“Money is one of the shatteringly simplifying ideas of all time; it creates its own revolution.”

-Paul Bohannan

That’s the opening quote to an important book I started reading this week, The History of Money, by Jack Weatherford. The book’s first paragraph goes on to ring the Gold bull bell with “The Dollar is dying; so too are the Yen, the mark and the other national currencies…”

When it was published in 1997, Charles Schwab called this “the book to read.” And I agree, you should read every economic history book you can get your paws on – your hard earned money is too important to leave to the people opining on it from Washington.

The shatteringly simple observation about money is context. Its history is at least 3,000 years old. And when debating it, consensus tends to cram its craw into the moment in which it lives. The Dollar isn’t dead this year; it’s breaking out from a 40 year low. The Yen didn’t die after 1997 either (it ended up hitting a 40 year high by 2011). Everything, including the value of your moneys, is relative.

Back to the Global Macro Grind…

After another shatteringly strong string of US economic data points (starting last Thursday with US roiling jobless claims hitting another YTD low and culminating with a blockbuster New Orders component of yesterday’s ISM report for August), yesterday’s US stock market ripped a +1% morning move to the upside and Treasury bonds continued to collapse.

Up for the 4th consecutive week, another #StrongDollar move was nipping on the heels of #RatesRising too. Consensus isn’t positioned for that, so I loved it. Then, all of a sudden, the most bearish catalyst of all hit the tape – a US politician’s opinion.

In the last year, there have been very few market risks that have scared me more than US central planners intervening during critical periods of market entropy. Going back to November of 2012 (when bond yields bottomed), Boehner’s voice was as market bearish as any you could find. He was the bearish factor yesterday too – the whole thing is just plain sad to watch.

