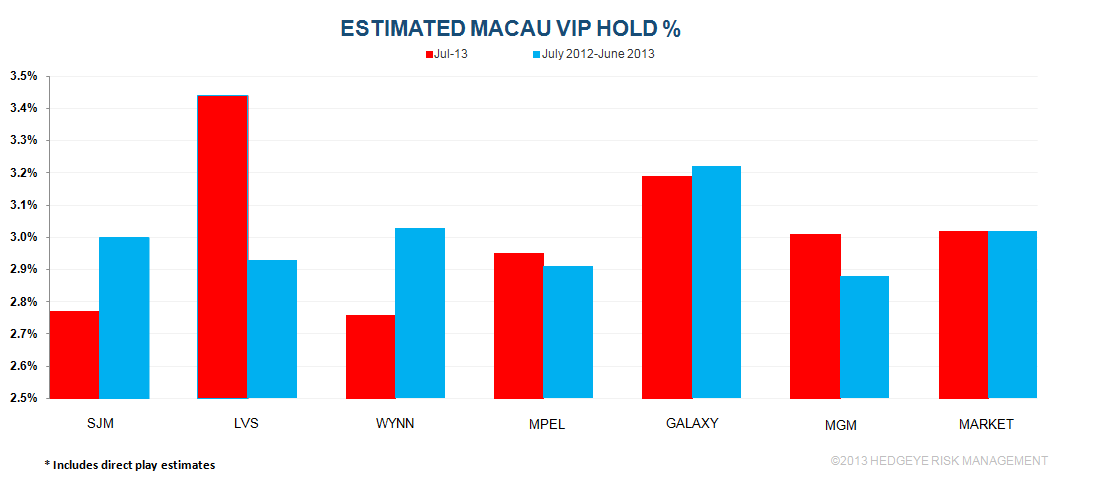

July GGR grew 20% YoY to HK$28.63 billion (US$ 3.69 billion). Volumes were the driver of the strength and all segments performed well. Mass, VIP, and slot revenues increased 32%, 16%, and 11%, respectively. VIP hold percentage was normal versus slightly below normal hold percentage in July 2012. We estimate that including direct play, VIP hold was 3.02% versus a normalized 3.00%. With normal VIP hold in both periods, GGR growth would have been 17%.

Here is the detail:

YOY TABLE OBSERVATIONS

Total table revenue grew 20% YoY. Mass market growth continued its streak of around 30% growth rate, up 32% in July. VIP volume rose 12% while VIP revenue gained 16%.

LVS

Table win grew 28%, lead by 96% growth at SCC. Mass revs remained strong at 43% while VIP RC grew 15%. Including direct play, we estimate that LVS held at 3.4% in July compared to 3.3% last July, assuming direct play of 16% vs. 22% last year.

- Sands climbed 9%

- Mass grew a meager 3%, lowest growth since August 2012

- VIP revenue rose 15%

- Sands held at 3.4% vs 2.8% in the same period last year. We assume 10% direct play in July vs 8% in July 2012.

- Junket RC fell 9%

- Venetian grew 7%

- Mass increased 21%

- VIP revenue fell 5%

- Junket VIP RC gained 8%

- Assuming 28% direct play, hold was 3.3% compared to 3.7% in July 2012, assuming 30% direct play

- Four Seasons gained 14%

- Mass revenue gained 30%

- VIP revenue grew 11% but Junket VIP RC declined 10%. July hold (assuming 15% direct play) was 3.7% vs 3.0% in July 2012 when direct play was 16%.

- Sands Cotai Central rocketed 96% higher

- Mass jumped 183% to $104MM, a new monthly high

- VIP revenues grew 63%

- Junket RC volume of $4.3BN, up 64% YoY

- If we assume that direct play was 10%, hold would have been 3.4%

MPEL

MPEL gained 20% in table revenues. Mass continued to be white-hot at 58% (1st in the market) while VIP growth was 7%. We estimate that MPEL held at 3.0% vs 2.9% last July. Estimated direct play was 10%, in-line with last year.

- Altira table revenues grew 4%. Mass and VIP both rose 4%

- VIP RC declined 1%

- We estimate that hold was 2.7%, compared to 2.5% in the prior year

- CoD table revenues grew 26% YoY

- Mass increased 67%, continuing its impressive streak of strong YoY double-digit gains since the property opened

- VIP win grew 8% and RC grew 10%

- Assuming a 14% direct play level, hold was 3.1% in July compared to 3.1% last year (assuming 15% direct play)

WYNN

Wynn table revenues grew 8%, the worst performer in the market

- VIP revenues grew 3%, while VIP RC increased 9%

- Wynn held at 2.8% (assuming direct play of 8%) vs 2.8% last July (assuming direct play of 10%)

- Mass revenues gained 29%

MGM

MGM had the strongest performance in July, growing 32% in table revenues.

