TODAY’S S&P 500 SET-UP – August 21, 2013

As we look at today's setup for the S&P 500, the range is 32 points or 0.63% downside to 1642 and 1.31% upside to 1674.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.48 from 2.48

- VIX closed at 14.91 1 day percent change of -1.26%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Aug. 16 (prior -4.7%)

- 10am: Existing Home Sales, July, est. 5.15m (prior 5.08m)

- 10:30am: DOE Energy Inventories

- 2pm: Release of FOMC minutes from July 30-31 meeting

GOVERNMENT:

- SEC could vote to introduce legislation requiring cos. to disclose how much more CEOs are paid than rank-and-file workers

- 9am: Former FDIC Chairman Sheila Bair, PIMCO CEO Mohamed El-Erian discuss U.S. economy

- 2pm: FOMC releases minutes from July 30-31 meeting

- Obama meets on Egypt aid cutoff as lawmakers demand action

WHAT TO WATCH:

- Goldman said to send client requests to exchanges in error

- J&J said to weigh $3b settlement of its hip implant cases

- Disgruntled investors eyeing Falcone’s holding co., NYP says

- JPMorgan said to be near selection of 2 new directors: Reuters

- Apple said to add music videos from Vevo to expand TV content

- Office Depot and Starboard agree to settlement on board

- Kodak bankruptcy reorganization approved by N.Y. judge

- Subway targets Europe w/as many as 1,000 new outlets in 2014

- New China Trust said to withdraw ILFC bid on regulator ties

- Facebook’s Zuckerberg seeks universal Internet access

- Perry Capital said to build Herbalife stake opposed to Ackman

- Disney to shutter 10-yr-old Toontown online multiplayer game

- AT&T sued on refusal to carry Al Jazeera cable network in U.S.

- Apple iPad’s China mkt share slumps as Samsung tablets gain

- APA needs to study Envestra finances before making any new bid

- Toyota’s Lexus Marque to open luxury stores in branding push

- China Telecom posts 2nd-straight profit gain on iPhone boost

EARNINGS:

- AFC Enterprises (AFCE) 5pm, $0.31

- American Eagle Outfitters (AEO) 8am, $0.10

- Eaton Vance (EV) 9am, $0.54

- Energy XXI Bermuda (EXXI) 7am, $0.47

- Hain Celestial Group (HAIN) 4pm, $0.62

- Hewlett-Packard (HPQ) 4:04pm, $0.86 - Preview

- JM Smucker (SJM) 7am, $1.20

- L Brands (LTD) 4:30pm, $0.60

- Lowe’s (LOW) 6am, $0.79 - Preview

- Madison Square Garden (MSG) 7:30am, $0.32

- PetSmart (PETM) Bef-mkt, $0.86

- Prospect Capital (PSEC) 4:03pm, $0.30

- Sears Canada (SCC CN) 7am, C$0.23

- Semtech (SMTC) 4:03pm, $0.51

- Staples (SPLS) 6am, $0.18

- Synopsys (SNPS) 4:05pm, $0.54

- Target (TGT) 7:30am, $0.95 - Preview

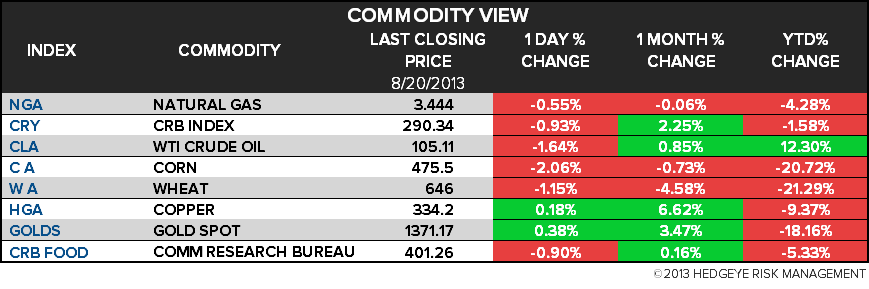

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Trades Near One-Week Low on Fed Speculation, Libya Restarts

- China Gold-Mine Deals at Record After Price Plunge: Commodities

- Gold Falls as Investors Await Fed Minutes for Stimulus Outlook

- Corn Retreats for Second Day on Higher Yields; Soybeans Decline

- Copper Falls as Chinese Manufacturing Seen Continuing to Shrink

- China Copper Imports Touch 10-Month High on Premium, Arbitrage

- Japan Watchdog as Tepco Doubter Warns of More Leaks at Fukushima

- Gold in India May Climb to Record in a Month: Technical Analysis

- Sugar, Coffee Fall on Emerging Market Currencies; Cocoa Slides

- China Platinum Imports Grow 20% Yoy on Supply Concerns: BI Chart

- Cocoa Deliveries in Brazil’s Bahia Decrease 1.6%, Hartmann Says

- Kenya Fights Off Port Competition With $13 Billion Plan: Freight

- North Sea Output May Slide as Much as 22% in 2013 on Maintenance

- Rebar Declines as China Punishes Banks for Some Steel Loans

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team