TODAY’S S&P 500 SET-UP – August 5, 2013

As we look at today's setup for the S&P 500, the range is 20 points or 1.03% downside to 1692 and 0.14% upside to 1712.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.31 from 2.30

- VIX closed at 11.98 1 day percent change of -7.42%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: ISM Services Index, July, est. 53.0 (prior 52.2)

- 11am: Fed to buy $1.25b-$1.75b debt in 2036-2043 sector

- 11:30am: U.S. to sell 3M, 6M bills

- 11:45am: Fed’s Fisher speaks on economy in Portland, Ore.

- U.S. Weekly Rates Agenda

GOVERNMENT:

- Transportation Sec. Anthony Foxx, NHTSA hold event highlighting latest pedestrian fatality data, agency efforts to reverse trend of rising fatalities, 11am

- Washington Weekly Agenda

WHAT TO WATCH:

- Apple can keep selling iPhone 4 after reprieve from U.S.

- U.S. decision seen aiding cheaper iPhone push

- China services, manufacturing indicate slowdown stabilizing

- Terrorism threat extends U.S. embassy closures through Aug. 10

- CBS blackout continues on Time Warner Cable stations

- New York Times agrees to sell Boston Globe to John Henry

- Fed should reverse commodity-trading policy: CFTC’s Chilton

- MBK said in exclusive talks to buy ING’s Korean insurance unit

- California Governor Brown ends immediate threat of BART strike

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- North American M&A Agenda

- Canada Weekly Agendas: Energy, Mining

- U.S. Services, BOJ, Carney, HSBC, Rohani: Wk Ahead Aug. 5-10

EARNINGS:

- Atlas Pipeline Partners (APL) 4:35pm, $0.39

- Bristow Group (BRS) 5:05pm, $0.94

- Dun & Bradstreet (DNB) 4:15pm, $1.52

- EW Scripps (SSP) 7:30am, $0.07

- EXCO Resources (XCO) 4:01pm, $0.11

- Fidelity National Financial (FNF) 4:04pm, $0.63

- GT Advanced (GTAT) 4:15pm, $0.09

- Hologic (HOLX) 4:01pm, $0.37

- Integrys Energy Group (TEG) 5:07pm, $0.37

- Jack in the Box (JACK) 4:01pm, $0.38

- Kosmos Energy (KOS) 7am, $(0.10)

- Macerich (MAC) Aft-mkt, $0.81

- Mindray Medical Intl (MR) 5pm, $0.50

- PAA Natural Gas Storage (PNG) 4:07pm, $0.19

- Plains All American Pipeline (PAA) 4:05pm, $0.60

- ProAssurance (PRA) 4:01pm, $0.87

- Retail Properties of America (RPAI) 4:01pm, $0.23

- Rockwood (ROC) 6:28am, $0.76

- Stone Energy (SGY) 4:03pm, $0.69

- Sunstone Hotel Investors (SHO) 4:14pm, $0.30

- Tesoro Logistics (TLLP) 4:30pm, $0.47

- Tyson Foods (TSN) 7:30am, $0.60

- Unum Group (UNM) 4pm, $0.79

- Volcano (VOLC) 4:05pm, $0.00

- Vornado Realty Trust (VNO) 5:17pm, $1.21

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Fed Should Reverse Commodity-Trading Policy, CFTC’s Chilton Says

- p Commodities Market, Industry News »

- Gold Bulls Cut Wagers on Signs U.S. Growth Quickens: Commodities

- U.S. Milk Climbs as Fonterra Halt Seen Spurring Demand Elsewhere

- Corn Slumps to Lowest Since 2010 on Outlook for Record U.S. Crop

- Brent Drops a Second Day as Libya Reopens Port, Rohani Appointed

- Gold Swings Between Gains and Declines Amid Stimulus Speculation

- Copper Swings Between Gains and Drops Amid Signs of U.S. Rebound

- Palm Oil Declines as Global Cooking Oil Supplies Seen Expanding

- Shale Drillers Pull Ahead of Global Oil Giants in Profit: Energy

- Cocoa Net Long of Money Managers on Liffe Rose in Latest Week

- Port Hedland Iron Ore Exports Drop as Shipments to China Decline

- Metal Prices May Be Capped by Negative Economic Surprises

- Lab Burger Reared to Challenge Real Meat Faces Taste Test Today

- COMMODITIES DAYBOOK: Gold Bulls Cut Bets as U.S. Growth Quickens

- Rusal Says Aluminum Premiums to Stay High as LME Tackles Backlog

CURRENCIES

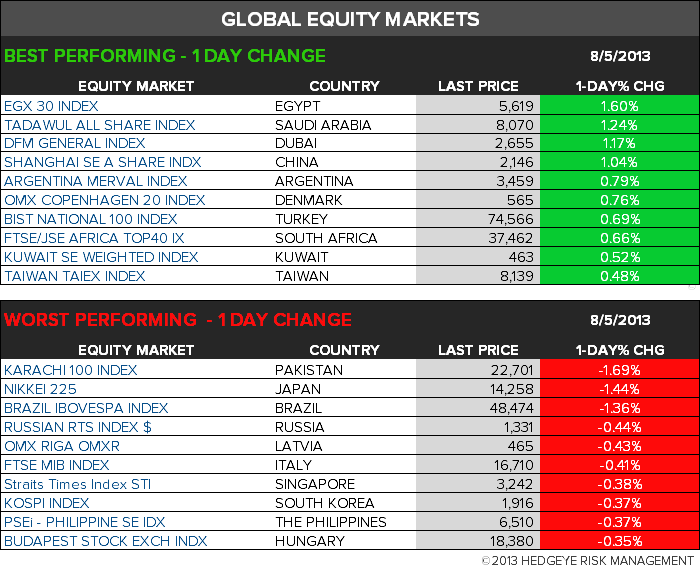

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team