IDEAS UPDATES

Below are the latest comments from our Sector Heads on their high-conviction, long-only stock ideas. Please note that our Financials team has added T. Rowe Price (TROW) to our Investing Ideas list this week.

FDX – The stock is just shy of a 52-week high and has outperformed the S&P 500 over that period, so it is not necessarily a contrarian stock. On a valuation basis, the stock is cheap trading at less than 6x TTM EV/EBITDA and has net cash on its balance sheet (excluding leases).

Many of the industrial data points that we track have moved favorably this summer, with rail, truck and airfreight indicators among them. To the extent that the operating environment continues to strengthen, it could provide a tailwind to FDX’s restructuring efforts.

FedEx also announced expanded options in for healthcare-related shipping, better accommodating items that require refrigerated environments. Growth in higher margin, niche markets is a focus for the industry.

HCA – Back in 2009 indebted companies, hospitals included, had a rough time convincing the markets they were going to make it through the debt crisis. It's easy to see what happened in the correlation between junk bond indexes such as JNK and hospital company stock prices both during the crisis and through the recovery. With #ratesrising and the junk bond indices getting pummeled as the 10-year yield moves out from under the federal reserves thumb, we are not seeing the same correlation and downward pressure on hospital stocks.

HOLX – We continue to like the opportunity for HOLX under the Obamacare, even if the law's first days go poorly. We estimated the additional number of Pap tests and mammography scans coming from the newly insured then took big cuts for the myriad of reasons why the law's targets are likely to fall short. Whether its states not expanding Medicaid, the Exchanges not being ready, or simple confusion on the part of everyone involved, HOLX is likely to get a sizable boost to their revenue growth next year.

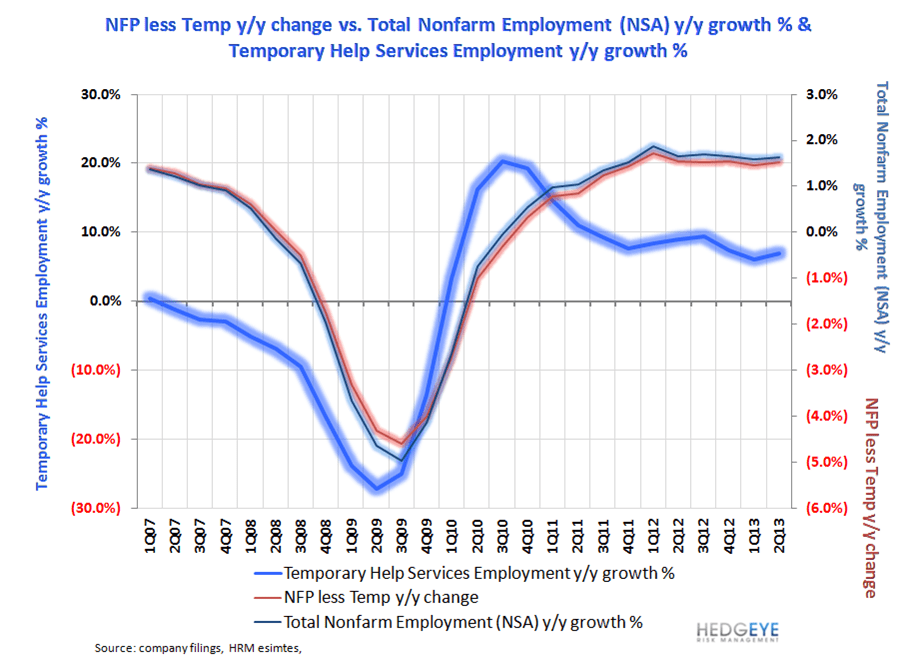

MD – We began taking a look at the role of temporary and part time workers on medical consumption this week. The media continues to write stories about firms skirting Obamacare regulations by hiring temporary versus full time employees. Media accounts are largely based on anecdotes, but we have had trouble finding actual data that backs these claims up.

It's a terrible idea that Obamacare's goal of insuring the uninsured and broadening medical security for some of the 50 million who go without insurance will lead to more people in temp jobs without health benefits. The temp Trend is a risk to a broad range of healthcare companies including MD, but so far the facts don't check out on the temp trend.

Temp job growth is still outpacing all other employment, but the impact is minimal on non farm payrolls (NFP). Reducing the NFP by Temp jobs, and employment is still growing (right axis, thin blue and red lines)

MPEL – August revenue growth in Macau is trending in the +16-20% range. MPEL’s August revenue share of 14.2% remains above recent trends. We remain positive on Macau with MPEL leading the way, particularly in the margin-rich mass segment.

