull market like this for US growth stocks, not selling the lows is one of the most important decisions you can make. What if you read Zero Hedge, capitulated to your emotional state, and sold the April 15th and/or June 20th lows?

- By April 18th (3days later), the SP500 locked in another higher-YTD-low of 1541

- By June 24th (3days later), the SP500 locked in another higher-YTD-low of 1573

Can you wait 3 more days to see if this noise settles? Or are we all high-frequency blog freaks now? By August 2nd 2013 (when the SP500 hit its all-time closing high of 1709) you’d have been up +11% and/or +8.6% in SPY, respectively. Just saying.

Maybe the world is going to end this time. I started making that call around this time in 2007 (and it almost did end). But this is not 2007, and not one of the people and/or risk management processes that called it last time is making that call this time either.

Maybe everyone who didn’t call the 2007 topping process is going to nail it this time. But maybe not. All I can tell you is that the noise of #PTCs (professional top callers) since April of 2013 has been deafening.

Our immediate-term Risk Ranges are now as follows:

UST 10yr Yield 2.70-2.93%

SPX 1621-1666

EEM (Emerging Markets) 36.91-38.49

VIX 15.05-18.98

USD 80.91-81.73

Brent 110.69-115.98

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer