In looking at Tiffany's 1st quarter results there were no big surprises. Sales, margins, and expenses were all largely in-line with expectations. EPS was $0.20, a penny below the Street, but that really shouldn't matter at this point. This is a quarter to tuck away and forget about. Domestic same-store sales declined by 34%, a combination of a 42% decline in the NY flagship and a 32% decline for the remainder of the US. Anyone paying attention to the luxury segment and other big-ticket discretionary categories should not be surprised by such large declines. Instead, we're focusing on a few subtle changes on the margin that came out of the quarter.

- 73% of TIF's EBIT comes from the US and Japan and we're encouraged to see an uptick in the sales trend in these markets. It's always risky to call an exact bottom, but this certainly looks like one to us.

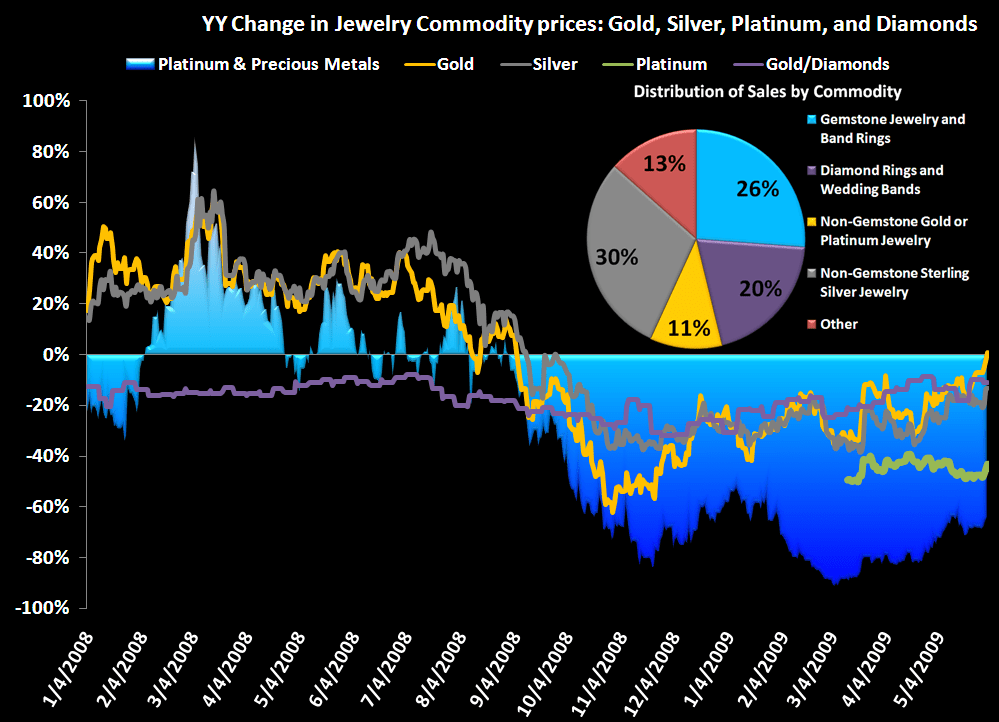

- With just under 50% of Tiffany's products containing a diamond of some sort, it is worth noting that diamond pricing has reversed dramatically in the past 6 months. We are now back to pricing levels of a couple of years ago. It will take some time for inventory turns to work through higher cost raw materials, but this reversal should help gross margins at the end of 2009 and throughout 2010.

- The recent and severe weakening of the U.S dollar should help TIF in the near-term, beyond the Street expectations. Let's be clear - the Dollar crashing does not end well for any of us, and we are not expecting tourists to return to 5th Avenue in droves, but this trend should help mitigate the fairly large FX translation impact we saw in 1Q.

- Consolidation has been a key theme of ours and the high-end jewelry market is a great example. With few national brands, if any that compare to Tiffany, there has been an increasing wave of store closures and bankruptcies. Inherent in the jewelry business is a high cost to fund inventory and only those with strong balance sheets will survive.

- Lastly, TIF's triangulation of sales, margins and inventories are improving on the margin. Check out the SIGMA chart below. 1Q is sitting in the lower left quadrant, and it is unlikely it will remain there for more than 1 more quarter. ANY move out of that quadrant is a positive stock move.

By no means are we out of the woods on the challenges facing the luxury retailer and consumer. In addition, we're not particular fans of the TIF business model (low margins and high inventory carrying costs). However, there is an increasing amount of certainty surrounding Tiffany. In our view the brand remains iconic in stature, expenses are being managed wisely and investments in the future remain in place where appropriate (store growth will be up 5-6% in '09). Importantly, management remains true to the brand and hasn't conformed to the environment. Has anyone seen the case of clearance engagement rings?

Eric Levine