TODAY’S S&P 500 SET-UP – July 31, 2013

As we look at today's setup for the S&P 500, the range is 16 points or 0.18% downside to 1683 and 0.77% upside to 1699.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.29 from 2.30

- VIX closed at 13.39 1 day percent change of 0.00%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, July 26 (prior -1.20%)

- 8:15am: ADP Employment Change, July, est. 180k (prior 188k)

- 8:30am: Employment Cost Index, 2Q, est. 0.4% (prior 0.5%)

- 8:30am: GDP Q/q, 2Q, est. 1% (prior 1.8%)

- 8:30am: Personal consumption, 2Q, est. 1.6% (prior 2.6%)

- 8:30am: U.S. Treasury quarterly refunding announcement

- 9am: ISM Milwaukee, July, est. 52 (prior 51.55)

- 9:45am: Chicago Purchasing Mgr, July, est. 54 (prior 51.6)

- 10:30am: DOE Energy Inventories

- 2pm: FOMC rate decision

- 3pm: Fed Aug. schedule for tentative outright Treasury buys

GOVERNMENT:

- President Obama meets w/ House, Senate Democrats

- Biggest U.S. equity exchange operators, trade group plan to ask SEC to delay final phase of market-wide program aimed at curbing sudden stock swings that takes effect Aug. 1

- 9:30am: Senate Environment and Public Works Cmte hearing on toxic chemical threats

- 10am: Senate Judiciary Cmte hearing on Foreign Intelligence Surveillance Act programs

- 12:30pm: House Budget Cmte hearing on poverty

- 2pm: Joint Economic Cmte hearing on tax laws, eco growth

- 2:30pm: Senate Finance Cmte hearing on principles for energy tax changes

- 2:30pm: Senate Commerce, Science and Transportation Cmte hearing on energy drinks, concerns about marketing to youth

- Senate confirms 5 to U.S. Labor Board, averting shutdown

WHAT TO WATCH

- Ebbing finl-mkt risk gives Fed option to delay tapering

- Alexion said to enlist Goldman to advise amid Roche overture

- Bill Ackman to unveil $2b investment, WSJ says

- Cubist buys Trius, Optimer to expand stable of antibiotics

- Intuit settles antitrust suit on pact to not hire from rivals

- U.S. economy probably grew at slower pace in 2Q

- HP says ex-SEC general counsel advising on Autonomy deal probe

- Amgen boosts yr EPS view; Phase 2 AMG-747 study terminated

- KKR said to consider bidding for Hutchison’s ParknShop

- Las Vegas Sands loses bid to vacate $101.6m trial verdict

- Honda maintains forecast after profit misses ests.

- Schneider Electric to buy Invensys for GBP3.4b cash, shrs

- Blackstone said to buy 7 Australian offices from GE Capital

- UBS to pay $60m fine to settle SEC mortgage-bond probe: WSJ

- BlackRock starts retirement indexes in push for retail assets

- German retail sales drop in sign of slow recovery

- Euro-area July consumer prices up 1.6% Y/y; est. 1.6%

- Toyota said to prepare to raise output target above 10m

- China leadership pledges steady growth w/ eco reforms

- EADS to adopt Airbus name, reflecting dominance of unit

EARNINGS:

- Humana (HUM) 6am, $2.47 - Preview

- ADT (ADT) 6am, $0.43

- Huntsman (HUN) 6am, $0.39

- Athabasca Oil (ATH CN) 6am, C($0.04)

- CGI Group (GIB/A CN) 6:30am, C$0.58

- NiSource (NI) 6:30am, $0.23

- Regency Centers (REG) 6:30am, $0.64

- Energen (EGN) 6:30am, $0.61

- SPX (SPW) 6:30am, $0.65

- Ingredion (INGR) 6:35am, $1.17

- Intact Financial (IFC CN) 6:55am, C$0.75

- Comcast (CMCSA) 7am, $0.63 - Preview

- American Tower (AMT) 7am, $0.90

- Delphi Automotive (DLPH) 7am, $1.14

- Wisconsin Energy (WEC) 7am, $0.47

- RioCan REIT (REI-U CN) 7am, C$0.40

- Garmin (GRMN) 7am, $0.65

- Burger King Worldwide (BKW) 7am, $0.19

- Booz Allen Hamilton (BAH) 7am, $0.40

- Jones Group (JNY) 7am, ($0.12)

- AllianceBernstein (AB) 7:02am, $0.38

- Southern (SO) 7:30am, $0.68

- Exelon (EXC) 7:30am, $0.54

- Hess (HES) 7:30am, $1.40

- Invesco (IVZ) 7:30am, $0.51

- Hyatt Hotels (H) 7:30am, $0.30

- Energizer (ENR) 7:30am, $1.31

- Hospira (HSP) 7:30am, $0.51

- Level 3 Communications (LVLT) 7:30am, ($0.09)

