“We are almost entirely incapable of predicting the future.”

-George Gilder

That’s the closing sentence to the opening paragraph to “The Need For A New Economics”, which is Chapter 1 of George Gilder’s latest book, Knowledge And Power.

The opening sentence is better: “Most human beings understand that their economic life is full of surprises.” And it’s better because it’s more in line with reality than an all-or-nothing statement about forecasting.

For me, risk management isn’t about predicting the future. It’s about probability weighting our decisions within a repeatable, but flexible, process. If you establish a multi-factor, multi-duration process, you’ll find yourself forecasting when you are about to be right and wrong, faster. Changing your mind is more important than anchoring on predictions.

Back to the Global Macro Grind…

As I was flying back from Los Angeles last night, I was thinking about everything I always think about when I have time to think – my family, my firm, and the Fed.

What on God’s good earth is the Fed going to do to my family and firm next?

It’s sad, but this is what our said free-market life has become. I was on the road all week seeing clients in California and I couldn’t go through 20 minutes of long-cycle (40-60 years) macro research without having to debate how the Fed can interrupt our analysis of things like economic gravity.

Never mind predicting the future, some of these un-elected central planners think they can “smooth” it! That’s just dumb. And I can only thank progressive information innovations like Google and Twitter for expediting the world’s education on that.

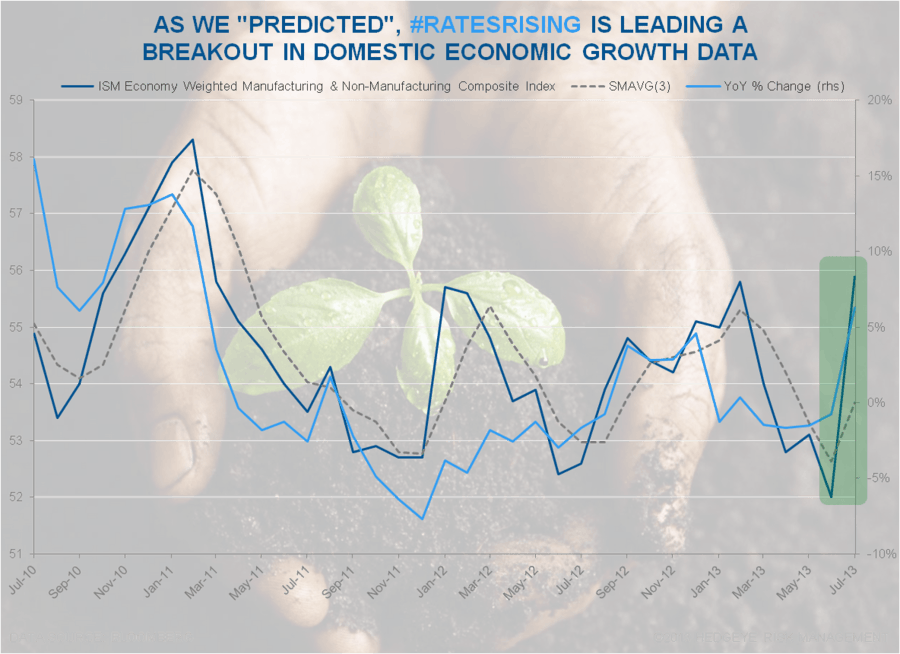

Bernanke’s Fed thought they’d be able to smooth the long-end of the yield curve – nope. Bond Yields continue to rip a series of higher-lows and higher-highs on accelerating US employment growth data. I know, after seeing the Nasdaq and SP500 correct -1.5-3% from their YTD highs, that must be the new bear case for US Equities. The data is now too good.

Got good data? Here’s how the most important leading economic indicator for US bond yields did this week:

- Initial Jobless Claims rose 16,000 this week to 336,000

- The 4-week rolling avg of claims dropped 2,250 this week to 330,500

- The 4-week NSA rolling avg of claims was -10.3% y/y versus last week’s -7.8% y/y

In other words, the bond market has it right. The Fed and bond bulls are still fighting both the data and the market. NSA (non-seasonal adjusted claims) remain our preferred leading indicator, primarily because it fits the 10yr Yield like a glove.

BREAKING: the Fed’s new “forward guidance” model is called the market front-running them.

From our latest Hedgeye Jedi hire, Jonathan Casteleyn, check out this week’s fund flows (i.e. outflow data) in Fixed Income:

- Fixed Income outflows accelerated to -$3.9B this week versus -$2.0B last week

- Tax-free (municipal bonds) continued their sharp outflow trend, losing another -$2.0B last week

- The 2013 weekly avg of Fixed Income inflow has now declined to $469M (vs +$5.8B in weekly inflows in 2012)

That’s not a typo.

Since President Obama is, allegedly, saying “no more bubbles” now, let me write that one more time – this past week’s #RatesRising Fixed Income OUTFLOWS were -$3.9B versus the 2012 Bernanke Bond Bubble weekly avg INFLOW of +$5.8B in 2012.

#cool

Nah. This ain’t cool bro. This is what we call another disaster for Americans who got jammed into everything yield chasing from Gold, to MLPs, to anything that looked and/or acted like a low-beta bond used to.

But don’t worry, Bernanke didn’t have anything to do with that or growth oriented investments pulverizing the slow-growth Yield Chasers (like Utilities) since bonds went over The Hedgeye Waterfall in June.

We use the thermodynamic model of the volume and velocity of water approaching its point of entropy (The Waterfall) as an alternative to the broken economic and market forecasting models of the Federal Reserve.

Rather than a crystal ball model, it’s a real-time probability weighted model that embraces uncertainty. And it works. What doesn’t work is attempting to ban and/or smooth things like free-market gravity.

As a result, the only long-term future prediction I will hang my hat on is that American monetary policy will evolve. If I’m wrong on that, as their old boy Keynes would say, in the long-run we’ll all be dead anyway.

UST 10yr 2.78-2.97%

SPX 1

Nikkei 135

VIX 13.97-15.65

USD 80.91-81.90

Yen 97.71-99.09

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer