There's been no better time to be an off-price retailer than the past 12-18 months. We've seen retail bankruptcies accelerate, consumer demand shrink rapidly, and the entire apparel industry has scrambled to right-size inventories. This has created the perfect storm of high quality goods in abundant quantities at great prices (i.e. supply) coupled with a value focused consumer (i.e. demand) seeking to save on apparel expenditures. ROST is the poster child for the kind of company that benefits from this phenomena.

Over the years, the Street has been overly focused on the day when "just-in-time" manufacturing and ERP systems would finally wreak havoc on the off-price model. If you listen to any conference call with either TJX or ROST, there is always the obligatory question asking about the "availability of goods". The answer is also always, "there are plenty of goods for purchase". This holds now even truer than ever. As long as consumer demand remains subject to change without notice and factories seek to run at high capacity levels, there will be a viable market for the off-price business. However, there will not always be a perfect storm like the one we are currently exiting.

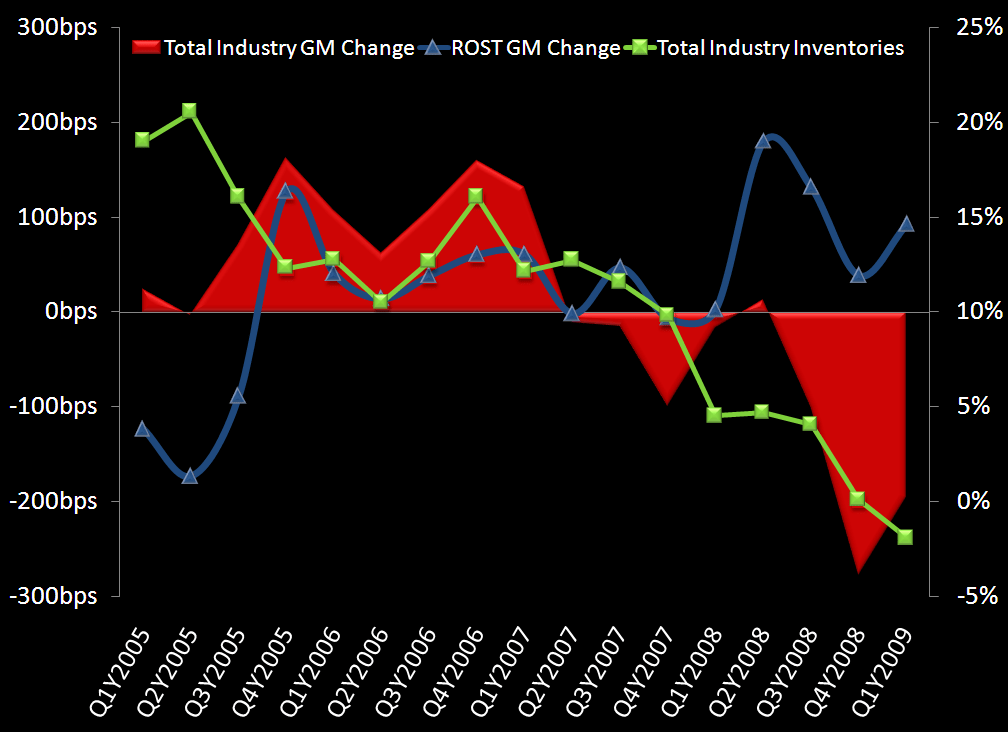

There is no question that ROST has managed its business well against a very challenging backdrop. Inventories have declined for the past six quarters and guidance suggests that they'll remain lean over the remainder of this year. SG&A expenses have been in check, only rising 28 bps since 2005 despite inflationary pressures including healthcare, payroll, and energy costs. Additionally, gross margins have expanded dramatically over the same period, up nearly 100bps while most other retailers have seen margins erode from peak levels. In fact, ROST is now on pace to report its highest operating margin (8%) in six years!

It's tough to knock this name right now given that they are seemingly doing everything right. In fact, ROST was the first company to meaningfully increase guidance with confidence in both the current quarter and remainder of 2009. (Betting that 'this is finally the end' has led to plenty a face-ripping for shorts over the past 2 quarters).

But this brings us to where we're focused for the remainder of the year as it pertains to ROST:

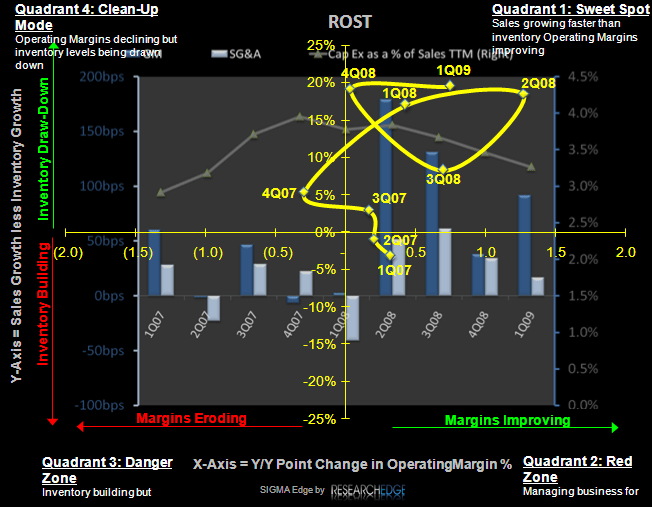

- High expectations coupled with comparisons on the gross margin and SG&A line that become increasingly difficult. GM's were up 128 bps in 2Q08 and 70 bps in 3Q08. Check out our SIGMA chart below.

- Top line compares remain tough in the current quarter as ROST cycles last year's stimulus checks. Same store sales were up 6% in 2Q08. Keep in mind that annual same store sales for ROST have only ranged from -1 to +6% at any time over the past 6 years.

- CA, its largest market, just reported a 4% comp increase for 1Q vs. 3% for the chain. We have been hearing more frequent discussions of a "relapse" in CA on the foreclosure front which may create a headwind in the coming months.

- Management has been talking positively about the recent success of the lower-priced, lower-income targeted DD's Discount concept. With all due respect, shouldn't this concept be doing great in the worst consumer downturn since the Great Depression?

- I have no doubt that there will be an abundant supply of goods for ROST, forever. However, I just don't see how the "quality" of the goods at very favorable purchase prices can be as beneficial in the next 3 quarters as it was in the prior three quarters. Inventory metrics for both the manufacturers and retailers show that supply has diminished materially over the past year. This should have an impact on gross margins going forward.

- Year over year comparisons on gasoline and transportation costs are no longer as beneficial. Additionally, prices at the pump have actually moved higher ($2.99/gallon over the Memorial Day weekend in NY) and may begin to impact both the cost and demand side of the equation.

At this point, the winds are changing and the extreme tailwinds that have favored ROST are easing. With the stock within 10% of its all-time high, heightened earnings expectations, peak margins, and the unlikely scenario in which the inventory glut of 2008 is repeated anytime soon, the fundamental risk here far outweighs the reward at this stage.

Eric Levine

Director