NKE – Nike’s Brand Jordan is having a great start to "Back-To-School," with sales growth over the past three weeks accelerating from 10% to 20% to over 40% according to The NPD Group. Why does this matter, one might ask, given that it is only a sub-brand of a globally-diversified portfolio? Not really the mountain/molehill metaphor that one might think. In the US, Jordan has evolved from a mere shoe into a massive brand. Nike’s share of the market is 42%. The next largest brand? You guessed it -- Jordan at over 13%. Next in line? Adidas, which struggles to capture 7%. Rounding out the top five are Skechers at 4.3% and New Balance at 4.0%. Put another way, Jordan is 5x the size of Reebok, which once challenged the Nike Brand as the biggest sneaker brand in the US.

NSM – There are two important intermediate term considerations for Nationstar investors. One is rates and the other is deals. The back half of 2013 is likely to see an increase in mortgage servicing-related deal activity as the big three (NSM, OCN, WAC) all raised their acquisition pipeline estimates during their second quarter results (by a combined $145 billion). Interestingly, NSM accounted for 70% of the increase. These deals historically have been accretive and catalytic for shares. We have no reason to think the result would be different in the coming quarters.

On the other hand, there is the #RatesRising dynamic. One of Hedgeye’s top themes at the moment is that long-term interest rates are likely to continue to move higher, making higher highs and higher lows. Rising rates are like an anchor on mortgage refinance volumes and Nationstar derives a substantial share of its earnings from refi activity. That said, Nationstar’s refi business is more defensive than many realize because it has a large contribution from HARP activity, which is less rate-sensitive than traditional refi volume.

Our expectation is that Nationstar shares will grind higher over the intermediate term on positive news around deals, but that rising rates act as a short-term headwind in the vacuum between deals.

TRADE: In the short-term, the market is and will continue to trade NSM inversely to long-term interest rates in the absence of other data, and rates have been grinding higher of late.

TREND: Over the intermediate term, the stock will trade around announcements of servicing acquisition deals. We think NSM remains well positioned here, alongside Ocwen and Walters.

TAIL: In the long-term, there is still a tremendous opportunity for non-bank servicers like Nationstar to roll-up the servicing business. NSM is well positioned to be a prime beneficiary. We continue to think consensus earnings estimates remain too low for 2013/2014.

SBUX – No material changes to our high conviction call on Starbucks as the stock continues to flirt with all-time highs. Yes, we acknowledge that SBUX is a “top pick” for many Wall Street analysts, but consensus can be right sometimes. Bottom line is we continue to like what CEO Howard Schultz is doing and the overall direction of Starbucks’ growth story.

A strong third quarter earnings report simply highlights the power of one of the best pure plays in global growth in the Restaurants sector. Cyclical factors, like improving coffee pricing, only add to the momentum as SBUX continues to push into new food and beverage segments in China and across the globe.

TROW – Financials Sector Head Josh Steiner and colleague Jonathan Casteleyn have moved shares of T Rowe Price (TROW) onto Hedgeye's best ideas list as a core holding. Simply put, we would buy and hold shares of TROW as we expect the company to benefit from the ongoing theme of a reallocation out of bonds with investors continuing to move into stocks.

T Rowe is one of the fastest growing equity asset managers and has consistently had the best performing stock funds over the past 10 years. With a disciplined process of carefully selecting the most talented investment professionals and producing and protecting the industry’s best stock performance, this allows TROW to consistently generate new inflow into its stock funds. The company has only had 3 quarterly outflows of client assets in the past 11 years which is an unmatched track record in the investment management industry.

With another good year of performance in the making, and a broader macro theme of bond fund flow in decline with an ongoing handoff to stock funds, the time is right for this leading equity fund manager and its investors to outperform.

WWW – Ask any investor in retail for the most hated stock, and most will say JC Penney. Others will say Sears. When asked who rounds out the top three, the consensus would probably say Radio Shack. Well those people will be overlooking a little shoe company based in Rockford MI called Wolverine Worldwide.

Yes, the stock is trading at 18 times earnings, giving the impression that it is loved – but the reality is that the Hedgeye Sentiment Monitor begs to differ. Our Sentiment Monitor triangulates sell-side ratings, buy-side short interest, and insider buying/selling and assigns a quantitative score accordingly. In WWW’s case, you can see that its current score is about 13, which means that investors are overly bearish.

A score closer to 90 (where many retailers sit today) would signify that the Street is overly bullish. Scores at the high and low end have both proven to be contra-indicators, meaning that overly bearish scores (like we have with WWW today) often leads to sell-side upgrades, short covering, and insider buys. While our positive stance on WWW is based on a longer-term fundamental view, this analysis certainly supports our positioning.