- Heartland Payment Systems (HPY) 7:30am, $0.58

- SodaStream International (SODA) 7:30am, $0.66

- Sherritt International (S CN) 7:42am, C$0.12

- Mastercard (MA) 8am, $6.29

- Phillips 66 (PSX) 8am, $1.81

- AGL Resources (GAS) 8am, $0.27

- Hudson City Bancorp (HCBK) 8am, $0.10

- Hercules Offshore (HERO) 8am, $0.05

- PG&E (PCG) 8:03am, $0.73

- AGCO (AGCO) 8:15am, $1.81 - Preview

- Allergan (AGN) 9am, $1.20

- Great-West Lifeco (GWO CN) 10:24am, C$0.54 - Preview

- New Gold (NGD CN) Bef-mkt, $0.05 - Preview

- Williams (WMB) 4pm, $0.14

- Bruker (BRKR) 4pm, $0.14

- WebMD Health (WBMD) 4pm, $0.06

- CBS (CBS) 4:01pm, $0.72 - Preview

- Williams Partners (WPZ) 4:01pm, $0.37

- Pioneer Natural Resources (PXD) 4:01pm, $1.11

- Amdocs (DOX) 4:01pm, $0.73

- Open Text (OTC CN) 4:01pm, $1.41

- CBL & Associates Properties (CBL) 4:01pm, $0.53

- Trinity Industries (TRN) 4:01pm, $0.95

- Bloomin’ Brands (BLMN) 4:01pm, $0.23

- DreamWorks Animation SKG (DWA) 4:01pm, $0.20

- Whole Foods Market (WFM) 4:02pm, $0.37 - Preview

- ServiceNow (NOW) 4:02pm, ($0.05)

- Shutterfly (SFLY) 4:02pm, ($0.16)

- Thoratec (THOR) 4:02pm, $0.43

- MetLife (MET) 4:03pm, $1.33

- Yelp (YELP) 4:03pm, ($0.04)

- Allstate (ALL) 4:05pm, $0.98

- Lam Research (LRCX) 4:05pm, $0.71

- Pharmacyclics (PCYC) 4:05pm, ($0.04)

- QEP Resources (QEP) 4:05pm, $0.35

- Seattle Genetics (SGEN) 4:05pm, ($0.21)

- Questar (STR) 4:05pm, $0.22

- Atmel (ATML) 4:05pm, $0.06

- SunPower (SPWR) 4:05pm, $0.11 - Preview

- Rovi (ROVI) 4:05pm, $0.46

- PHH (PHH) 4:05pm, $0.37

- Ruckus Wireless (RKUS) 4:05pm, $0.03

- Ashford Hospitality Trust (AHT) 4:05pm, $0.60

- Atwood Oceanics (ATW) 4:09pm, $1.34

- Lincoln National (LNC) 4:10pm, $1.15

- Western Gas Equity Partners (WGP) 4:10pm, $0.13

- Western Gas Partners (WES) 4:13pm, $0.38

- Microchip Technology (MCHP) 4:15pm, $0.54

- Concur Technologies (CNQR) 4:15pm, $0.37

- Trulia (TRLA) 4:17pm, $0.03

- Yamana Gold (YRI CN) 4:23pm, $0.11 - Preview

- Essex Property Trust (ESS) 4:27pm, $1.85

- Marriott International (MAR) 4:30pm, $0.57

- Charles River Laboratories (CRL) 4:30pm, $0.71

- Eagle Rock Energy Partners (EROC) 4:30pm, $0.05

- Murphy Oil (MUR) 4:31pm, $1.54

- First Quantum Minerals (FM CN) 5pm, $0.21

- Kinross Gold (K CN) 5pm, $0.06 - Preview

- DDR (DDR) 5pm, $0.27

- Ctrip.com International (CTRP) 5pm, $0.30

- Axiall (AXLL) 5pm, $1.18

- Vanguard Natural Resources (VNR) 5:15pm, $0.33

- NXP Semiconductor (NXPI) 8pm, $0.66

- Suncor Energy (SU CN) 10pm, C$0.63 - Preview

- US Silica (SLCA) Aft-mkt, $0.40

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

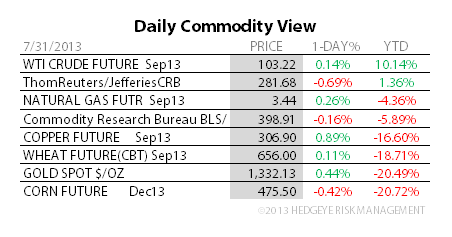

- ANZ Opens 50 Ton Gold Vault in Singapore as Asian Demand Climbs

- Potash’s $20 Billion Market Transformed by Uralkali: Commodities

- Wheat Climbs on Signs Lower Prices Fueled Demand From Importers

- Commodity-Linked Structured Note Sales Slump to Nine-Year Low

- Gold Extends Biggest Monthly Gain Since January 2012 Before Fed

- WTI Set for Best Month Since August Before U.S. Oil Supply Data

- Rebar Advances for Second Month as China Pledges Steady Growth

- Palm Oil Climbs to One-Week High as Weak Ringgit Boosts Exports

- Potash Group Surviving Demise of Russian Rival: Corporate Canada

- Glencore Takes Lead in Metals Storage as Goldman, JPMorgan Cut

- Oil Contango Hazard for Bulls Seen in WTI Prices: Energy Markets

- Shell to Chevron Move Offshore as Nigerian Risks Mount: Energy

- LME Zinc Stocks at 10-Month Low Amid Supply Deficit: BI Chart

- Corn Seen Sliding Below $4.50 on Bear Flag: Technical Analysis

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team