TODAY’S S&P 500 SET-UP – September 9, 2013

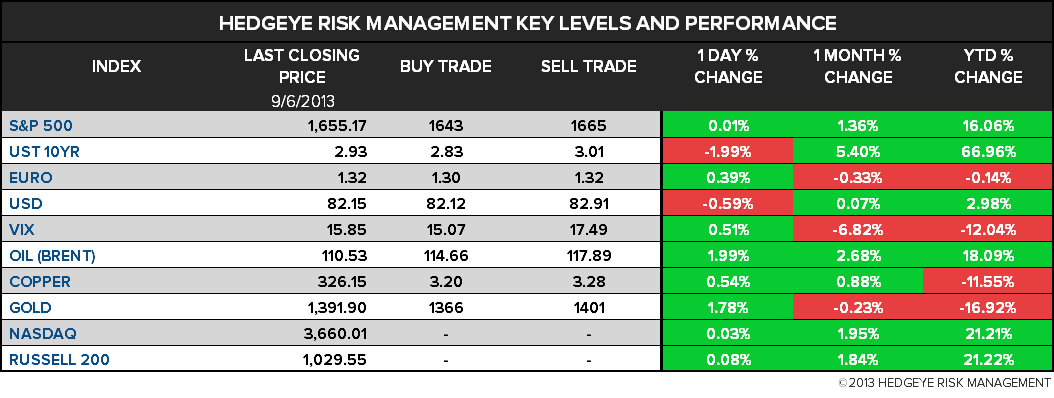

As we look at today's setup for the S&P 500, the range is 22 points or 0.74% downside to 1643 and 0.59% upside to 1665.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.47 from 2.48

- VIX closed at 15.85 1 day percent change of 0.51%

MACRO DATA POINTS (Bloomberg Estimates):

- 11am: Fed’s Williams speaks in San Francisco

- 11am: Fed to buy $1.25b-$1.75b in 2036-2043 sector

- 11:30am: U.S. to sell $30b 3M, $25b 6M bills

- 3pm: Consumer Credit, July, est. $12.3b (prior $13.8b)

- 4pm: USDA crop-conditions report

GOVERNMENT:

- Congress returns from summer recess

- Senate, House convene at 2pm; Senate will proceed to consideration of joint resolution to authorize limited use of U.S. Armed Forces against Syria

- National Security Adviser Susan Rice, Dir. of Natl Intelligence James Clapper, Sec. of State John Kerry, Joint Chiefs Chairman Martin Dempsey, and Defense Sec. Chuck Hagel brief House on plan to use military force in Syria, 5pm

WHAT TO WATCH:

- Obama expands push to sell Syria attack in war-weary U.S.

- Assad in interview said to deny using chemical weapons

- Neiman Marcus said to be near $6b sale to Ares Management

- Shuanghui, Smithfield deal obtains CFIUS clearance

- China may cut annual growth target to 7%: state economist

- China’s export growth beats ests. for a 2nd month

- Suntory to buy Glaxo’s Lucozade, Ribena for $2.1b

- Google made new offer to settle EU antitrust probe

- Nasdaq tweaks IPO cross rules with “pre-launch period”

- NYSE buys stake in private-placement startup ACE

- Tokyo winning 2020 Olympicsis seen aiding eco. recovery

- Monte Paschi wins backing from EU’s Almunia for aid plan

- Vodafone may not get approval for Kabel Deutschland offer: FT

- “Riddick” tops U.S./Canada box office w/ $18.7m

EARNINGS:

