Conclusion: The slope in bond yields continues to follow the slope of improvement in the labor market and broader domestic macro data in July/Aug. Another YTD low in Jobless Claims, another multi-year high in ISM New Orders, and a return to positive labor productivity growth preface tomorrow’s jobs report.

INITIAL CLAIMS

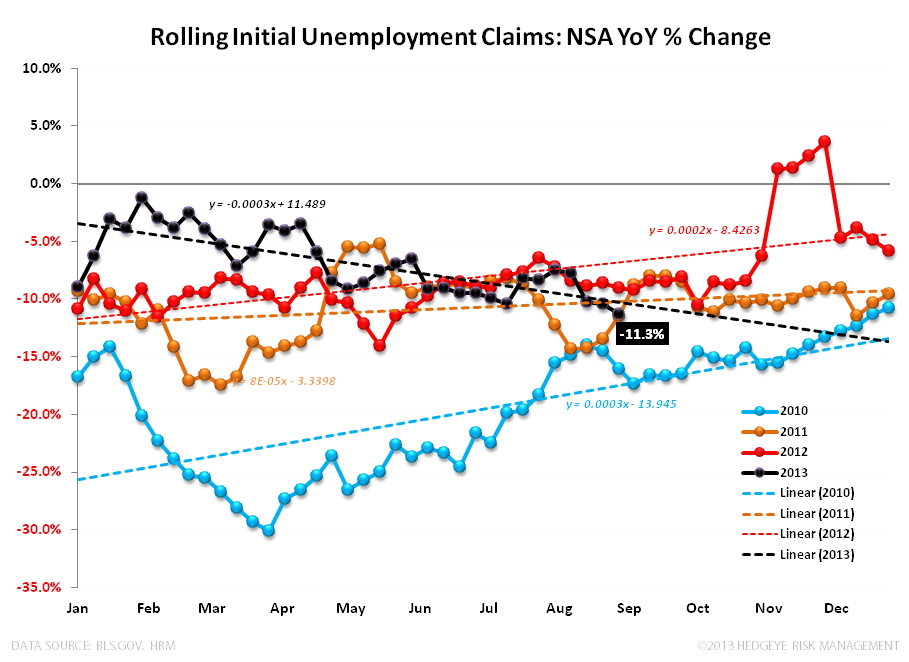

Non-seasonally adjusted Claims: NSA claims registered another new cycle low, and lowest reading since September 2007, in absolute terms this week at 269K.

The YoY rate of change improved to -13.1% vs. 10.8% (revised) last week with the 4-week rolling average in YoY claims accelerating -80bps to -11.3% this week vs. -10.5% the week prior.

In short, our favored read on the underlying strength in the labor market, continues to register accelerating improvement.