- We estimate that hold was 3.0% adjusted for direct play of 7% vs hold of 2.6% last year assuming 8% direct play

- VIP RC and Mass grew 15% and 32%, respectively

GALAXY

Galaxy table revenues increased 26%. VIP revenues gained 22% while RC volumes grew 8%. On the bright side, Mass growth was strong at 40%. Hold was 3.2% in July 2013 vs. 2.9% last year.

- StarWorld table revenues rose 11%

- Mass soared 69%

- VIP gained 4%.

- Junket RC rose 7%

- Hold was 3.2% vs 2.9% last year

- Galaxy Macau's table revenues grew 43%

- Mass had another great month at 40% growth

- VIP rebounded strongly at 44% growth

- Hold was 3.4% vs 2.7% last July

SJM

Total table revenue grew 12%, with mass and VIP growth of 11% and 13%, respectively. RC volume gained 17%. SJM held at 2.8% vs 2.9% last year.

SEQUENTIAL MARKET SHARE - June to July (property specific details are for table share while company-wide statistics are calculated on total GGR, including slots):

LVS

Market share gained 240bps to 22.8%. July’s share is above its 6-month average of 21.0% and better than its 2012 average share of 19.0%.

- Sands' share was flat at 3.5%. For comparison purposes, 2012 share was 3.9% and 6M trailing average share was 3.2%.

- Mass share dropped 30bps to 5.1%

- VIP rev share was unchanged at 2.8%

- RC share was 2.3%, -10bps MoM

- Venetian’s share gained 20bps to 8.0%. 2012 share was 7.9% and 6 month trailing share was 8.3%.

- Mass share decreased 10bps to 13.4%

- VIP share was unchanged at 5.4%

- Junket RC share declined 20bps at 3.7%

- FS gained gained 130bps to 3.5%. This compares to 2012 share of 3.7% and 6M trailing average share of 2.9%.

- VIP was rocketed 170bps higher to 4.4%

- Mass share gained 70bps to 1.7%

- Junket RC gained 20bps to 3.2%

- Sands Cotai Central's table market share gained 110bps to 7.5%, which compares to the 6M trailing average share of 6.1%.

- Mass share fell 20bps to 9.2%, a new high

- VIP share climbed 150bps to 6.7%

- Junket RC share fell 30bps to 5.7%

MPEL

MPEL grew 60bps in share in July to 13.2%. Its 6 month trailing share is 14.3% and their 2012 share of 13.5%.

- Altira’s share fell 50bps to 3.3%, below its 6 month trailing and 2012 shares of 3.8%

- Mass share gained 10bps to 1.2%

- VIP lost 80bps to 4.2%

- VIP RC share gained 40bps to 4.9%

- CoD’s share fell 80bps to 9.8%, above the property’s 2012 and 6M trailing share of 9.4% and 10.3%, respectively.

- Mass market share slipped 10bps to 12.3%

- VIP share fell 120bps to 8.6%

- RC share dropped 100bps to 7.7%

WYNN

Wynn GGR share was 10.2%, flat MoM. 2012 average share was 11.9% and their 6M trailing average share has been 11.0%.

- Mass share was gained 140bps to 7.7%

- VIP share tumbled 70bps to 11.1%

- Junket RC share gained 10bps to 12.1%

MGM

MGM’s market share dropped the most among its peers - 150bps to 9.5%, below its 6M and 2012 average of 9.9%

- Mass share tumbled 140bps to 6.6%

- VIP share dropped 140bps to 10.5%

- Junket RC slipped 130bps to 10.4%

GALAXY

Galaxy's share gained 60bps to 19.9%, above its 2012 average and 6-month average share of 19.0% and 18.5%, respectively

- Galaxy Macau share improved 70bps to 11.6%

- Mass share lost 30bps to 10.3%

- VIP share improved 110bps to 12.2%

- RC share gained 90bps to 11.6%

- Starworld share was flat at 7.6%

- Mass share gained 50bps to 4.1%

- VIP share dropped 10bps to 9.2%

- RC share gained 90bps to 9.9%

SJM

SJM share lost 10bps to 24.4%, below their 2012 average of 26.7% and their 6M trailing average of 25.3%

- Mass market shares gained 10bps to 26.6%

- VIP share lost 10bps to 24.4%

- Junket RC share rose 60bps to 28.1%

Slot Revenue

Slot revenue grew 11% YoY to $154MM in June

- GALAXY had the best YoY growth at 33% to $21MM

- LVS grew 22% to $47MM

- MPEL gained 11% to $26MM

- MGM was flat at $25MM

- WYNN dropped 2% to $21MM

- SJM had the worst YoY slot performance, -5% to $14MM