Investing Ideas Updates:

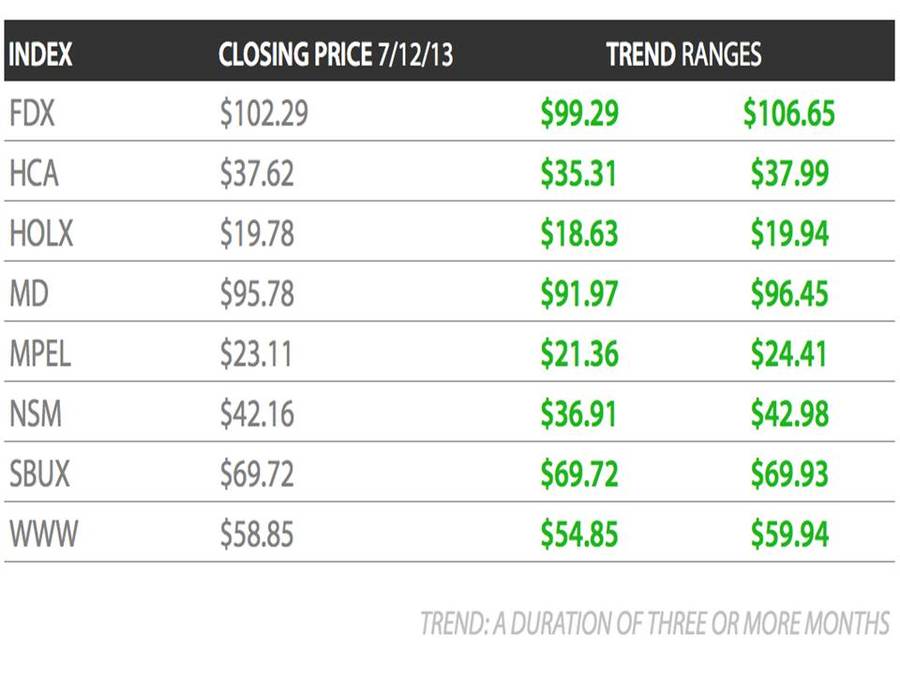

FDX: Industrials sector head Jay Van Sciver features FedEx in a Hedgeye Flash Call with investors. See this week’s Sector Spotlight (below) for a full write-up.

HCA: When Tenet (THC) announced that they were buying Vanguard Health Systems, they let slip that inpatient volumes continued to be soft in the second quarter after a weak first quarter. They also said their outpatient business was doing well, however, and despite the slowdown in inpatient volume, their results would trend toward the low end of their guidance.

The market overlap between HCA Corp and THC is high, roughly 70%, and trends at the two hospital operators mirroreach other closely. We suspect the recent THC news raised concerns that HCA will have a less than stellar result.

The other development this week has been news that the Obama Administration is delaying the employer mandate. While not a meaningful source of newly-insured consumers under Obamacare, it is a meaningful commentary on readiness. The implication is that other key parts of the law will be delayed as well, including the Exchanges.

Obamacare delays are negative for HCA and its peers and while none of the provision changes have caused changes in our outlook, we are keeping a close eye on developments in DC.

HOLX: We recently launched a survey of OB/GYNs we plan to take every month asking physicians about a number of key items that apply to Hologic as well as several other Subgroups including Hospitals and Managed Care. We’ll be asking about patient traffic, deliveries, pregnancy trends and key to the HOLX thesis, about changes in their use of the Pap smear.

Hologic’s Pap test, ThinPrep®, has been under pressure due to changes in the Cervical Cancer Screening Guidelines updated last year encouraging less frequent testing. We estimate ThinPrep® is 18% of HOLX’s current revenues, so while less frequent testing is a headwind, the exposure appears manageable to us.

Our survey will help us quantify how quickly the new guidelines are being adopted ahead of HOLX’s current quarterly result so stay tuned.

MD: Healthcare sector head Tom Tobin has no update on Mednax this week.

MPEL: Gaming, lodging and leisure sector head Todd Jordan has no update on Melco Crown this week.