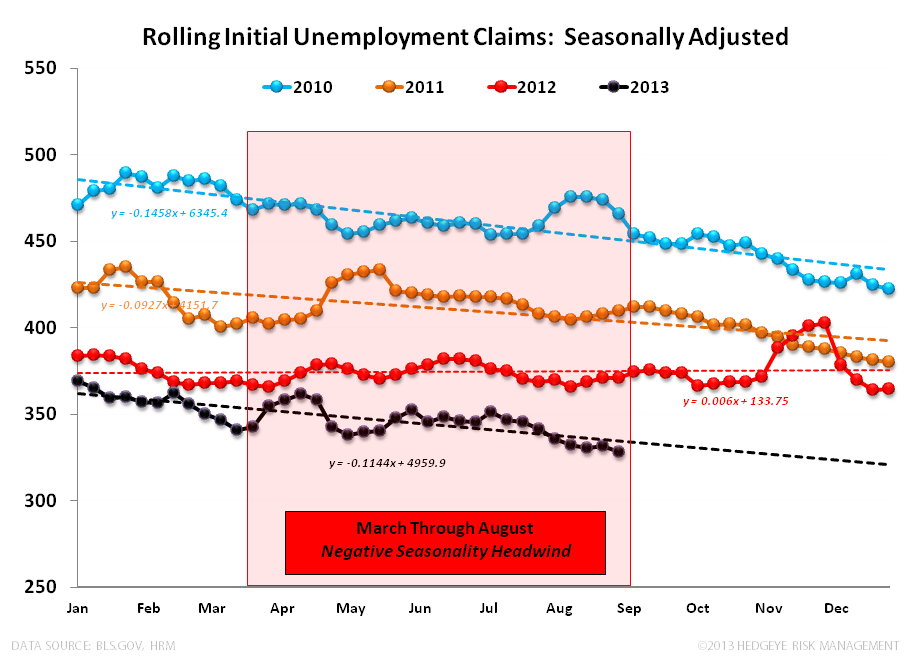

Seasonally adjusted Claims: Headline, seasonally adjusted initial jobless claims declined 8K WoW to 323K – on par with the lowest print of the year and lowest reading since January 2008. The 4-week rolling average in claims declined -3K with the YoY and 4wk rolling YoY rates of improvement both accelerating sequentially.

The slope of bond yields continues to follow the slope of improvement in the labor market and slow growth, yield chase assets (see utilities/staples in Sector Divergence Monitor below) continue to come under pressure alongside #RatesRising, an improving growth outlook, and the realities of monetary policy renormalization.

We think the prevailing asset class and sector level performance dynamics (i.e slow growth lower vs high growth higher, Stocks Ups vs. Bonds/Gold Down) continue to extend themselves.

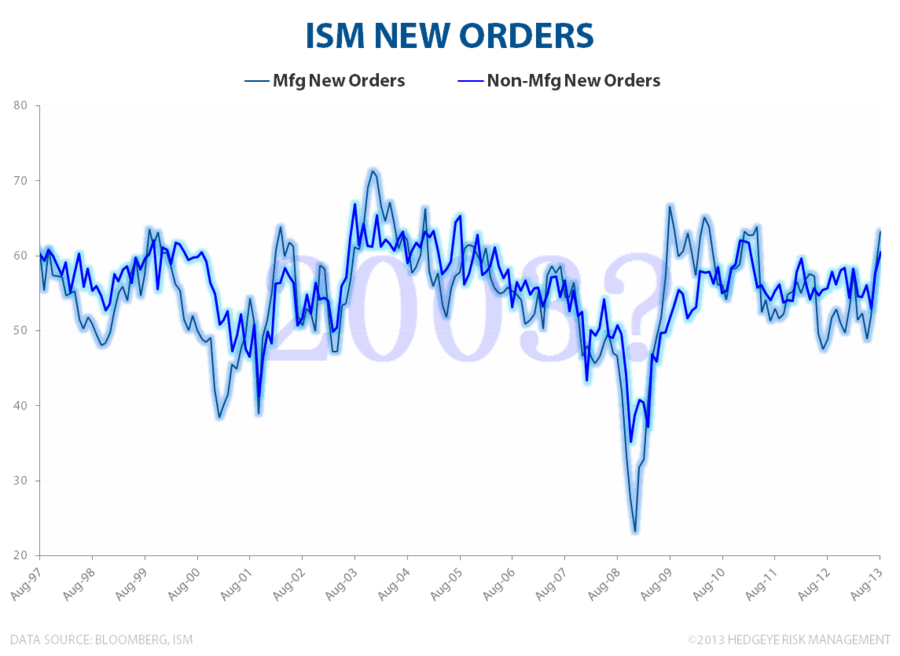

ISM Non-Manufacturing: The ISM services data followed yesterday’s manufacturing data higher with the composite index advancing to 58.6 in August from 56.0 in July. The Business Activity, New Orders, Employment, Deliveries, and Backlog components all strengthened sequentially. Notably, the best lead indicator within the componentry - New Orders - breached 60 to the upside, registering its strongest reading since February 2011.

