Re-accelerating Chinese Demand combined with the REFLATION trade have basically been the dominating global macro factors behind the bullish stance that we have held for the past 3 months. Everything was prefaced on our "Breaking The Buck" macro call, and for a generational short squeeze in most global equity markets our thesis worked.

Now the Buck isn't breaking - its crashing... so I am back to hunting from the bear camp. If we have an American currency crisis, very few things will work. I am long Gold (GLD) and TIPs (TIP), Healthcare (XLV), and Energy (XLE), China (CAF), etc... and there is no level of certainty that those will work either. Crisis are called crisis for good reason, and I do not use the term loosely.

After trying to resuscitate herself in the early morning, intraday you are seeing the USD break down to lower lows. This is bad. Treasuries are now selling off alongside the US Dollar (which is counterintuitive to people who think Treasuries are "quality"). If US Cash gets trashed, Treasuries are not the "safety trade" that they used to be. The Japanese are already selling Treasuries, and China's order is potentially pending...

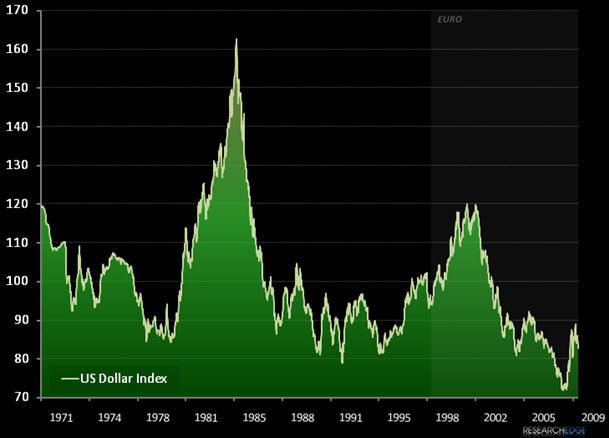

My critical line of long term support (81.42) on the US Dollar Index is broken. If this downward spiral of US currency credibility holds, you're going to see a real life stress-test of Mr. Secretary of the US Treasury. This could be one that even the almighty ole boy network won't be able to figure out.

Perceived wisdom is a very dangerous element to this cocktail, particularly when you mix it up with some glaring levels of Washington/Wall Street groupthink. In the charts below, Andrew Barber and I have outlined the same chart flashing a light on 3 different realities: USD solo, USD since Euro, and USD's long standing 3-year moving average. I started this chart in 1971, because that's when Nixon abandoned the Gold Standard.

Think long and hard about these charts, and pass them around to your friends. Who knows, maybe President Obama will get a copy and figure out the point. He claims to "get" it on most things, and I have no reason to believe anyone who is allowed to be objective can't "get" this point. Post 1971 the US Financial System has been based upon the elimination of a post War gold standard and the accepted narrative fallacy of limitless credit creation based on that US Dollar as the world's reserve currency.

This is scary,

KM

Keith R. McCullough

CEO, Research Edge LLC

New Haven, CT