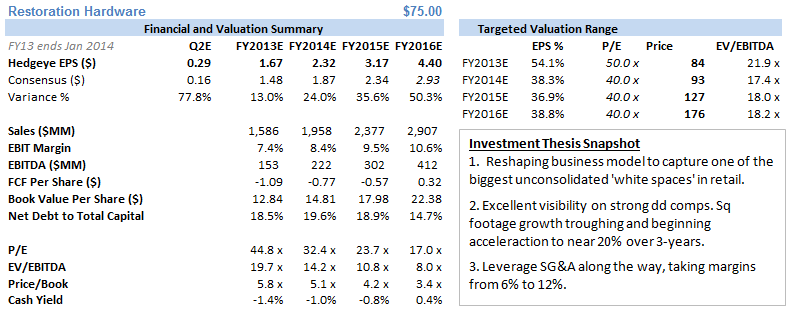

Conclusion: People are asking the wrong questions about RH. THE key question is when it will earn $8.00 per share. We think the answer is 2018.

It was absolutely painful listening to analysts grilling management on the RH Q&A wanting to be spoonfed precise guidance in the coming quarters. We love math as much as anyone – probably more. But seriously…this is a company that should earn about $1.50 per share this year, and people are asking for guidance on items that account for maybe a nickel a share? Here’s a better question… How long will it take for RH to earn $8.00?

Our current math suggests that we’ll see that number around 2018. That’s $6.50 in incremental earnings in 5-years. Put a different way, that’s a 40% earnings CAGR. Use that as ammo next time anyone tells you that RH is too expensive or that ‘they already missed it’. If you want to use a simple PEG on today’s 12-month forward earnings, you’re looking at a $90 stock within 1-year based on our model. 2-years is $125, 3-years is $175. You get the idea… If you want to review the detailed modeling assumptions, join us for our Best Ideas call on RH in 2-weeks. (We did one at the IPO at $32, and while the stock has worked, we think that the thesis has evolved to an even greater unrealized degree.)

Now…here are a couple of puts and takes on the quarter.

1) The print itself was solid. Right in line with our model with adjusted EPS coming in at $0.49 vs the Street at $0.42.

2) Revenue was in-line with our above-consensus estimate, but the composition was off. RH comped 26%, which was well-below our expectation of near 40% and the consensus of 29%. But the RH Direct business (not in the comp) came in meaningfully higher, accounting for 47% of total sales. They washed each other out. But people will always want to see the comp higher. I guess it just sounds better. This ordinarily wouldn’t matter – but with a 9.4% run in the stock 10-days leading into the quarter – the company really needs perfection to keep the treadmill going. 26% is sub-perfect.

3) On the flip side of that, RH guided up 3Q revenue by nearly 7% -- setting expectations for higher comps (high 30s). No one is upping revenue guidance in the consumer space these days. The confidence management has in its business is extreme.

4) RH eliminated the Fall Source Book – the 8 pound catalogue package that your mailman hates delivering. We give the company all the credit in the world given the sheer costs associated with the mailers and limited economic benefit. The marketing dollars will be spent with more experiential forms of advertising.

5) Combining the higher comp expectation for 3Q with the cost saves from the elimination of the mailer, RH raised EPS guidance to $0.27-$0.29 vs. the Street at $0.16. Again, a huge delta in guidance change.

6) RH appears to be on a track of Gross Margin recovery. After weakness in 1H, 3Q GM should be closer to flat, with full recovery by 4Q.

All in, the reported numbers were excellent. The cadence of strategic change to achieve the long-term earnings growth we’re looking for was there. The revenue composition combined with investors badgering management about guidance to a greater degree than usual is not going to help the stock. But we’re talking a very short window. 2H square footage is accelerating, comp is improving, and gross margins are on the rebound. And all of this is in the context of what we think is an extremely favorable 5-year growth trajectory.