This note was originally published July 23, 2013 at 15:54 in Macro

“What the *&%! Just Happened” headlined yesterday’s release of GMO’s quarterly investment letter. While the title is probably accurate in capturing the prevailing, post-Taper announcement sentiment of the larger investment community, that the initial inflection in a bond bubble 30Y’s in the making occurred with some price convexity, and not a wimper, shouldn’t be particularly surprising.

In fact, if you have been long U.S. growth for the last 8 months, the Taper announcement itself was more a confirmation of economic reality than a prodigious central planning event. The acceleration in the domestic macro data since late November and the slow creep higher in the 10-2 spread were heralding some measure of a policy shift.

In so much as a widening in the yield spread <--> expectations for QE Taper <--> Improving Domestic Macro, is a transitive relationship, the recent “bear steepening” in rates should be taken as positive confirmation of an improving domestic growth outlook. This first step function move higher in yields is simply the market adjusting to the positive gravity of the domestic economic data and the implications of a sober policy response.

In essence, the initial move in rates represents the ball under water moving towards being only half-submerged.

From here, particularly given the Fed’s much communicated ‘data dependency’, the next 100+ bps higher should be viewed more as a growth dependent return to interest rate normalcy than a tightening in the conventional sense. If the fundamental data is such that the controlling, dovish contingent at the fed is willing to signal a rate increase - even a small, gestural increase - we’d argue that pro-growth exposure should continue to outperform in the run-up to that event.

As we’ve moved past the acute response phase, the market has seemingly come to accept and price in a reduced flow of fed stimulus. We detailed the implications of #RatesRising on our 3Q13 Macro Themes call last week. We’d highlight a couple of incremental events of the last week:

ACCEPTING REALITY: Measures of implied interest rate volatility in the options markets have dropped precipitously over the last couple weeks. Seemingly, the market has absorbed the acute impacts of the initial announcement with investor angst ebbing alongside initial portfolio re-adjustments.

TAPER TIMELINE: Alongside lower volatility and a newly range-bound 10Y, today’s main policy related headline from Bloomberg that the consensus expectation of economists for Fed tapering (to the tune of $20B) to begin in September is further evidence that the market is getting comfortable in delineating the impacts of tapering vs. tightening.

Given the practical aspects of implementing a tapering which, practically, means they will reduce the flow of purchases and subsequently monitor the impact before implementing incremental reductions, a September start makes sense. With Bernanke likely stepping down come January, initiating the reversal of unprecedented policy initiatives which he captained makes sense from a continuity and (Bernanke) legacy perspective. It also gives policy makers sufficient runway for scaling back purchases with an early eye towards a complete cessation come mid 2014.

Also, implicit in the reduction in QE purchases is that QE was, in some manner, successful in its objective. This gives the FED and QE as a policy some credibility should they need to re-accelerate easing at some point in the future.

SEASONALITY REMINDER: As it relates to the expectation for tapering to begin in September - recall that the seasonal distortion present in the reported employment and economic data will build as a headwind thru August before again flipping to a tailwind over the Sept-March period. Any prospective delay in tapering due to perceived/optical weakening in the data over the next 6 weeks should be short-lived as the impact of the distortion reverses come September. Further, any negative drag associated with reduced stimulus may be partially masked by the positive seasonal tailwind as we move towards year-end and through 1Q14.

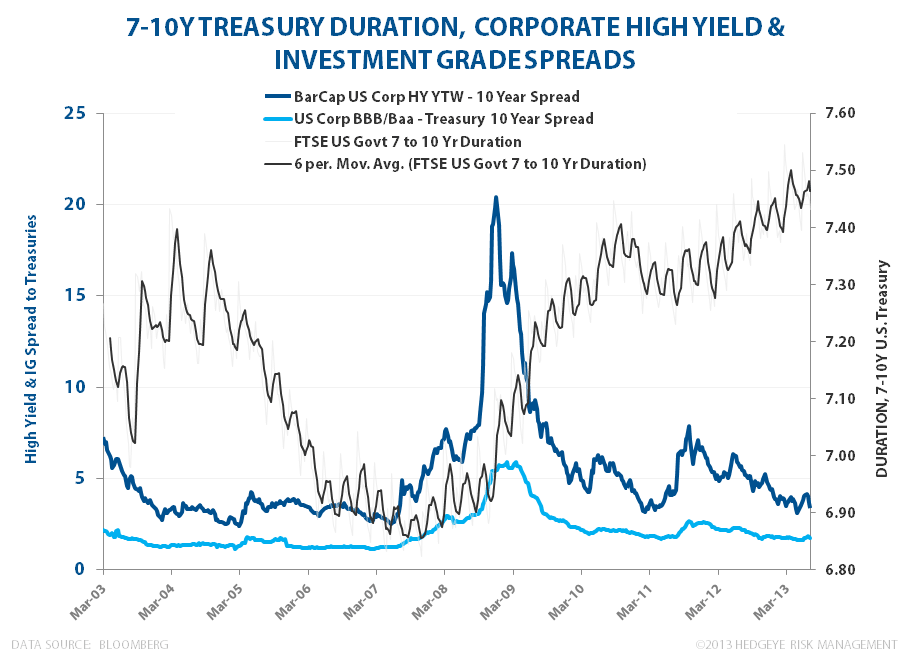

(Not So) LATENT RISK: Duration (price sensitivity to interest rate movement) on 10Y treasuries remains near peak levels while high yield and IG spreads remain near trough levels. Despite the recent diminuendo in interest rate volatility, risk associated with another expedited back-up in yields remains very much alive across the fixed income spectrum.

Quantitative Setup: 10Y Treasury Yields remain in Bullish Formation (Bullish across TRADE, TREND, & TAIL Durations) with immediate support and resistance at 2.45% and 2.75%, respectively.

Christian B. Drake

Senior Analyst