Summary

We received a number of responses from more positive investors challenging our CAT thesis following last Thursday’s presentation. The three key bullish themes that emerged were:

- Buyback: Better capital allocation for CAT going forward in the form of share repurchases

- Segment Models: The downside may look minor when modeled by segment, particularly when inventory reductions are factored in.

- Mining Cycle Already Well Known: The stock is hated already – how much downside could there be? Investors should ‘look through’ the downturn.

CAT has already underperformed and we have been negative on the name for over a year. However, we still see significant downside. While we could always be wrong and will change views as appropriate, data and experience suggest these cycles go on for much longer than most investors expect and frequently overshoot. This one seems to be just getting started.

Argument 1: Better Capital Allocation/Buyback

Overvalued: CAT announced a $1 billion buyback with its disappointing 1Q 2013 earnings. That shift in capital allocation has generated some optimism – particularly on the day it was announced. However, CAT’s equity appears overvalued. Buying overvalued equity is not a great way to create value.

Good Acquisitions: If anything, issuing overvalued equity to make acquisitions of cheap, good businesses might add some value, even providing a short-term reporting boost from some of the purchase allocation flexibility. Following the challenges of ERA and Bucyrus, additional large acquisitions seem unlikely.

Buyback Valuation Discussion Cringe-Worthy: On the call following 1Q earnings CFO Bradley Halverson said with respect to the buyback:

“So the question is why now. And our balance sheet is very strong. We think with the drop in stock price recently and where our PE is, the fact that we believe we have a slow growing economy but one that's stable…. We had a good cash flow quarter. We have plans for a good cash flow year and we think, again, this is an opportunistic time here in the short term to reward our shareholders with $1 billion stock buyback.” - Bradley Halverson 4/22/13 (Bloomberg Transcript)

First, low multiple cyclicals tend to be overvalued - P/Es do not work as a valuation metric (cyclical investing 101). Cyclicals tend to be cheapest when earnings are negative and they have no P/E. Second, CAT already has plenty of leverage. Does anyone really think CAT is underleveraged? Finally, CAT has not been generating all that much free cash flow recently. If the cash flow impact of receivables growth and rental equipment purchases are included, CAT had negative free cash flow in 2012 (cash from operating activities less capital spending and investment in receivables).

Buy Backs & Performance: Buybacks tend to be a last resort for companies that do not have anything better to do with cash. They are also frequently used to manage investor sentiment by mingling the announced buybacks with poor financial results (like CAT’s 1Q 2013). Large buybacks are often associated with underperformance (see RRD or RSH, for example). When CAT was outperforming in the past decade, it was adding capacity and doing deals amid a robust market outlook. Now, aggressive internal investment appears less attractive.

Magnitude Insufficient: The announced buyback adds back cents to EPS, while the down-cycle in mining capital investment is likely to remove dollars.

Argument 2: Segment Models

Hard to Normalize: CAT changed its segment definitions, so gathering segment level history before 2009 is challenging. Add in acquisitions, and it is really difficult to look back at how changes in resources-related capital spending impacted the different businesses. Even management thinks so:

“In terms of what's normal, man, as I look back over the last few years in mining, it's a little tough to decide actually what's normal.” – Michael DeWalt, 4/22/13

