TODAY’S S&P 500 SET-UP – September 11, 2013

As we look at today's setup for the S&P 500, the range is 32 points or 1.37% downside to 1661 and 0.54% upside to 1693.

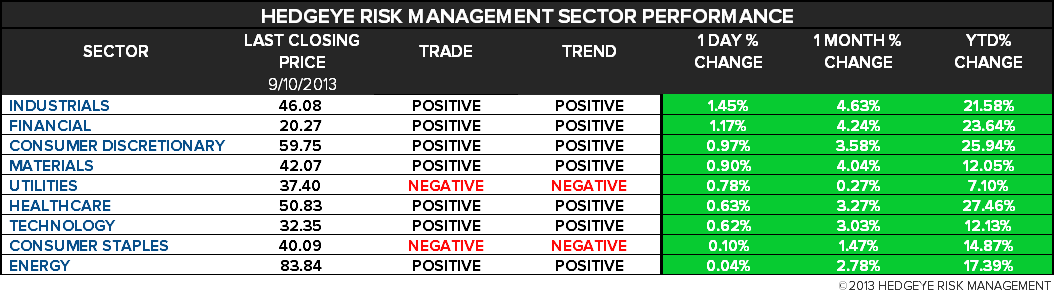

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.48 from 2.49

- VIX closed at 14.53 1 day percent change of -7.04%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Sept. 6 (prior 1.3%)

- 10am: Wholesale Inventories M/m, July, est. 0.3% (pr -0.2%)

- 10am: Wholesale Sales M/m, July, est. 0.5% (prior 0.4%)

- 10:30am: DoE Inventories

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2043 sector

- 1pm: U.S. to sell $21b 10Y notes in re-opening

GOVERNMENT:

- De Blasio gets most votes in New York Democratic mayoral primary

- House, Senate in session

- House Transportation and Infrastructure Cmte to unveil Water Resources Reform and Development Act of 2013, 2pm

- House Oversight panel meets to review TARP inspector general’s report on Treasury role in Delphi pension bailout, 1:30pm

- House Financial Svcs panel holds hearing on the Fed at 100 years, 2pm

WHAT TO WATCH:

- Obama pursues Russian proposal on Syria chemical weapons

- IBM to sell customer-service business to Synnex for $505m

- Apple iPhone 5C seen as expensive: analysts

- Vodafone $10.2b Kabel Deutschland deal under threat

- Disney delays fifth “Pirates of the Caribbean” film

- Canada, Ontario sell $1.1b in GM shares

- Verizon said to plan record bond sale of up to $49b

- China’s richest man hunts hotel mgmt cos. in U.S.

- KKR said to weigh teaming with Japan INCJ for Panasonic unit

- U.K. unemployment unexpectedly falls to 7.7%

EARNINGS:

- Dollarama (DOL CN) 7:30am, C$0.78

- Evertz Technologies (ET CN) 4pm, C$0.14

- Men’s Wearhouse (MW) 5:30pm, $1.14

- Vera Bradley (VRA) 4:03pm, $0.32

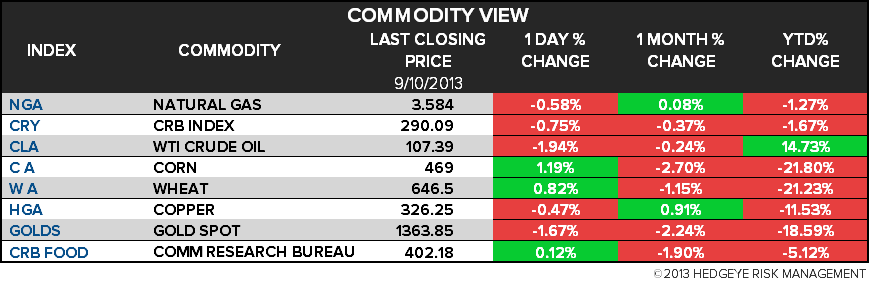

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Ruthenium Slides to Eight-Year Low as Hard-Disk Demand Declines

- Tin Shortage Worsens as Indonesia Rules Curb Supply: Commodities

- Copper Climbs as Banks Project Stronger Chinese Economic Growth

- Brent Crude Rises From Two-Week Low as Syria Strike Risk Remains

- Gold Swings Near Three-Week Low as Obama Seeks Syria Delay

- Soybeans Gain Before USDA Report Set to Signal Lower U.S. Output

- Cocoa Rises to 1-Year High in New York on Shortage; Coffee Gains

- Aluminum Buyers in Japan Said to Win Fee Cut From Suppliers

- Sugar Harvest in India Seen Beating Estimate to Worsen Glut

- Hurricane Humberto Is First of Season; Storm Gabrielle Weakens

- Goldman Expects Decline in Commodities Index in 12 Months on Oil

- Power Prices to Hold Near 8-Year Low on Weather: Energy Markets

- China Scrap Copper Imports Surge as Smelters Struggle: BI Chart

- Gold Decline Seen by Goldman as Fed’s Tapering to Spur Selling

CURRENCIES

GLOBAL PERFORMANCE

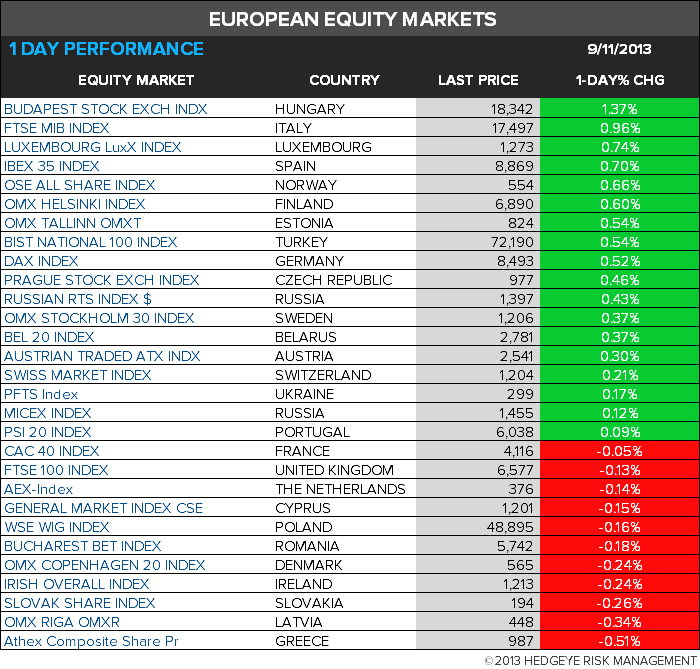

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team