“Information itself is best defined as surprise.”

-George Gilder

The first four chapters of George Gilder’s Knowledge and Power are right up my alley: “The Signal In The Noise”, “The Science of Information”, “Entropy Economics” – yes, someone else is talking “entropy” in the same sentence as markets! #beauty

On #OldWall, Gilder nails it: “The war between the centrifuge of knowledge and the centripetal pull of power remains the prime conflict in all economics.” And on risk management: “It is an economics of surprise that distributes power as it extends knowledge.” (page 5)

Think that through. In our profession, new information is surprise. If it wasn’t, why did so many risk going to jail? There is no easier way to generate returns than having inside information. Perversely, the road less travelled is the legal one. That’s why the 2.0 processes are taking mind share. We win and lose in an open forum of transparent information flow. We thrive by Embracing Uncertainty.

Back to the Global Macro Grind…

If many pieces of information aren’t surprising you throughout your risk management day, you probably don’t have enough factors in your model. Price is surprise. So is data. Information surprise is everywhere.

So how do you absorb it all and remain sober? The answer is it’s a grind. Multiple-factors, multiple-durations – the market waits for no one. Being proactively prepared to contextualize the most immediate-term of surprises is only the beginning.

Bucketing the big stuff into intermediate-term TREND macro themes helps, provided that your process is flexible enough to acknowledge that TRENDs can change. But what is change? In Chaos Theory speak, can a major macro phase transition be undone?

Of course, in the intermediate-term, everything and anything can be undone – this is the fulcrum principle of central planning! In the long-run, gravity takes hold of anti-dog-eat-dog-cycle-smoothing though. So you want to be on the lookout for that!

There is a massive phase transition that is being baked into market expectations right now. The causal driver of that expectation shift is whether or not the US Federal Reserve is done with its anti-gravity policy to devalue the US Dollar and monetize the USA’s debt.

The main regime changes in a #RatesRising environment (versus one discounting 0% rates in perpetuity) are as follows:

- Growth (as an investing style) outperforms slow-growth Yield Chasing

- Strong Currency countries outperform Currency Crisis countries

That’s basically what happened again last week:

- Nasdaq and Russell2000 (growth indices) were +1.5% and +1.4%, respectively

- US Consumer Staples Stocks (XLP) were -0.2% on the wk (-2.85% for the AUG to-date)

- Asian (ex-Japan) Equities were -3.3% (down -8% for the YTD)

Parts 1 and 2 of that are pretty straightforward – unlevered US domestic innovation (growth stocks) are absolutely ripping this year versus a basket of pretty much anything slow-growth. That’s not new as of last week either. That’s been the TREND since June.

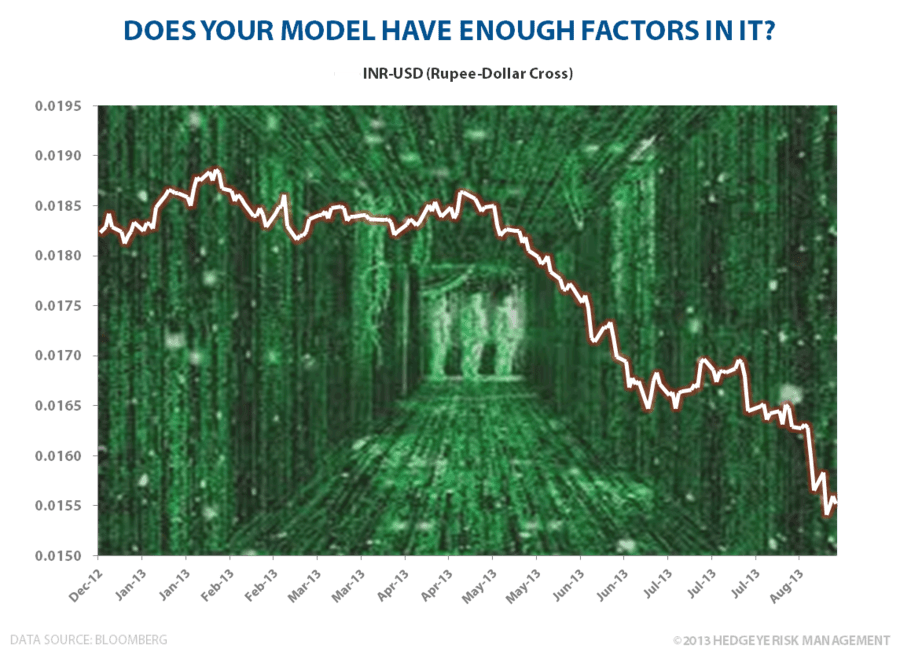

In June, #RatesRising ripped a massive amount of entropy into markets. Most people get that by now. What less people have realized is how powerful a combination A) #RatesRising and B) #StrongDollar can be versus Emerging Markets (both equity and debt).

USD didn’t go down for the 2nd week in a row last week, here’s how that new information flowed to Indonesia, Chile, etc.:

- Emerging Markets (MSCI Index) = -2.6% on the wk to -11.6% YTD

- Emerging Markets Latin American Index (MSCI) = -1.5% on the wk to -17.2% YTD

Now, to be fair to the Chileans, they are also right levered to another major macro risk factor that comes into play during #StrongDollar and #RatesRising regimes – we call it #CommodityDeflation (the CRB Commodities Index = -0.6% last wk = -1.4% YTD).

Since #StrongDollar was more of a 1st six months of 2013 story doesn’t mean that the #CommodityDeflation risk ceases to exist (Coffee prices were -5.3% last wk to -25.2% YTD). Again, looking at the YTD scoreboard:

- Peru (metals/mining represents over 1/3 of the index) is the worst country in Global Equities at -19% YTD

- Chile and Brazil (both resource heavy indices) are 3rd and 4th worst in the world at -15% and -14% YTD, respectively

- Gold: despite its +4.5% month-over-month bounce off the lows, it is still -17.2% YTD

Ostensibly, there is new immediate-term TRADE information here to consider. If the US Dollar continues to weaken like it has from its July 2013 YTD highs, why can’t commodities and their related country stock market indices continue to re-flate?

Alternatively, the USD could be doing more of the same (building a gigantic base of higher-40yr-lows that were caused by the US cutting rates to zero), and this bullish Consumption (Growth) vs. bearish Commodities (Absolute Return Yield Chasing) theme remains intact.

The beauty of modeling macro the way that we do is that we don’t have to be certain about any of the answers to these questions. We simply have to absorb all of the information surprises we receive within the context of multiple durations, factors, and cycles – and make the highest probability call we can from there.

Our immediate-term Macro Risk Ranges are now as follows:

UST 10yr Yield 2.72-2.95%

SPX 1

VIX 12.17-14.98

USD 80.89-81.76

Euro 1.32-1.34

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer