This note was originally published at 8am on August 15, 2013 for Hedgeye subscribers.

“How far is it wise to respond to a mood?”

-Frank Oppenheimer

Since yesterday’s Early Look focused on asking ourselves baseline risk management questions, I’ll roll with a good one that particle physicist Frank Oppenheimer asked his older brother in the 1930s. Here’s how Robert Oppenheimer answered it:

“… my own conviction is that one should use moods, but not be greatly deflected by them; thus one should try to use the gay times to do those things one wants to do that require gaiety, and the sober moods for the work one wants, and the low moods for giving oneself hell.” (American Prometheus, pg 95)

I’m a moody guy. So that answer spoke to me. Sober every morning, working. Giving myself hell about all my market mistakes come the afternoon. Sounds about right.

Back to the Global Macro Grind…

Markets are moody too. They rarely cooperate with all of your positions. And they don’t care whatsoever about your views. Tough relationship we have with this Mr. Market, I know. That’s why I am lobbying the Fed to call her Mrs.

Early last week I polled you asking whether you thought the latest #EOW (end of the world) correction in US stocks would be on the order of 1, 2, or 5%. Since only one client answered 1%, I figured the probability of that being the correct answer was going up.

If you answered 5%, please don’t go all caps or moody on me. Take a breath. It’s just an opinion. And we all have one or we wouldn’t be playing this game. Currently the correction (from the all-time closing high of 1709 in the SP500) is -1.4%.

Now what? Well, let’s redo the poll with some forward looking information:

- Immediate-term TRADE support is 1680 = -1.7% from the all-time high

- Intermediate-term TREND support is 1637 = -4.2% from the all-time high

- Immediate-term risk range for US Equity Volatility (VIX) = 11.62-13.71

So, what do you think?

A) 1% correction (i.e. the market closes up today and yesterday was it)

B) 2% correction (somewhere between today and early next week, that’s it)

C) 4% correction (re-testing the TREND line, which we haven’t done since late June)

I’m going with B again.

If the market closes up on the day today, that will make me and everyone else (other than anonymous client Mr. X) who answered the poll last week wrong. If that happens, we can all just give ourselves hell.

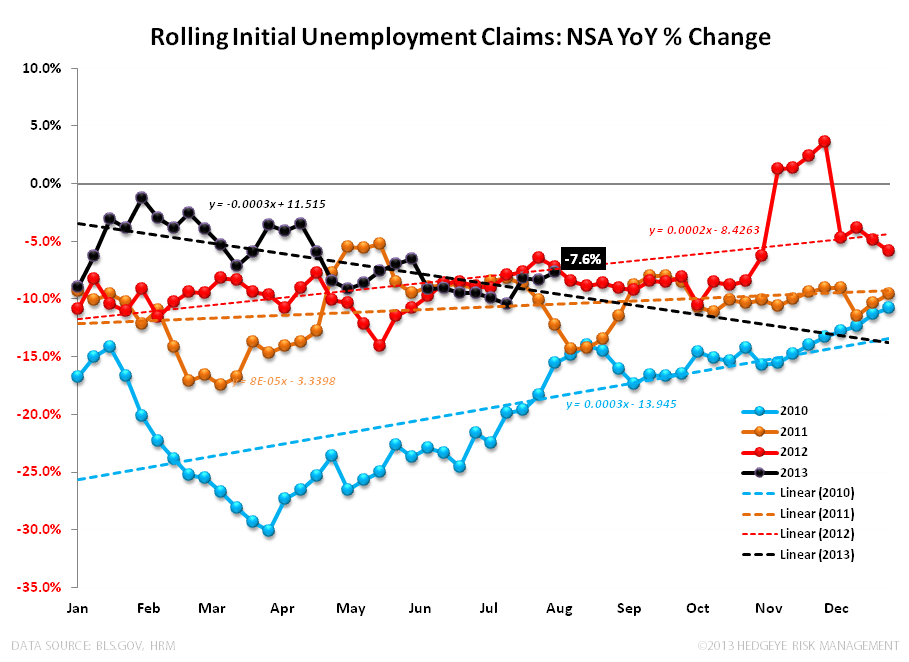

What would have been really hellish in 2013 is missing this call on US employment #GrowthAccelerating. Again, we don’t care about the line-items in the BLS data; we only care about the slope of the line in the only leading indicator we can find for the bond market: NSA (non-seasonally adjusted) rolling US jobless claims. Most of the monthly payroll data is statistically useless.

We’ll get that weekly US Jobless Claims data point this morning – and if there’s one data point that matters to both the long-end of the US Treasury curve (and the US stock market), that is it. So let’s put this morning’s number in the context of recent history:

- Last week’s NSA claims number came in -10.5% year-over-year (slight improvement vs the previous week)

- The average for the last 12 weeks is claims falling -8.8% year-over-year

- Giving exception to a single anomalous data point 3 weeks ago, avg y/y improvement over 12 weeks = -9.7%

Yes, that’s a lot better than your parroting partisan pundit would lead you to believe. It’s also our definition of not only what matters to the employment vs Fed story, but what Mr. Market trades on – the 10yr US Treasury Yield fits NSA rolling claims like a glove.

Oh, and there’s seasonal headwinds in this jobless claims series that become tailwinds in September (that can run through February). Most (other than Mr. Bond and Stock Market) don’t expect to see the jobs picture improve, so it probably will.

One other way to measure the moodiness of it all is the weekly II Bull/Bear Spread:

- Last week, Bulls dropped from 51.6 to 47.4%

- Last week, Bears rose from 18.5 to 20.6%

- Last week, Bull/Bear Spread re-tested its most bearish level since Q2 at 2680 basis points wide

Yep – everyone says everyone is bullish. But they aren’t. Less than 50% are bullish. That’s really bearish. And the last time we saw a 2600bps handle on the Bull/Bear spread was in the 1st week of July. The SP500 proceeded to move from 1631 (our new TREND support) to 1709 within a month.

So, if you are all beared up (on stocks) this morning, just remember that bullish gaiety can quickly become a mid to late month-end move. The profitable bearish mood is in bonds. We’ll see if this morning’s jobless claims print reiterates that. September is coming.

UST 10yr 2.64-2.75%

SPX 1682-1712

VIX 11.62-13.71

USD 80.94-82.02

Yen 97.37-99.45

Brent 108.11-111.49

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer