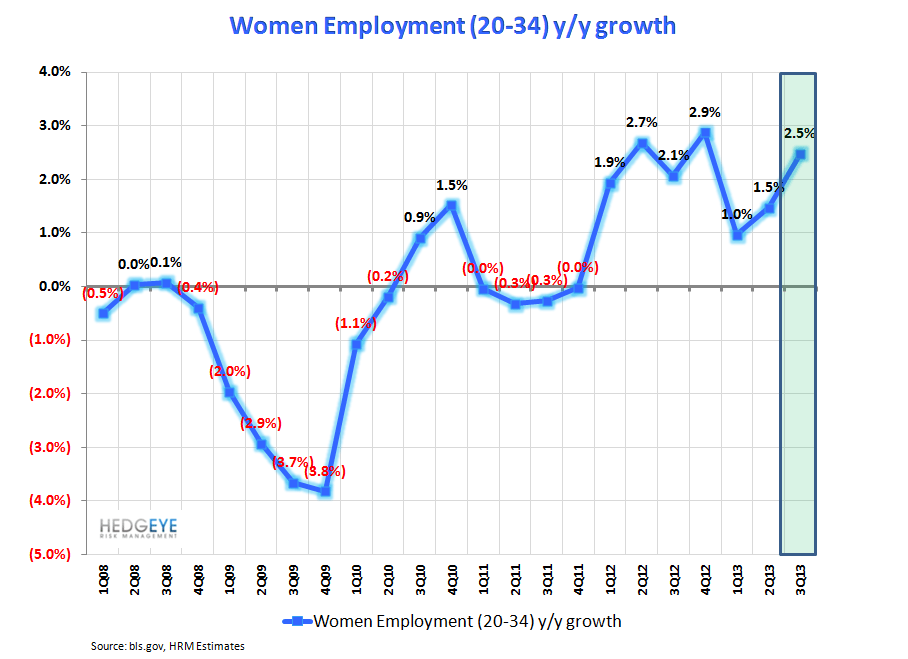

Here’s a number from today’s jobs report that most overlook – the employment growth among women aged 20 to 34. As the chart below shows, that year-on-year employment growth among those women is accelerating.

Those numbers dovetail with Healthcare Sector Head Tom Tobin’s theme of rising birth rates as employment often comes with health insurance, which is pretty much a necessity before having a child.