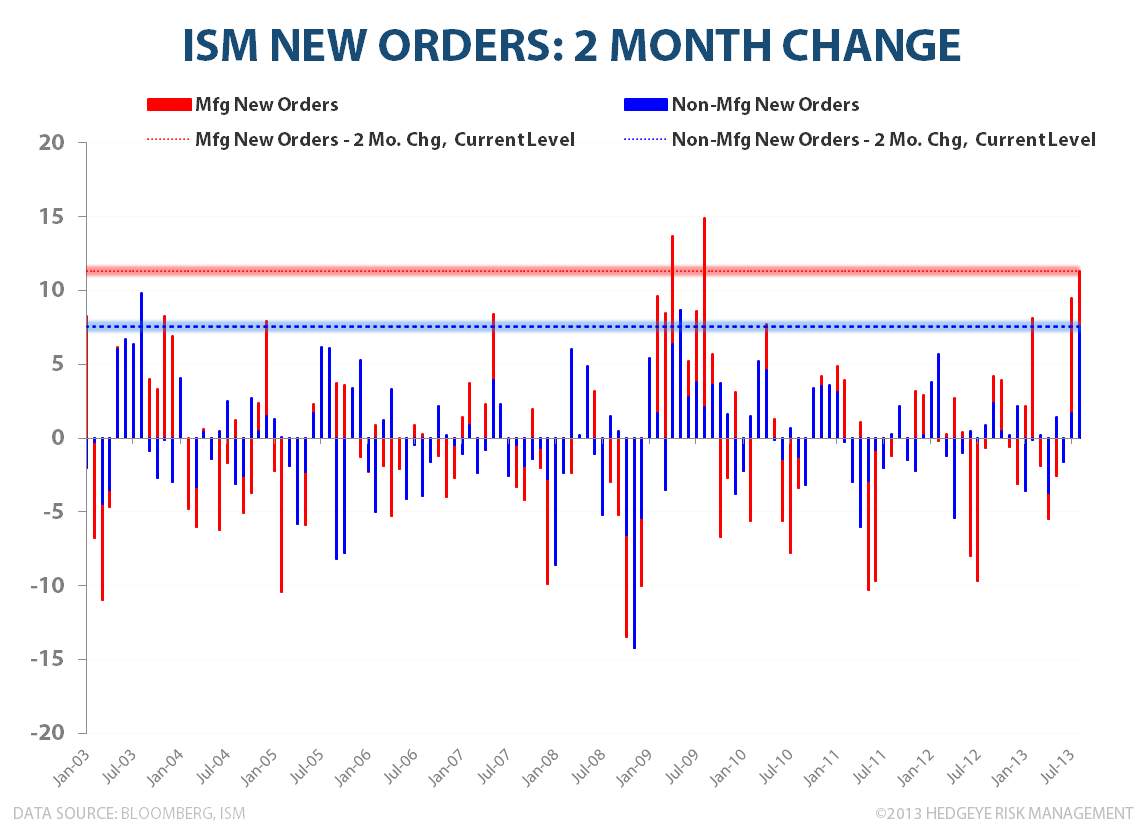

On a two month basis, the New Orders reading within both the Manufacturing and Non-Manufacturing Survey’s posted their best advances (outside of the onset of the recovery in mid-2009) since 2001 and 2003, respectively.

On balance, manufacturing, which sat as the domestic macro deadbeat in the March-May period, is showing accelerating improvement with the ISM, PMI, and Fed Regional Survey data all strengthening over the July/Aug period.

Labor Productivity: Meanwhile, the final labor productivity data for 2Q13 came in at +2.4% after a two quarter stretch in negative territory. Nothing particularly investable here, but nice to see a return to positive growth >2%. Longer-term, and in context of the Labor Market, with demographics and (potentially) other structural headwinds creating secular pressure on domestic labor supply, productivity gains will sit as an increasingly important driver of real output growth.

Christian B. Drake

Senior Analyst