Back to the economic gravity part…

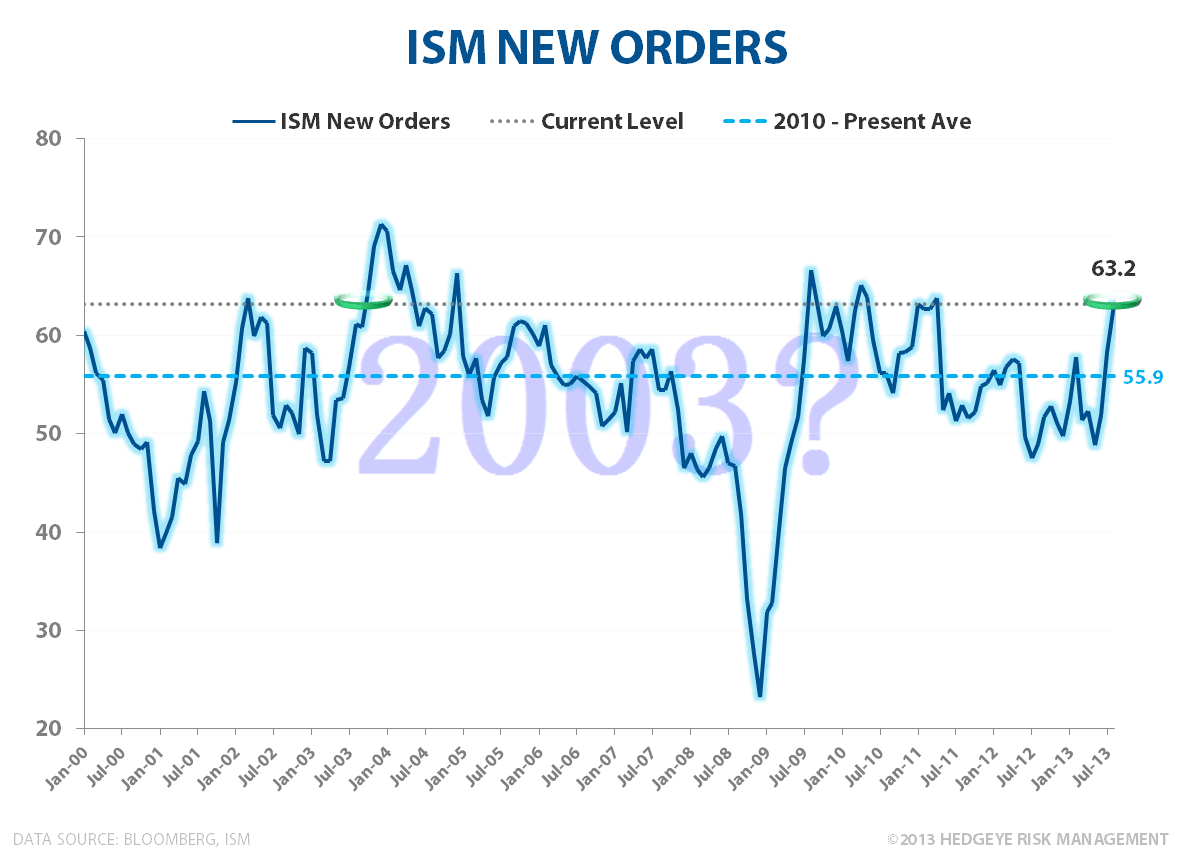

- New Orders (in the ISM report for August) hit a monster shot of 63.2! yesterday (vs 58.3 in July)

- Go back to 2003 (see Chart or The Day) and look at how quickly economic gravity shocked growth bears to the upside

- Not unlike 2000-2002, consensus has become shatteringly bearish about growth; it’s a lagging indicator

To be clear, there’s a big difference between consensus being bearish and Mr. Market’s bullish opinion. While yesterday’s intraday gains in the SP500 were cut in half, the decliners were led by the slow-growth sectors (gainers were once again all about growth):

- Slow-Growth Utilities (XLU) got smoked again (after being down -5% for AUG), leading losers on the day at -1.2%

- Dividend Yield Chasing Consumer Staples (XLP) were down -0.1% in an up market as well (XLP -4.5% in AUG)

- Nasdaq (QQQ) +0.63% and Financials (XLF) +0.9% led gainers, as they have throughout 2013

In other words, if you are bummed out about Kimberly Clark (KMB) or Kinder Morgan (KMP) not getting you paid on the principal appreciation side of the equation, that’s just too bad. This Bernanke Yield Chaser style factor was as much a bubble as Gold was.

#RatesRising for the right reasons (growth expectations rising), is public enemy #1 for overvalued, slow-growth, securities. Whether it feels right or not, money chases positive returns. It flows away from draw-down risks.

Since I’m already out of everything Commodities, Fixed Income, and Emerging Markets (0% asset allocations), I have had relatively low stress on the draw-down risk side of big macro asset class moves in 2013 (Gold bounced, but is still -17% YTD and bonds are getting smoked), but that doesn’t mean I can afford to give up a lead for the sake of being beholden to this great growth data.

There are 3 big Macro things that would get me out of being long growth equities:

- If #StrongDollar snaps its long-term TAIL risk line of $79.11

- If #RatesRising stops and the 10 yr UST Yield breaks 2.44% @Hedgeye TREND support

- If #GrowthAccelerating Style Factors (like Nasdaq diverging from the Dow) reverse and break TREND

Johnny one-time Boehner’s intraday comments mattered because they kept the #1 risk to what’s been strong US consumption growth in play. It’s called an Oil tax at the pump. And Putin likes it.

The best way for Obama to pulverize Putin in St. Petersburg this week would be to stick a weapon of mass currency appreciation in his grill. If I was advising the President, I’d have him bring that #StrongDollar ace to the table – and maybe say something like this:

“Vlad, if you don’t tone this down, I am going to taper, then tighten – and if you don’t think I can get Summers to do it, try me – your little Petro-Dollar Putin power problem will look like Fukushima, and fast.”

But that’s just me – I’m a doer type of a guy who likes to make decisions without asking the bureaucracy of the world for its opinion. I’d like to see a US President build a #StrongDollar, Strong America revolution on the back of your hard earned currency.

Our immediate-term Macro Risk Ranges are now:

UST 10yr Yield 2.73-2.93%

SPX 1

Nikkei 133

VIX 15.93-17.98

USD 81.78-82.65

Brent 113.12-117.98

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer