“The greatest obstacle to pleasure is not pain; it is delusion.”

-Lucretius

When I read that in The Swerve (pg 196) I couldn’t stop drawing the analogy between the 14-16th century Vatican and the US Federal Reserve. That might sound a little out there for you this morning, but Bernanke’s fear-mongering dogma is way out there too. Hopefully you can find some balance in between our opposing definitions of economic freedom. I am, if you care, Catholic.

If you stop studying the history of your beliefs, you’ll have issues. At the end of the 4th century, “historian Ammianus Marcellinus complained that Romans had virtually abandoned serious reading.” (pg 93) Getting people to just take the church’s word for it without thinking was a process (no books). “It had taken a thousand years to win the struggle and secure the triumph of pain seeking.” (pg 107)

Mixing politics, religion, and perceived wisdoms – that’s bringing it on thick. But it’s the only way I can remind you that the pattern of changing human beliefs are not new this morning. It’s called education. The delusion that a country needs to be perpetually punished by a weak currency and a 0% return on her hard earned savings is one of the greatest obstacles to free-market pleasures.

Back to the Global Macro Grind…

Many are paid to think Bernanke is right. They believe that the US Dollar needs to be beat and whipped whenever it rises from the deadness of it all. Many think bond yields should stay at the 0% bound in perpetuity too. Just don’t forget why – they run Bond funds.

This morning we’re seeing a sharp contrast between American and Chinese economic policies:

- In the USA, people who are long Gold, Bonds, and Crude Oil futures continue to beg for Bernanke to talk down tapering

- In China, they’re reminding you that the entire world doesn’t sign off on short-term (reactive) Keynesian policy making

In a strikingly simple statement overnight, China’s Finance Minister said that they “won’t use large scale stimulus.” Markets took their word for it. The Shanghai Composite backed off in a hurry and closed down another 1%.

So who wouldn’t like a statement like that? Who will be in pain if, god forbid, Bernanke isn’t dovish in today’s testimony?

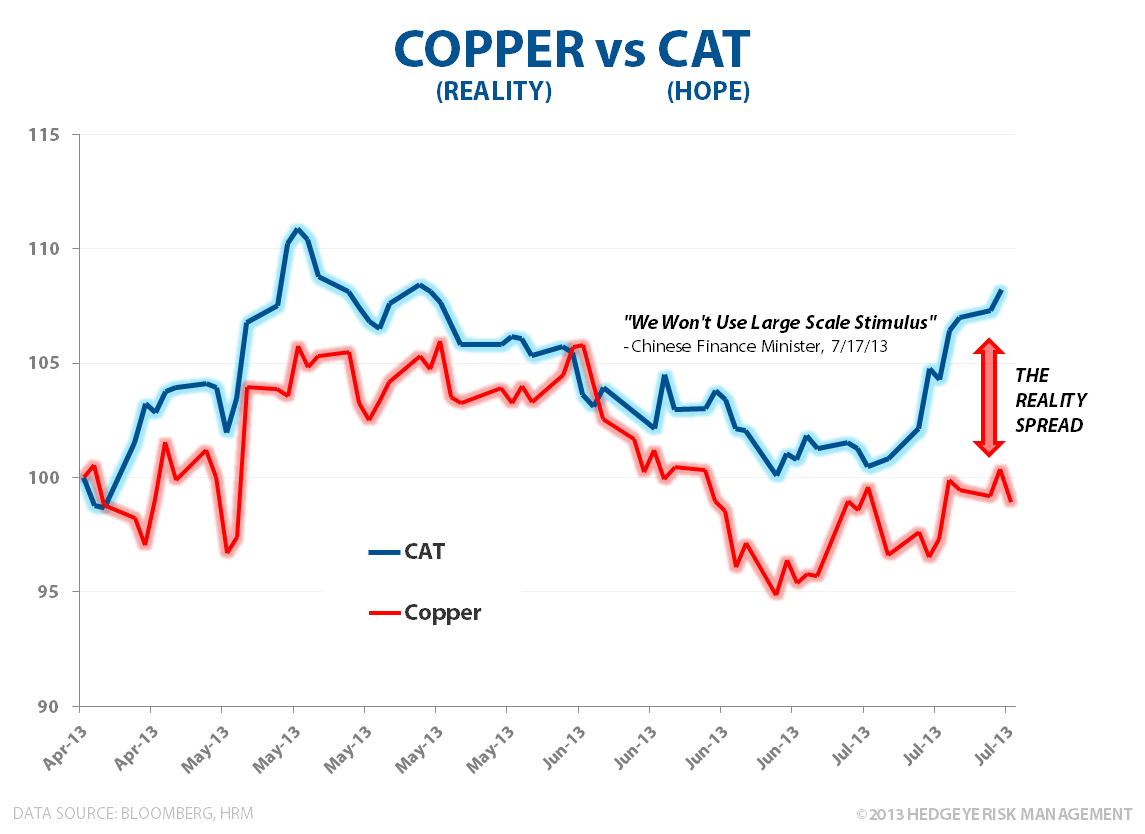

1. Copper – hopefully you aren’t long that bubble. It took the Chinese “news” (in line with Darius Dale’s view that China wasn’t going to stimulate you) seriously and Copper futures fell over -1% immediately. Don’t forget that when China was spending its brains out on “infrastructure” over 3 years ago, it represented almost 2/3 of incremental global copper demand.

2. Caterpillar – for the last year (as the Mining Capex Bubble began to pop) its CEO, Doug Oberhelman, has sounded like he should be running for political office in the south of France. He wants bailouts and government stimuli in his Chinese order book, baby! Do you blame him? I do. Hope is not an investment process.

Copper and CAT perma-bulls are just two of the many constituencies who lobby The Ben Bernank to whisper sweet-nothings of dovishness in the ears of the WSJ Hilsy (yes, the Jon Hilsenrath) as the Rest of Us just try our best to front-run it all.

If you don’t think that’s what’s really behind the pain-seeking messaging of the Fed, you are delusional. I have never seen the US government spend so much time talking down the one thing all these central plans were supposed to produce – growth.

And I mean real (inflation adjusted) economic growth. In the USA at least, sustained growth has always been married to 2 major (and coincident) leading pro-growth indicators:

1. #StrongDollar

2. #RisingRates

So, if you don’t want to step on anyone at the Fed Vatican’s toes – and if you never want to question any of these money-printing pontiffs publicly, you would have probably been cool with taking The Borgias word for it in the 15th and 16th centuries too.

In other news, the US stock market finally had a down day yesterday. That was its 1st down day in the last 9 as the SP500 and Russell2000 backed off their all-time highs of +18% and +23% YTD, respectively.

Immediate-term TRADE overbought is as overbought does, so we’ll see if we can re-load the long book on a correction to a reasonable line of immediate-term TRADE support (for SPY that’s now 1656).

The #1 thing that will stop me from getting really long again is Bernanke Burning The Buck (toning down tapering expectations). Every one of the aforementioned constituencies disagrees with me on that – but I’m betting 99% of The People in this country would call my #StrongDollar America the pleasure they seek.

Now, if only the US government explained it to them like we do, without all the conflicts of interest…

Our immediate-term Risk Ranges are now:

UST10yr 2.49-2.75%

SPX 1

Shanghai Comp 1

USD 82.12-83.61 (bullish)

Brent Oil 107.61-110.13

Copper 3.05-3.19

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer