Pulls the market back to trend (that's a good thing)

Macau is back on track for another 20% (give or take) growth month. We remain bullish on Macau. The near-term momentum is strong and we believe there is cushion in both the VIP and Mass business to offset the China macro issues.

Average daily table revenues (ADTR) grew 50% YoY this past week and up 13% over June’s ADTR. With only 3 days left in the month, it’s pretty safe to say that July was a good month for the Macau operators. We are raising our full month GGR growth projection (includes slots) to +19-21% YoY, up from 14-19%.

The strength this past week looks volume driven both in the VIP and the Mass segments. While not included in the table games numbers, we are hearing the Electronic Table Games seem to be surging and could provide a boost above our slot forecast of HK$1.15 billion in July revenues.

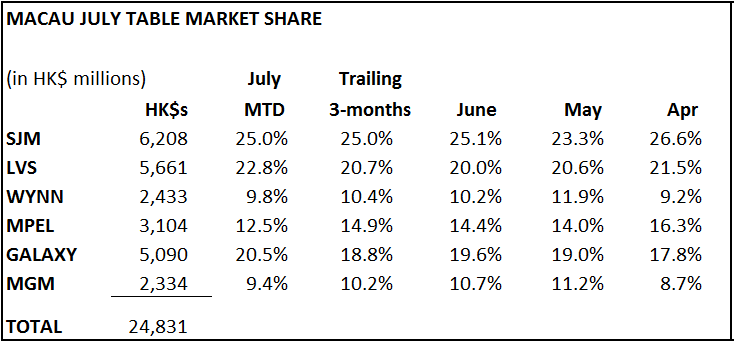

In terms of market share, July has been a big month for LVS and Galaxy. LVS's share of 22.8% is not only above the 3 month trend but grew 170 bps month-to-date in only one week. The big boxing match held at the Venetian on Saturday night probably drove most of the increase. We heard the Mass floor at the Venetian was packed and it's safe to assume that a number of top VIPs were present as well. The match featured the very popular boxer Zou Shiming who was the first Chinese fighter to ever medal at the Olympics. We can only imagine how successful the Manny Paquio fight will be in November.

MPEL remains well below its recent share trend and Wynn and MGM are trending slightly lower. LVS likely took share from all 3 operators, especially MPEL on Saturday. MPEL is likely holding below the market but we also think that Altira had a couple of bad volume weeks. However, MPEL remains one of our top picks along with MGM and LVS.