Summary bullets:

- LINE, LNCO remains a “Best Idea” short for us. Poor 2Q13 results strengthen our conviction in that call.

- No material update on the ongoing SEC inquiry or the pending BRY merger;

- Production, adjusted EBITDA, DCF all miss guidance, and it would have been worse if not for some low quality earnings;

- Total capital capex surprised to the upside, and the gap between total capex and maintenance capex grows wider, despite no production growth;

- 2H13 guidance for production, adjusted EBITDA, DCF all cut;

- 2H13 guidance assumes strong NGL prices and realizations – that optimism seems misplaced.

Mum is the word on SEC inquiry and BRY merger…..No real direction on the SEC inquiry or the BRY merger in the conference call or in the new 10-Q or S-4/A. There is no longer a guided closing period for the merger in the S-4/A, and there are several new risk factors to the merger. We find it strange that LINN said yesterday morning (8/8) that its S-4/A would be filed with the SEC yesterday “afternoon” (8/8), though it wasn’t filed until early this morning (8/9). Why the delay? We don't know, but we find it odd... We highlight some key changes and additions to the risk factors and disclosures in the 10-Q and new S-4 in the appendix of this note.

On the 2Q13 results……Hard to find positives here. Production of 780 MMcfe/d was at the low end of guidance, 780 - 820 MMcfe/d, and down 2% QoQ. Adjusted EBITDA of $378MM missed guidance by 4% and DCF missed guidance by 10%. Distribution coverage was 0.89x vs. guidance of 1.00x. And the results were low quality, as other revenues, natural gas marketing margin, and an anomalous drop in taxes other than income increased DCF by $15 – 20MM. Further, premiums paid on settled derivatives in the period were $43MM. Excluding those costs boosted DCF by 28%. Backing out premiums paid and other special items, we arrive at our own non-GAAP numbers: EPU of $0.05, FCF/unit of -$0.44, CF/unit of $1.01, and Open EBITDA of $310MM.

On downward revisions to 2H12 guidance……LINN cut 2H12 production guidance (from the April 25th guidance) by 2%, oil production guidance by 4%, adjusted EBITDA by 6%, and DCF by 15%. Distribution coverage drops to 0.90x from the prior guidance of 1.06x. We note the $22.5MM increase to 2H13 non-GAAP (cash) G&A guidance. On page 50 of the 10-Q we read, “Our legal expenses incurred in defending the lawsuits and responding to the SEC inquiry have been significant and we expect them to continue to be significant in the future.” I guess LINN’s lawyers don’t take unit-based comp?

Total capital expenditures surprise to upside……Total capital expenditures in 2Q13 were $338MM (development capital + purchases of other PP&E + joint venture funding, per the cash flow statement), up from $277MM in 1Q13. We consider this QoQ increase of $66MM a large surprise to the upside, especially considering the 1% drop in production QoQ. Further, CEO Mark Ellis answered this question incorrectly on the conference call:

Analyst: “And just last one for me, and I’m sorry if I may have missed this, but how much total CapEx was spent this quarter?”

CEO Mark Ellis: “I don’t have that number off the top of my head, hang on one sec.” [15 second delay] “$260 million.”

The 10-Q (which we did not have when Mr. Ellis made this statement) plainly states on page 22 that for 2Q13, “capital expenditures, excluding acquisitions, of approximately $334 million” ($4MM delta between that and the CF statement is an accrual issue). Mr. Ellis’ answer on the call was materially incorrect.

Total capex vs. maintenance capex vs. production growth……In 2Q13, total capex including JV funding exceeded maintenance capex by $226MM, with pro forma production down 1% QoQ. Over the TTM, total capex including JV funding has exceeded maintenance capex by $875MM ($219MM/quarter!) with no organic production growth to speak of. In fact, by our estimates, pro forma organic production in 2Q13 was down 5% from the 3Q12 average. We believe that LINN’s maintenance capex is massively understated; if it was at an appropriate level, all of DCF would be wiped out.