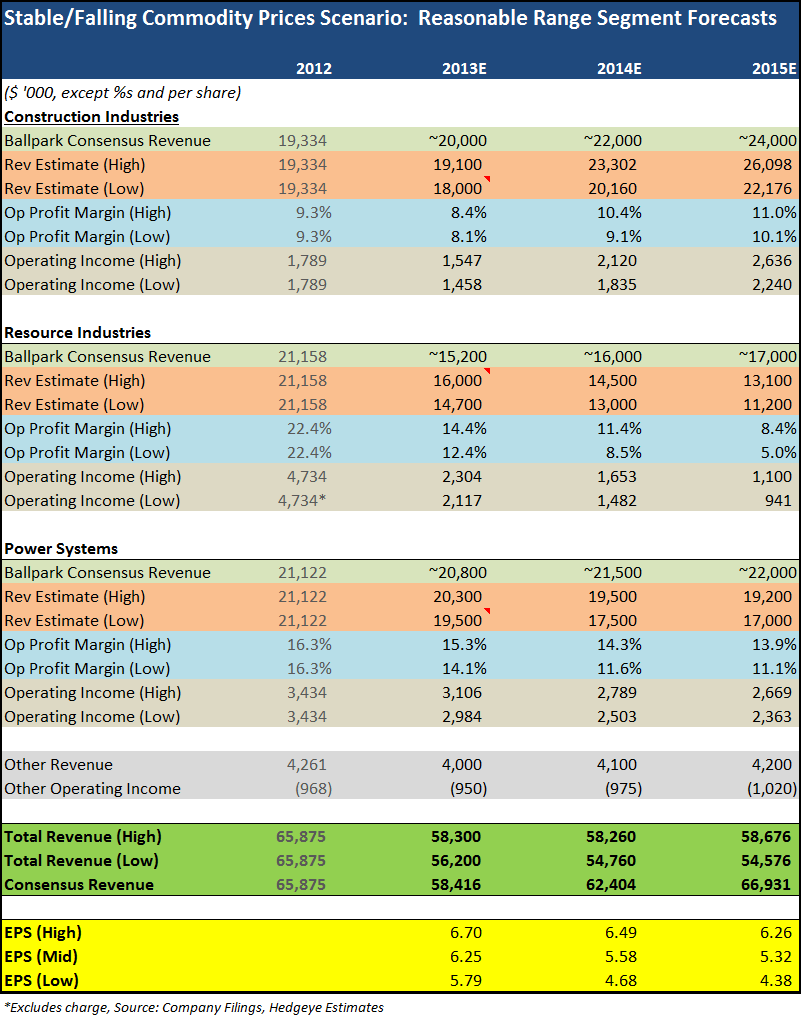

Our Forecast Range for a Flat/Declining Commodity Price Environment

Deep cyclicals like CAT tend not to have gentle changes in results over time. Many analysts nonetheless model gradual change, even when the evidence suggests otherwise. The table below assumes that the move higher in commodity prices is largely over – principally that metal and energy prices will not rise much faster than inflation in the forecast period. Our March 2013 Mining & Construction Equipment presentation supports that outlook, but it is a key assumption for the forecast. When commodity prices stall, resource-related capital spending reverts to maintenance-type levels in our analysis.

We don’t do point estimates, especially in cyclical names where long-term forecasts are likely to be significantly off. If an investor is on the right side of the cycle, industry structure and valuation, we have found that performance follows. That said, we were asked for specifics on our outlook for CAT segments. We provide the table below to give a sense of our views, with supporting discussion underneath. If the estimates for Resource Industries look extreme, just look up the volatility in results at Bucyrus, or in the shipbuilding industry or housing construction market. When the demand cycle moves, revenue and margin swing hard in the same direction.

Resource Industries

The decline in mining capital spending is not a deviation from normal levels, but a return to them. Resource Industries is dominated by mining capital spending, with coal, iron ore, copper, gold and other minerals as key end-markets.

Aftermarket Sales: Many investors seem to believe that Resource Industries sales are more than half parts and service. We think the actual number is a lower, perhaps only 25%-40% depending on the year. (If it were half of sales, CAT would open every presentation with it, and rightly so.) We see CAT’s dealer network as a liability in the mining equipment space, where there are only a couple hundred relevant customers globally. For example, JOY does derive slightly more than half of its sales from aftermarket products – but it does not have a dealer network to support. Dealers take a sizeable cut of the aftermarket revenue, as CAT dealers typically focus on service and support. As another indication, CAT reports total Bucyrus revenue (excluding divestitures) as $4.76 bil in 2012. Finning bought its distributorship for $465 million and reports that in the ~half year that it owned it, the distributorship generated $233 million in revenue. If we assume the same service-to-new-products revenue mix for the Bucyrus distributorship as Finning and assume a similar sales multiple for the other divestitures, we get an aftermarket share of around 30%-35%. It is also worth noting that if mining activity weakens significantly, existing equipment may be parted out, reducing aftermarket sales. CAT should simply disclose the number in an unambiguous, wink-free way.

Scale & Duration of Decline: We expect to see a 70% decline, give or take about 10 percentage points, in mining capital spending in total over something like four to seven years. That is derived from an expectation that mining capital spending will return to maintenance levels (see slides 7 & 8 in our recent CAT slide deck for how we get there). Near maintenance levels of capex is what miners normally spend. That is because mining is a sub-GDP growth industry that tends to add its capacity in huge lumps (like in the ‘00s and the ‘70s). That capex decline includes a portion of parts and service, since those are often capitalized expenses. Importantly, CAT’s backlog already contains orders stretching out quarters and years, so investors can look ahead further than the reported topline.

Margin Pressure: Mining equipment companies added significant manufacturing capacity over the past decade. If our view of the pending market decline is correct, it would be internally inconsistent not to model significant margin pressure. CAT, Komatsu, Hitachi, Liebherr and others are likely to be more price competitive when backlog duration is short and capacity is available. JOY’s operating margins ranged from slightly negative to a high single digit from 1. In the resources-related capital spending boom, JOY’s operating margin nearly tripled. Given the topline outlook for mining capital spending, the margin assumptions presented could prove generous. In the early 1980s, following the last resource-related capital investment boom, competition from Komatsu helped drive very significant losses at CAT.

