TODAY’S S&P 500 SET-UP – August 2, 2013

As we look at today's setup for the S&P 500, the range is 22 points or 0.99% downside to 1690 and 0.30% upside to 1712.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.40 from 2.38

- VIX closed at 13.45 1 day percent change of 0.45%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Change in Nonfarm Payrolls, July, est 185k (pr 195k)

- 8:30am: Personal Income, June, est. 0.4% (prior 0.5%)

- 9:45am: ISM New York, July (prior 47)

- 10am: Factory Orders, June, est. 2.3% (prior 2.1%)

- 12:15pm: Fed’s Bullard speaks on economy in Boston

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Obama nominates Hersman for another term as NTSB chairman; GFI Group’s Giancarlo as CFTC commissioner; O’Rielly named to FCC Republican seat

- Natl Governors Assn holds annual mtg in Milwaukee

WHAT TO WATCH:

- Dell holders to vote on Silver Lake, Michael Dell LBO

- Icahn in suit accuses Dell board of trying to force buyout

- Swaps probe finds banks manipulated rate, hurting retirees

- Apple seeks Obama reprieve on iPhone import ban from ITC

- Apple decision in case vs Samsung delayed until Aug. 9

- Dodd-Frank stands; suit by states, Texas bank thrown out

- Payrolls probably grew in July, helping trim jobless rate

- Hewlett-Packard ends LCD pricing suit vs Chunghwa, Tatung

- BofA faces claims from regulators on jumbo mortgages, CDOs

- Tourre’s “junior employee” defense seen leading to loss

- Halliburton, SLB sued on fracking price-fixing claims

- ICU Medical said to be in exclusive talks on sale to GTCR

- Canceling Lockheed F-35 said to be option in Pentagon review

- RBS appoints Ross McEwan as CEO as lender swings to profit

- Potash split has India’s biggest buyer seeking lower price

- Japan exchange in talks with Tocom on trading system

- U.S. Services, BOJ, Carney, HSBC, Rohani: Wk Ahead Aug. 3-10

EARNINGS (AM):

- Alliant Energy (LNT) 6am, $0.56

- Alpha Natural Resources (ANR) 7am, $(0.58)

- American Axle & Manufacturing (AXL) 8am, $0.30

- Bell Aliant (BA CN) 6am, C$0.41

- Berkshire Hathaway (BRK/A) 5pm, $2,166.00

- Brinker International (EAT) 7:45am, $0.74

- Buckeye Partners (BPL) 7am, $0.79

- Cablevision Systems (CVC) 8:30am, $0.05

- CBOE Holdings (CBOE) 7:30am, $0.51

- Chevron (CVX) 8:30am, $2.96 - Preview

- Church & Dwight (CHD) 7am, $0.59

- Eaton (ETN) 6:28am, $1.11

- Eldorado Gold (ELD CN) 7am, $0.08

- Exelis (XLS) 7am, $0.37

- Gartner (IT) 7am, $0.52

- Host Hotels & Resorts (HST) 6am, $0.42

- ImmunoGen (IMGN) 6:30am, $(0.30)

- Manitoba Telecom Services (MBT CN) 4:03pm, C$0.48

- Och-Ziff Capital (OZM) 7:30am, $0.13

- Pinnacle West Capital (PNW) 8am, $1.15

- PNM Resources (PNM) 8:30am, $0.33

- Power of Canada (POW CN) 12:05pm, C$0.60

- Sealed Air (SEE) 6am, $0.25

- Sirona Dental Systems (SIRO) 6:30am, $0.91

- SNC-Lavalin Group (SNC CN) 8:27am, C$0.53

- Telephone & Data Systems (TDS) 7:32am, $0.09

- Ultra Petroleum (UPL) 8am, $0.43

- United States Cellular (USM) 7:32am, $0.17

- Viacom (VIAB) 6:55am, $1.30 - Preview

- Washington Post (WPO) 8:30am, No est.

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Baguette Hopes Fade for Some French Farmers on Low-Protein Wheat

- p Commodities Market, Industry News »

- Gold Bears Dominant Again as U.S. Growth Quickens: Commodities

- WTI Heads for Weekly Advance Before Jobs Data; Brent Tops $110

- Gold Extends Biggest Weekly Drop Since June on Better U.S. Data

- Copper Rises on Buying of Metal to Close Out Bets on a Decline

- Wheat Advances Amid Crop-Quality Concerns From France to U.S.

- Potash Split Prompts India’s Biggest Buyer to Seek Price Cut

- Coffee Climbs After Brazil Plans Aid for Farmers; Cocoa Falls

- Record High-Quality Wheat Prices in China May Spur Imports

- Iron Ore Rally May Firm on Chinese Demand; More Supply Ahead

- Olam Defies Russian Grain-Export Slump as Traders Retreat

- Crude Premium Rises to 2013 High in Asia on Iraq: Energy Markets

- Obama Nominates GFI Group’s Giancarlo as CFTC Commissioner

- COMMODITIES DAYBOOK: Gold Bears Regain Dominance on U.S. Growth

- Wheat Costs in Japan Climbing for Third Time as Abenomics Bites

CURRENCIES

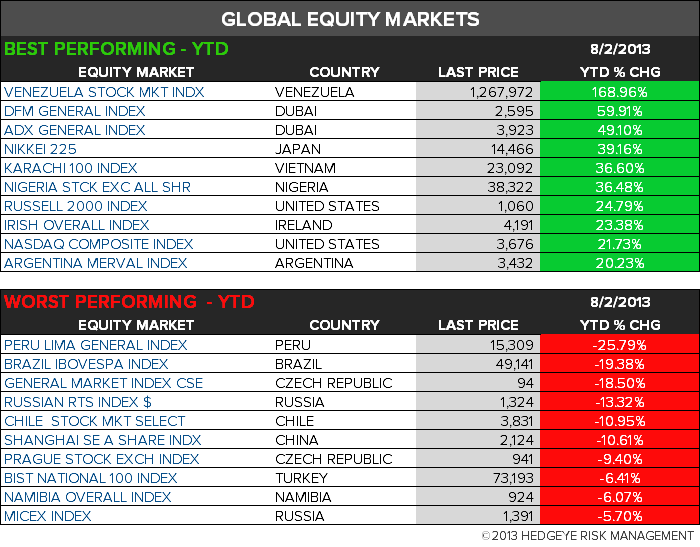

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

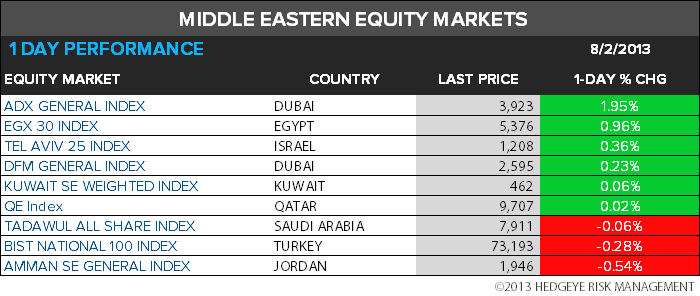

MIDDLE EAST

The Hedgeye Macro Team