Understated maintenance capex is not a TX Hogshooter problem……LINN’s comments on the 2Q13 call suggest that the explanation for the delta between total capex and maintenance capex, +$200MM/quarter, coupled with production flat-to-down, is largely because of its disappointing TX Hogshooter program in 2012 and 1Q13. LINN drilled 28 gross Hogshooter wells on the TX side of the border; management noted that 14 of those wells underperformed expectations. LINN stated on the 1Q13 conference call that its working interest in those wells was 60% on average, so 8.4 net wells underperformed. At $8.5MM/well, that is $71MM of capital that underperformed. Spreading that out of 5 quarters, gets us to $14MM/quarter, or ~6% of the difference between total capex and maintenance capex. This is not a TX Hogshooter issue, and the issue is not going away.

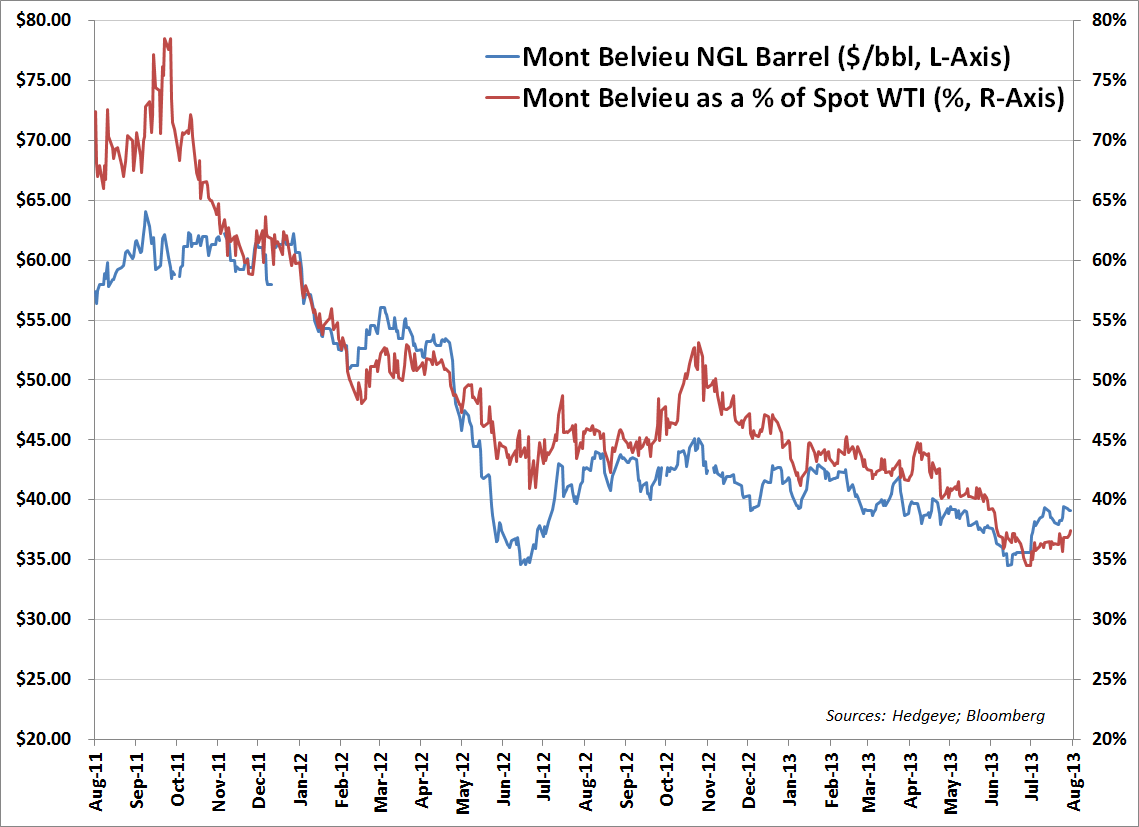

NGL price optimism is misplaced……LINN’s realized NGL price in 2Q13 was $26.69/bbl, which was 70% of the Mont Belvieu benchmark NGL price in the quarter, $38.00/bbl. LINN’s guidance for 2H13 NGL price is $33.00/bbl, suggesting a material improvement in realized NGL prices. As we show in the two charts below, that optimism seems misplaced. Ethane – particularly Jonah Field ethane that is priced at Conway – is at rejection levels, as it has been for more than a year. And the NGL barrel price at Mont Belvieu today is at $39.00/bbl, only $1/bbl higher than the 2Q13 average. In our view, current NGL prices suggest a realized NGL price for LINN in 2H13 around $27 - $28/bbl. As LINN will produce ~5.0 MMbbls of NGLs in 2H13, LINN could be guiding DCF $25MM - $30MM ($0.11 - $0.13/unit) too high. Recall that LINN does not have NGL hedges.

Peculiar drop in taxes other than income……Taxes other than income taxes (production taxes) in 2Q13 were $32.3MM, 6.6% of revenues, and $0.46/Mcfe; that was 26% below guidance of $44MM. It is an also an outlier relative to prior periods (in 2012 production taxes were 8.2% of revenues and $0.54/Mcfe, and in 1Q13 production taxes were 8.6% of revenues and $0.55/Mcfe) and forward guidance (3Q13 guidance is for production taxes to jump back up to $48MM, or $0.64/boe). This could be the one-time item: “Ad valorem taxes, which are based on the value of reserves and production equipment and vary by location, decreased by approximately $2 million compared to the three months ended June 30, 2012, primarily due to an adjustment related to the properties acquired in the Green River Basin region partially offset by taxes associated with property acquisitions in 2012 and higher rates on the Company’s base properties” (2Q13 10-Q, page 28).

