This note was originally published August 13, 2013 at 16:55 in Financials

Affordability Sinks, but Likely Will Sink Much Further Before the Current Rally Gives Way

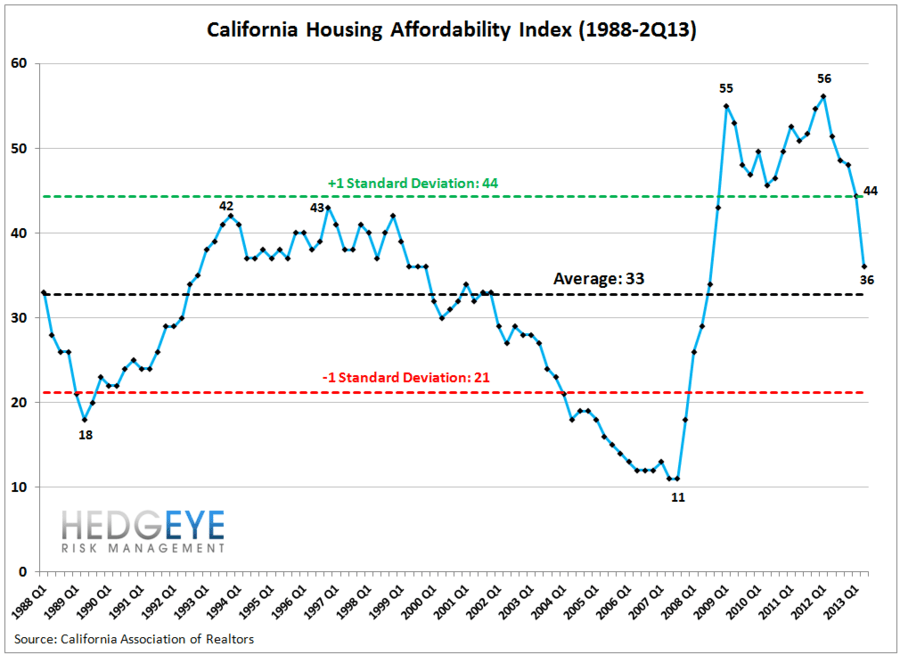

Yesterday, the California Association of Realtors released its 2Q13 housing affordability index, which showed that affordability in the state declined to 36 from 44 QoQ. The index reading corresponds to the percentage of households in the state that could afford the median priced home based on current home prices and interest rates. We were admittedly surprised to see how large the drop was Q/Q. In fact, the 8-point sequential decline from 44 to 36 was the largest decline recorded in the history of the series, which dates back 25 years to the start of 1988. It was also the largest YoY decline in affordability at 15 points.

Most observers would argue that this is likely bad news for housing, and we're not going to dispute the fact that dimished affordability reduces the longer-term upside potential for both home prices and housing-levered equities. That said, we think it's equally important to note the autocorrelation of the affordability data. Affordability tends to exhibit long-dated boom/bust cycles rising or falling until the point at which it is at least one and up to two standard deviations overbought or oversold.

Currently, we are 0.28 standard deviations oversold en route to being 1-2 standard deviations overbought. This suggests that in spite of the run we've seen thus far, and the significant Q/Q drop in affordability, there is still considerable room for further upside in either home prices, interest rates or, most likely, a combination of the two.

On a national basis, US housing affordability declined to 60 from 65 Q/Q in the second quarter. Obviously, housing nationally is far more affordable than in the state of California, but we like to use CA because it has historically been a great proxy for the market as a whole.

Joshua Steiner, CFA

203-562-6500

jsteiner@hedgeye.com

Jonathan Casteleyn, CFA, CMT

203-562-6500

jcasteleyn@hedgeye.com