PLAYING IT FROM THE SHORT SIDE...

Editor's note: This week, instead of our usual Macro Report, Sector Spotlight and Investing Term, we're trying something different. While we know most of you are long-only investors, we wanted to give you a peek into research on some short ideas that we provide for our institutional clients. These stock ideas from Hedgeye Sector Heads provide a deep research dive into shares of companies and markets we believe are poised to decline in value. Our team here at Hedgeye enjoys a successful track record on the long and short side and is dedicated to unlocking value on both for our clients.

This week's first short idea comes from our Financials Team led by Josh Steiner and Jonathan Casteleyn. Please note that this note was originally published on August 15th.

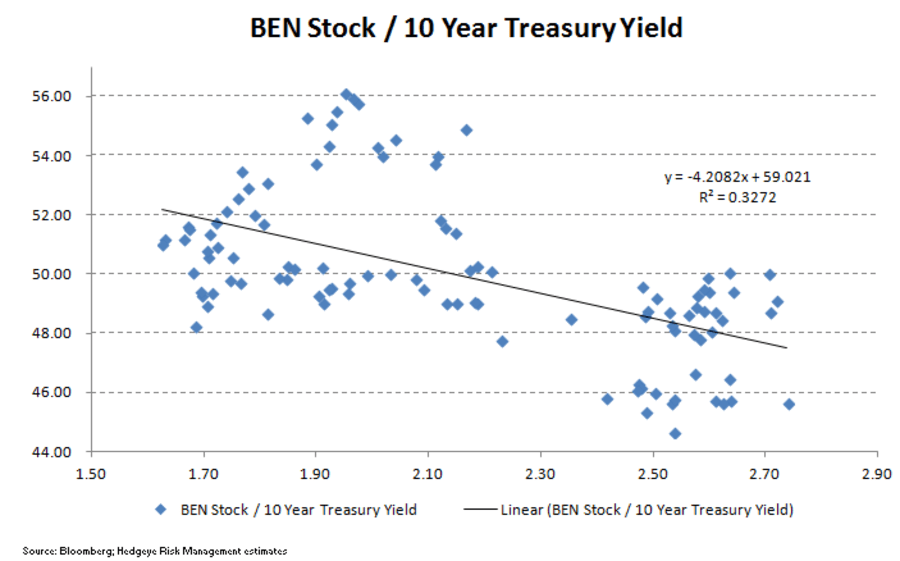

BEN Stock Starting to Track the 10 Year Bond Yield

Franklin Resources (BEN) - This is our favorite short idea in the group with its disproportionate exposure to both fixed income and retail investors (our least favorite exposures). When looking at BEN stock and the recent trajectory of the 10 year Treasury yield, the two variables appear to be tracking each other very closely. The 10 year Treasury yield bottomed on May 2nd at 1.63% which was also the recent high in BEN stock two weeks later on May 17th at over $56 per share.

Since these closely grouped two week peaks, the substantial rise in the 10 year Treasury has marked a requisite decline in Franklin stock with a similar trajectory. In our chart below we have inverted the 10 year Treasury axis in order to simply show the relationship, but in beginning of July the slight rally in the 10 year also spurred a relief rally in shares of BEN which moved from near $45 per share to over $50 per share.

Interestingly the recent further sell off in Treasuries from 2.59% to 2.72% as of last night has also been in concert with BEN shares moving from over $50 to back near the $48 per share range. While the R-squared of the two variables isn't overly compelling at 0.32, the regression of daily 10 year Treasury yields and BEN stock would imply a near term trajectory to $46 per share for Franklin shares if the U.S. 10 year goes through a 3% yield. As more daily data comes in, this relationship may become more compelling, but it is just an initial observation for now.

Separating the Forest From the Trees In Emerging Markets

Our next short idea has worked out rather well since Hedgeye first began beating the drum. Our Macro Team believes that further appreciable downside remains here (and obviously upside for those on the short side).

Please click here for access to this Hedgeye idea.

Tying Two Rocks Together: The LINN/BRY Merger

Our final short idea comes from Hedgeye Jedi Kevin Kaiser who heads up our Energy research. Kevin is a focused, no-nonsense sort of guy who smelled smoke in LINN Energy's (LINE) accounting practices, called it out and stood strong as investors long the stock fought back tooth and nail. Of course, the accounting smoke eventually led to fire in LINN's stock following news of an SEC inquiry. You may have read about his research in Barron's.

Please click here to access Kaiser's detailed research on why the stock has room to fall even further.