Peculiar increase in other revenues and natural gas marketing margin……Other revenues and natural gas marketing margin came in at $14.5MM in 2Q13, up $7MM QoQ and $7MM (94%) ahead of guidance. Another low quality source of DCF in the quarter.

LINN ramps up in the Jonah, likes the OK Hogshooter, has high hopes for HZ Wolfcamp……LINN plans to ramp up drilling activity in the Jonah Field in 2H13, and that will drive the back half production growth. The fact that they are ramping back up in this gas/NGL play now says a lot about the asset base on the whole. Seems like a desperate attempt at production growth – and not returns – to us…….LINN was quite bullish on the OK Hogshooter on the call, but we wonder if that’s optimism is justified. The Company has drilled only 9 gross (~4 net) wells, will not give us a 30d rate, but did say that the wells have an 80 – 85% initial decline (which is quite high, in our view). We thinks its a bit early to sing the praises of this play……LINN also noted that it has Permian acreage prospective for the HZ Wolfcamp; it will participate in four non-op wells “with a pretty small working interest” and drill one operated well in 2H13. No well results expected before 1Q14. We don't consider it material to the stock at this time.

Kevin Kaiser

Senior Analyst

APPENDIX: New disclosures worth reading…..

On BRY merger risk, 10-Q page 50: “Due to the pending SEC inquiry, the timing of LinnCo’s pending merger with Berry is uncertain. If the merger is not completed, or there are delays in completing the merger, our unit price and our business could be adversely affected and we would be subject to a number of risks…”

On premiums paid, 10-Q page 42: “The premiums paid for put options that settled during the three months ended June 30, 2013, and June 30, 2012, and during the six months ended June 30, 2013, and June 30, 2012, were approximately $43 million, $36 million, $86 million and $62 million, respectively. Deducting the premiums paid for put options would reduce the Company’s adjusted EBITDA and DCF; however, the Company pays cash for put options at the time of execution and no additional amounts are payable in the future under the contracts. Therefore, the Company’s calculation of adjusted EBITDA and DCF is more representative of the cash available for distribution during the period. The Company considers the cost of premiums paid for put options as an investment related to its underlying oil and natural gas properties only for the purpose of calculating the non-GAAP financial measures of adjusted EBITDA and DCF.”

