Northern Tier Energy (NTI) – a variable distribution refining MLP – released 2Q13 results yesterday, with the key number being distributable cash flow (DCF) of $63MM, or $0.68/unit.

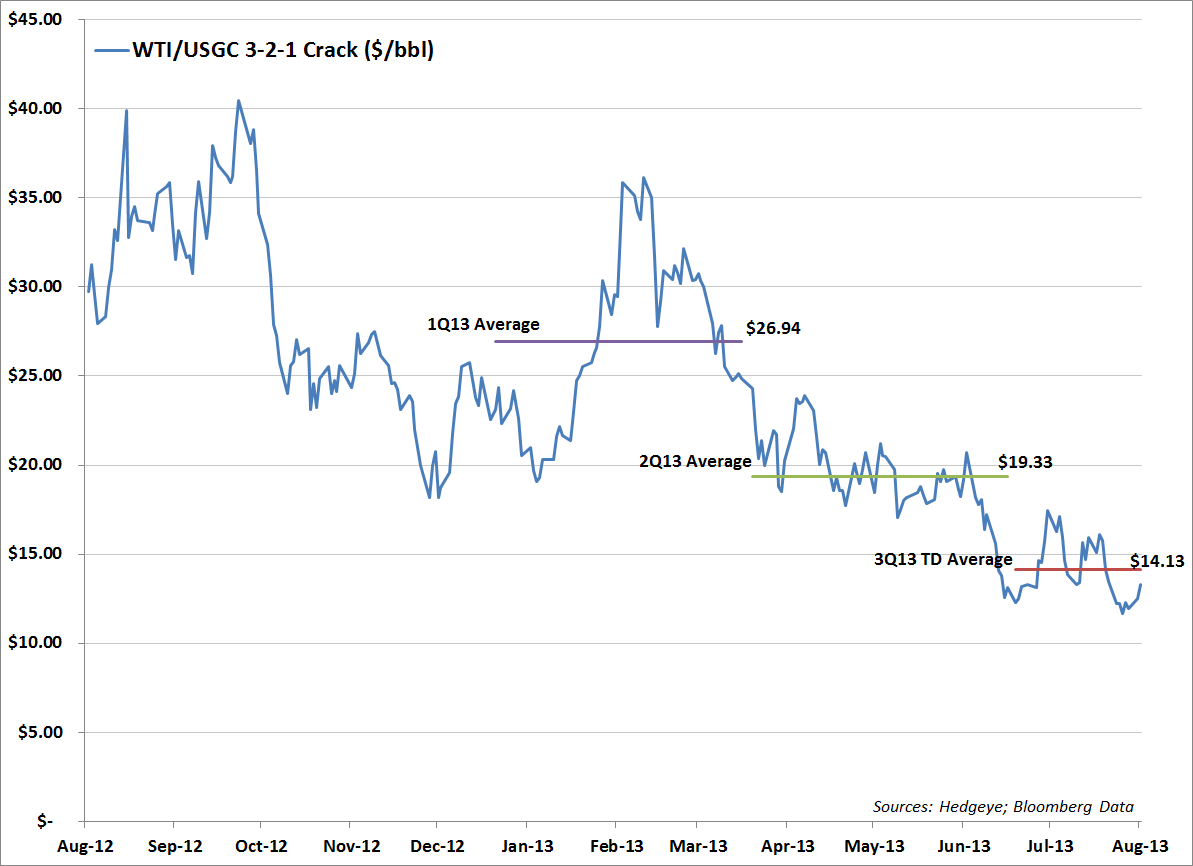

While the distribution declined 45% from 1Q13, the result was better-than-expected considering the collapse in the 3-2-1 crack (see chart below) and the fact that throughput was down 35% QoQ due to a planned turnaround at the Company’s lone refinery in St. Paul, MN.

This was a nice result for the General Partner (GP), and, coincidentally (or not), NTI announced after yesterday’s close that the GP (indirectly owned by ACON Refining, TPG, and NTI’s CEO) would sell another 11.5MM units (plus a 1.75MM underwriter’s option) to the public. So far in 2013, the GP has sold 37MM units (including the deal announced yesterday), ~61% of its stake as of YE12 and ~40% of the total units out.

In our view, NTI may have played some games in the quarter to boost the distribution above what it otherwise would have been.

First, NTI did not take a reserve for turnaround expenses in the quarter. NTI adds back actual turnaround expenses to DCF, but typically deducts a reserve for it each quarter so that there are not large, spurious declines in DCF owing to turnarounds (this makes sense if NTI is actually consistent with this process). In each of 3Q12, 4Q12, and 1Q13 NTI deducted $10.0MM from DCF to reserve for turnaround expenses. This quarter NTI reserved $0.0. As a result, NTI is currently under-reserved for turnaround expenses by $18.1MM, having reserved $30.0MM but spent $48.1MM in the quarters since coming public.

On the conference call, management noted that they will again begin reserving for turnaround expenses in 3Q13.

The second curious item in the quarter is that capital expenditures deducted from DCF ("maintenance" and "regulatory" capex) came in at $13.5MM, 37% below the guidance of $21.3MM. This was not a “beat.” These capital expenditures were pushed out into future periods (or possibly considered expansion capex?). Capital expenditures not deducted from DCF ("expansion" capex) came in at $28.9MM, $11.1MM above the guidance of $17.8MM. In short, total capex was above guidance, the capex deducted from DCF was below guidance, and the capex not deducted from DCF was way above guidance. That's a little suspect, in our view.

These two items alone increased DCF in 2Q13 by ~$17.8MM ($0.19/unit), or 28%.

We were wondering yesterday why NTI would do this – after all, it is a variable distribution MLP (it shouldn’t be trying to smooth DCF). But the announcement of the GP selling after yesterday’s close has given us a clue...

We think that NTI has now set itself up for even worse 2H13, beyond the collapse in refining margin (see chart), due to these moves to boost the distribution in 2Q13. The maintenance and regulatory capital projects got pushed back and the Company will again be reserving for turnaround expenses to make up the delta between what’s been reserved for and what’s been spent ($18.1MM). The manufactured DCF gains in 2Q13 will be DCF losses in future periods.

Kevin Kaiser

Senior Analyst