So Much Hasn’t Hit Yet: Of course, dealer inventory adjustments are a major factor in the 1Q sales decline and CAT’s own inventory adjustments also negatively impacted margins. However, Resource Industries has only reported one quarter of YoY revenue declines. It seems a bit premature to call the end of a likely multi-year reversal in this segment after just one quarter. Resource Industries pricing was still up in 1Q. Pricing can hold for a little while as the industry works on backlog – like in 2009 – but a sustained downturn amid industry overcapacity is likely to produce intense price competition.

Power Systems

Resources Exposed: We have generally referenced “resource-related” capital investment as opposed to “mining” capital investment. That is so we could also reference energy-related capital investment at Power Systems. While CAT has not done a great job at breaking down end market exposures for Power Systems, it is no stretch to suggest that the division is heavily exposed to oil & gas capital investment. The division also has some exposure to mining capital spending, such as mine site power and locomotives.

Not As Big Of A Drop, But It Could Be: Oil & gas capital spending also boomed in the past decade. That helped growth in some of CAT’s highest margin Power Systems product lines. We assume that Power Systems is half ‘resources’ exposed, with much of that exposure from oil & gas. Even though oil prices, for instance, have held reasonably firm, they have still appeared to stall since 2010/2011, or even 2007. Historically, stable commodity prices drive capital spending back toward maintenance levels. Critically, large energy companies appear to have started cutting capital spending. We have assumed drops in line with 1Q 2013 actuals, but oil & gas capital spending may well be the next shoe to drop for CAT if energy prices remain stagnant.

Locomotives & Other: Locomotive demand is exposed to commodity volumes. Sales should see slowing demand growth following a long period of significant investment by railroads (including mining railroads). New locomotive emissions regulations ~2015 are a factor. We assume the balance grows at a mid-single digit rate.

Construction Industries

Rebound Likely, Industry Competitive: We expect a delayed but significant cyclical upswing in construction equipment. We prefer developed market exposure in less competitive niche products to CAT’s broad product portfolio. As a whole, the industry tends to be fragmented and competitive. Even in a demand upswing, we do not expect Construction Industries to deliver margins comparable to those of Resource Industries near its peak.

A Better Idea: If an investor wants exposure to the rebound in construction equipment demand, they should buy a construction equipment company. CAT’s profit outlook is not dominated by the outlook for construction equipment demand, in our view. Even estimates that are above street expectations fail to deliver upside for CAT EPS.

Argument 3: Mining Cycle Already Well Known

Not In Consensus: From what we can see of consensus expectations, the “well known” impact seems limited to 2013, with remarkable improvement thereafter in 2014 and 2015. If forecasters are looking for a one year speed bump, then the cycle is not known, or at least not well understood.

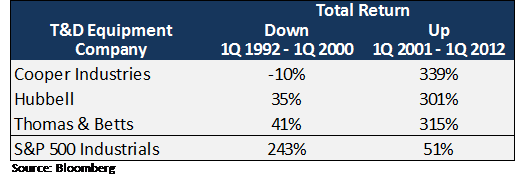

Not Unusual for Recognition: In our launch deck last year, we included a table showing the up-cycle in Transmission & Distribution (T&D) equipment. T&D stocks outperformed handily even after the huge northeast blackout in 2003, a demand sign that was hard for anyone investing in NYC, Boston or CT to miss. That cycle was well recognized, but it still worked. CAT has so far, too. Mostly analysts hesitate to show how long and positive an up-cycle can be. The opposite tends to hold true on the downside.

Investors Are Not Going To Look Through It: We do not know many analysts or PMs with the patience to ride out a four to seven year down-cycle. We expect resources-related capital spending to go down and stay down for decades. There is no other side to see.

2Q Outlook

1Q Weakness vs. 2Q Expectations: Given how spectacularly weak 1Q 2013 headline results were, 2Q may well improve sequentially. Inventory destocking is supposed to slow from 1Q 2013’s pace and production is guided to improve along with it. However, just as in 1Q, we do not expect the market to respond much to headline results. We also think there is a small chance that management drops the increasing unattainable $12-$18 2015 EPS guidance.

Implied Orders Matter More: Implied orders are likely to matter more than the headline number (implied orders = period revenues – change in backlog). These stabilized in 1Q amid a short-lived rebound in key commodity prices. Weakness in iron ore, copper and coal is likely to generate a renewed decline in implied order rates this quarter. For all of the focus on dealer retail sales, they lag. Orders tend to lead. This is where we expect CAT to struggle in 2Q and in 2H 2013. Declines in implied orders are important for our short thesis. If we are correct, those declines should start to push 2014 expectations lower, along with normalized profit expectations.