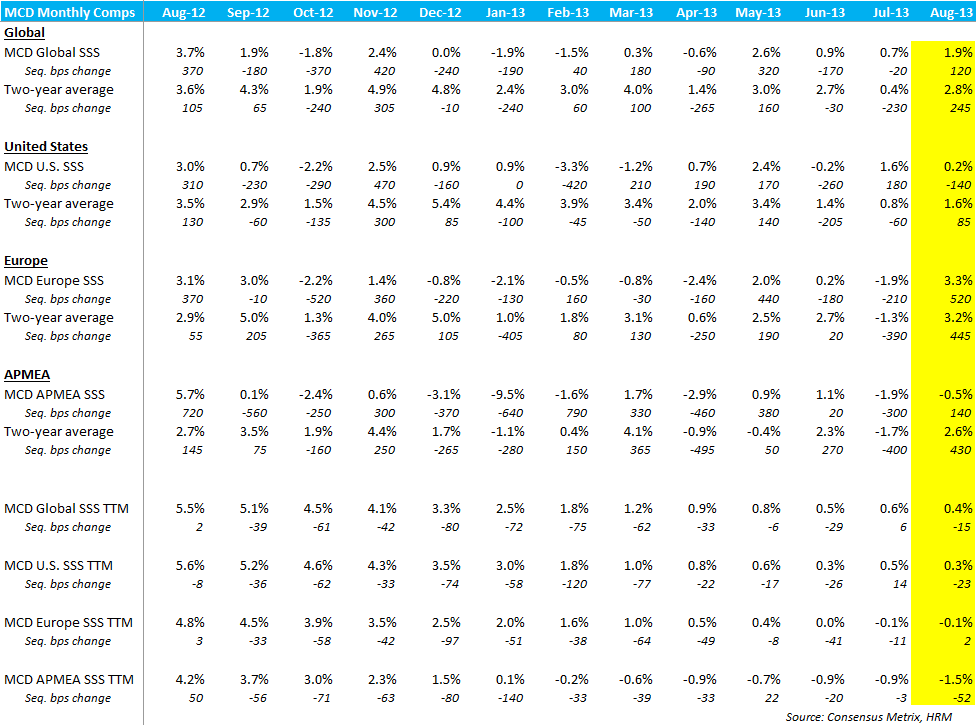

MCD reported August global same-store sales growth of +1.9% versus +3.7% in 2012. However, the two-year trend ticked up 245 bps sequentially.

The U.S. and Europe regions showed same-store sales growth of +0.2% and +3.3%, respectively. The U.S. missed consensus expectations by 60 bps, while Europe beat by 340 bps. The two-year trends accelerated sequentially to +1.6% in the U.S. and +3.2% in Europe. The APMEA region reported same-store sales growth of -0.5% versus +5.7% a year ago, beating consensus expectations by 40 bps. The two-year trend accelerated sequentially to +2.6%.

Overall, August sales were slightly better than we had expected—but not enough to change our fundamental view. Although Global sales were better than estimates, U.S. sales disappointed and remain a point of concern for us. MCD continues to refer to the U.S. environment as “persistently challenging,” which, interestingly enough mirrors the chatter we have been hearing from a majority of the larger casual dining companies more so than that of other QSRs.

Despite a flurry of recent initiatives regarding new items and menu changes propelling the stock higher, we remain comfortable with our thesis. In fact, we’ve had a rather bearish take on this news, as we believe these initiatives could add to the operational complexities of McDonald’s stores. Please see our recent note “MCD: A Pending Mighty Disaster” for more thoughts on this topic.

We continue to believe there is a disconnect between investors’ expectations and the company’s fundamentals. MCD will present tomorrow morning at the Goldman Sachs Global Retailing Conference. We’ll post on anything incremental following the presentation.

Howard Penney

Managing Director