On maintenance capex, 10-Q page 43 (our emphasis): “Maintenance capital expenditures, a component of total capital expenditures, is a non-GAAP calculation established at the beginning of each calendar year that represents the estimated capital investment required to approximately maintain production levels from the prior year and replace proved developed producing reserves that are forecasted to be produced as a result of maintaining production levels from the prior year. Management makes estimates of maintenance capital expenditures as part of the annual budget process, ranks the most efficient projects by production replacement and proved developed producing reserves replacement and allocates the total planned expenditures across the four quarters of each calendar year. While the Company believes its estimates and assumptions to be reasonable under the circumstances, they are subject to, among other things, risks and uncertainties including production rates, reserve quantities and capital costs estimates. At the end of each calendar year, the Company evaluates the performance of its annual capital program, re-ranks its most efficient projects and incorporates the results of this analysis in its subsequent calendar year estimated maintenance capital expenditures. The calculation includes the cost to convert nonproducing reserves to producing status and does not include the initial cost to acquire the underlying asset as that amount has already been spent in a prior period and therefore does not impact the ability to make distributions in future periods.”

On maintenance capex, 10-Q page 50: “ If we underestimate the appropriate level of estimated maintenance capital expenditures or the estimated maintenance capital expenditures do not produce the expected results, we may have less cash available for distribution in future periods when adjustments from the previous year are included in future estimates. Over time, if we do not set aside sufficient cash reserves or have available sufficient sources of financing and make sufficient expenditures to maintain our asset base, we may be unable to pay distributions at the anticipated level and could be required to reduce our distributions.”

On NGLs, 10-Q page 49: “We have been and continue to be limited in our ability to effectively hedge our NGL production. As a result, we are subject to the current depressed price environment for NGLs, and in particular, ethane prices. If current price levels for NGLs continue into the future, our revenues and results of operations will be affected, which could result in distributable cash flow that is insufficient to maintain our current distribution to unitholders.”

On put options, 10-Q page 46: “In certain historical periods, the Company paid an incremental premium to increase the fixed price floors on existing put options because the Company typically hedges multiple years in advance and in some cases commodity prices had increased significantly beyond the initial hedge prices. As a result, the Company determined that the existing put option strike prices did not provide reasonable downside protection in the context of the current market.”

On merger tax implications, S-4/A page 179 (our emphasis): “As a result of the anticipated increase in tax liability due to the remedial allocation, LINN has agreed to pay LinnCo $6 million per year for three years (2013, 2014 and 2015). The $18 million to be paid during this period is expected to compensate LinnCo for a portion of the increase in its total tax liability with respect to the assets acquired in the Contribution, and is not intended to fully compensate LinnCo for the increased total tax liability. The total tax liability generated from the remedial allocation will be recognized over the remaining life of the underlying assets, which could extend beyond 50 years. The total deferred income tax liability impact from the transactions is estimated to be approximately $452 million (included in the total approximate $477 million deferred income tax liability shown on the pro forma condensed combined balance sheet). This tax liability will be partially deferred when considering the tax shield that LinnCo receives with respect to the LINN units it currently owns. If LinnCo were to sell or otherwise liquidate the LINN units acquired, the deferred tax liability of $477 million would be payable. The tax shield and other factors were considered by the conflicts committees of both LINN and LinnCo in negotiating the compensation to be paid by LINN to LinnCo for LinnCo’s tax liability.

“Under the Contribution Agreement, LINN and LinnCo have agreed (i) to work in good faith at the end of each of calendar year 2014 and 2015 to evaluate whether the amount distributed to LinnCo as discussed above has reasonably compensated LinnCo for the actual increase in tax liability to LinnCo, if any, resulting from the allocation of amortization, depletion, depreciation and other cost recovery deductions using the “remedial allocation method” pursuant to Treasury Regulations Section 1.704-3(d), with respect to the assets acquired in the Contribution and (ii) to make any adjustment to such distribution as mutually agreed. The total tax benefit that LINN expects to realize from this transaction, undiscounted, is approximately $1.4 billion (purchase price times 38%) of additional depreciation, depletion and amortization that will be recognized on a unit-of-production basis over the remaining life of the property. Based on its pro forma ownership percentage, approximately one third of the approximate $1.4 billion total undiscounted tax benefit will be allocated to LinnCo.”