- Casey’s General Stores (CASY) 4pm, $1.26

- Five Below (FIVE) 4:01pm, $0.09

- HD Supply Holdings (HDS) Aft-mkt, $0.31

- John Wiley & Sons (JW/A) 8am, $0.43

- Palo Alto Networks (PANW) 4:03pm, $0.06

- PVH (PVH) 4:02pm, $1.37

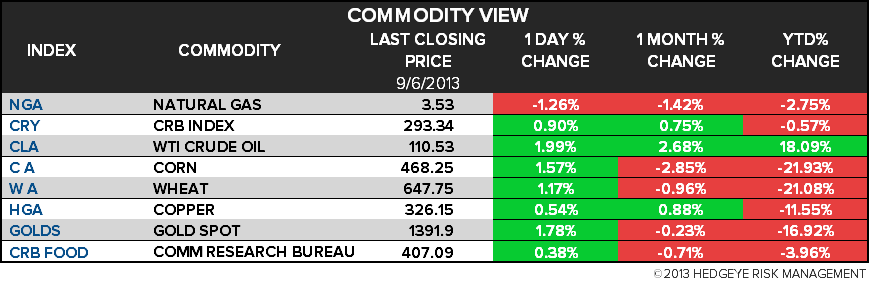

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Sales From Perth Mint Drop in August as Fed Nears Taper

- Hedge Fund Gold Bets Climb to Highest Since January: Commodities

- Gold Declines on Speculation Federal Reserve Will Curb Stimulus

- Indonesia Seen Exporting Some Tin This Month by Trade Official

- Copper Rises for Third Day as Chinese Exports Exceed Estimates

- WTI Falls From Two-Year High as Obama Presses for Syria Action

- Robusta Coffee Falls to 2-Month Low on Vietnam Crop; Cocoa Drops

- Jiangxi Copper Sees Treatment Fees Advancing as Ore Supply Rises

- Bullish Diesel Bets Spurred as U.S. Fuels World: Energy Markets

- Soybeans Rise for Third Day as Midwest Dryness Curbs Crop Yields

- U.S. Natural Gas Rebounds After First Weekly Loss Since Aug. 9

- Chinese Zombies Emerging After Years of Solar Subsidies: Energy

- Gradually Rising Capacity Rates Bullish for Steel: Bull Case

- Gold Inventories Plummet 36%, Leverage Is Highest in Nine Years

CURRENCIES

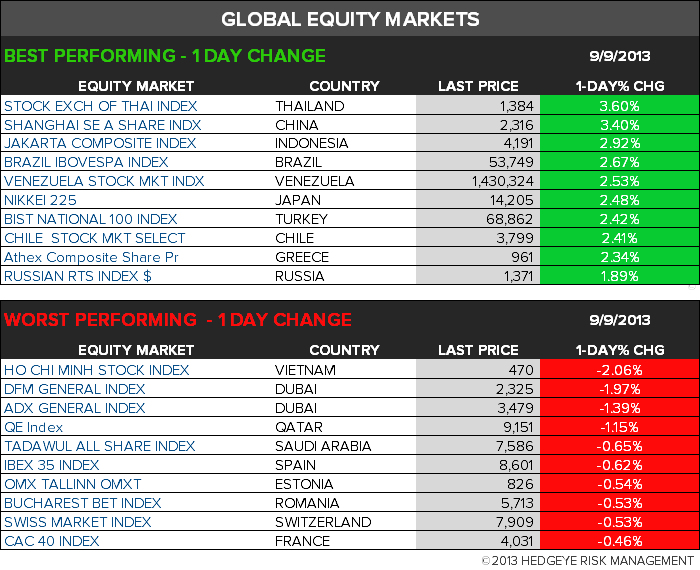

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

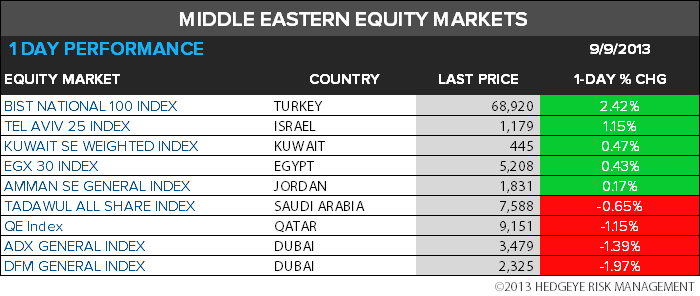

MIDDLE EAST

The Hedgeye Macro Team