Conclusion: Today’s Retail Sales and Small Business Confidence numbers were solid, extending the trend of broad improvement observed across the balance of the domestic macro over the last two quarters and offering some positive confirmation of the early 3Q13 strength signaled by the Labor Market and ISM figures for July.

--------------------------------------------------------------------------------------------------------------

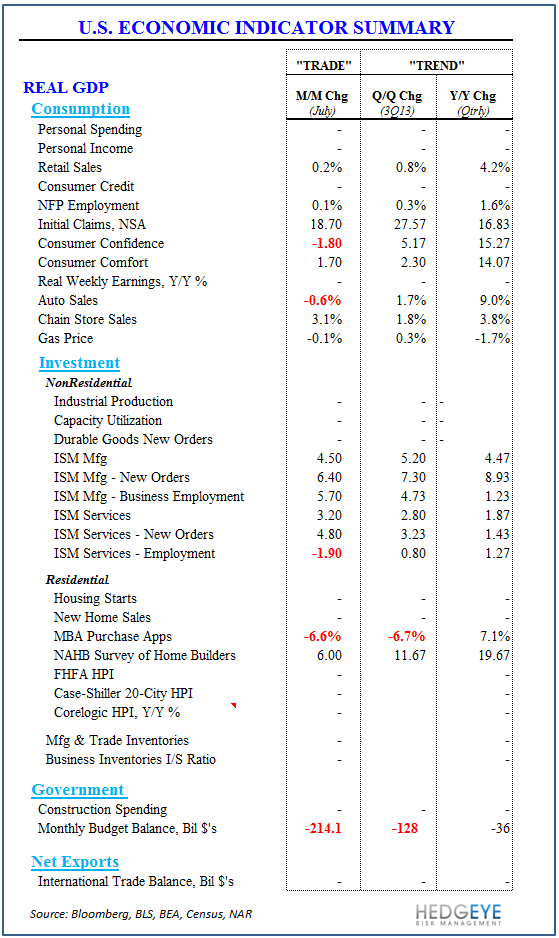

U.S. MACRO - Solid Start to 3Q13: The Labor Market (initial claims) continued to show accelerating improvement in July while the ISM manufacturing and services surveys reflected a broad recovery off the lackluster activity that characterized the April-June period.

As can be seen in the Economic Indicator Summary Table below, 3Q13 has started off solid with the preponderance of growth/activity indicators released thus far showing improvement on both a TRADE & TREND basis. On balance, the July Macro releases have come in ahead of expectations according the Citi and Bloomberg Economic Surprise Indices.

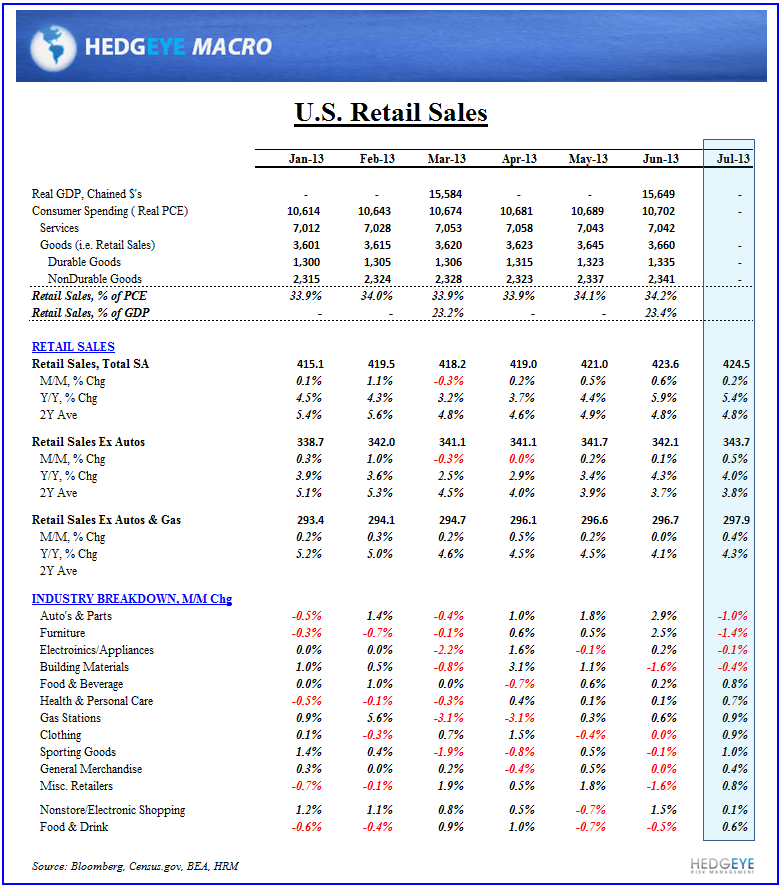

RETAIL SALES: Monthly Retail sales are volatile, subject to notoriously large revision, and reported in nominal dollars but, still, it’s hard to ignore a component responsible for roughly a third and a quarter of PCE and GDP, respectively.

The first read on consumer spending in 3Q13 came in healthy with July Retail sales ex-Autos accelerating to 0.5% MoM (vs. 0.1% in June) while Sales excluding Autos & Gas accelerated to +0.4% MoM (vs. 0.0% in June).

On a year-over-year basis, growth slowed modestly across each of the primary aggregates with Total Retail Sales, Sales ex-Autos, and Sales ex-Auto’s and Gas slowing 50bps, 30bps, and 40bps, respectively. On a 2Y basis, however, all three measures accelerated modestly in July.

All in, not a game changer or positioning catalyst, but a positive update for consumer spending to start the third quarter.

We’ll be interested to see the Personal Income data for July (8/30 Release) and the impact of the furloughing of federal workers on aggregate disposable income growth – which has been treading water at a lackluster ~+2% YoY. As a reminder, we expect income growth for federal workers (~2% of the total workforce) to grow approx -7% over the balance of the fiscal year due to the combination of furloughs and employment declines. The impacts, while moderate, should constrain the upside in disposable income growth and consumer spending in 3Q13.

NFIB Small Business Optimism: The NFIB Small Business Optimism Index climbed to 94.1 in July from 93.5 in June. Under the hood, the outlook for general business conditions deteriorated sequentially although (somewhat incongruously) hiring plans, sales expectations, and job openings all advanced.

The directional TREND in the consumer and business confidence metrics provides a better read on sentiment than any one data point in isolation and the larger trend in small business confidence remains positive and in agreement with the ongoing advance in the lead measures of consumer confidence.

With labor, credit, and confidence trends all showing ongoing improvement and with a diminishing fiscal drag and easier comps as we annualize sequestration and the tax law changes into 2014, the growth dynamics for the U.S. economy, and prospects for the U.S. Dollar and U.S equities remains favorable. Consumption growth faces some constraints in the near term and congress will likely re-emerge as a negative catalyst in some form in the coming weeks, but, fundamentally the data continues to support a constructive outlook for domestic growth

Christian B. Drake

Senior Analyst