NSM: The recent strength in Nationstar can be attributed to Fed Chairman Ben Bernanke’s comments this past Wednesday night that he isn’t in any hurry to begin tapering the Fed’s asset purchase program. This is good news for would-be mortgage refinancers, as tapering talk has pushed the long end of the yield curve (long-term interest rates) steadily higher since the beginning of May.

A substantial portion of Nationstar’s earnings come from mortgage origination, most of which is refinancing-driven.Traditionally, rising rates spell disaster for refinancing volume, so it’s not surprising to see Nationstar shares weak inthe short-term. The reasons we’re not overly concerned fundamentally are twofold.

First, most of Nationstar’s refinancing business isn’t traditional refinancing at all, it’s HARP refinancing. HARP refinancing entails borrowers who are underwater on their mortgages and cannot refinance through conventional means because their LTV, or loan-to-value, ratios are too high to meet traditional underwriting criteria.

The thing about HARP refi volume is that it is far less rate-sensitive than traditional refi volume. That’s because a) these borrowers have no other options and b) many of these borrowers are at rates well above market rates anyway, so even a sizeable back-up in rates has only a small effect on the savings they can achieve by refinancing through HARP. Also, it’s important to realize that HARP activity has been quite low in the servicing portfolios that Nationstar has acquired, namely the Bank of America book.

Second, there is a benefit to mortgage servicers from rising rates. Mortgage accounting can be a bit confusing, but here’s a simple way of thinking about it. Mortgage servicing rights, or the MSR, are recorded as an asset on the balance sheet. The MSR is the present value of the future stream of income from servicing the portfolio of mortgages under contract.

There are several things that can cause the value of this asset to fluctuate, one of which is interest rates. Rising ratesmake the asset more valuable because they reduce refinancing volume, which is the same as extending the life of the asset. Mortgage companies recognize changes in the value of the MSR asset as income or loss each quarter. As such, this rise in rates late in the quarter is likely to trigger a sizeable MSR write-up (i.e. more income) for Nationstar.

TRADE: In the short-term the market will trade NSM inversely to long-term interest rates.

TREND: Over the intermediate term, we expect 2Q earnings to be beat Street expectations when the company reports in mid-August , which should be a positive catalyst for the stock to move higher.

TAIL: In the long-term, there is still a tremendous opportunity for non-bank servicers like Nationstar to roll-up the servicing business. NSM is well positioned to be a prime beneficiary. We continue to think consensus earnings estimates remain too low for 2013/2014.

SBUX: Restaurants sector head Howard Penney has no update on Starbucks this week.

WWW: Retail sector head Brian McGough says “Wolverine World Wide’s 2Q print was spot-on with what we needed to remain confident in our call that this is a $100 stock over 2 years.” McGough was both amused and dismayed by Wall Street’s lack of vision, noting that many participants in the company’s earnings call this week were upset that WWW management refuses to be pulled into the game of making quarterly revenue and earnings estimates. Management did reaffirm their projected range of revenues for the full year, and upped their projected earnings guidance. But how is a Sell Side analyst (see this week’s Investing Term) to make a living when the companies he follows won’t cooperate?

Despite a significant drop in their Performance shoe division, McGough says the thesis on WWW remains strong: WWW will ramp up global revenues as it scales recently acquired brands over its existing global infrastructure. Taking successful shoe lines that are sold domestically, and opening them up to the world market should take this stock to a double for patient investors.

Macro Theme of the Week: C’mon In! The Water’s Fine

This shark – swallow you whole.

- Quint, “Jaws”

Bernanke to beach party revelers: it’s OK to go back into the water, kids!

There are metaphors aplenty to accompany this week’s celebratory scene as Helicopter Ben takes to the skies yet again. Hedgeye senior Financials sector analyst Jonathan Casteleyn says Fed Chairman Bernanke threw the markets for a loop in his Congressional testimony in May that “implied that the quantitative easing program that has been in place since 2008 could slowly be reigned in and that the Fed was becoming more data dependent.” The markets reacted to the emergence of a more fiscally prudent Fed the same as any spoiled child reacts when a parent says “No” – by throwing a tantrum.

If you have every witnessed an embarrassed parent watching their child writhing on the floor in the toy aisle, finally clutching the most expensive item just to quiet their screaming tot, then you have a pretty good idea of what must be going on down at the Federal Reserve these days.

The week started with dire predictions. “Treasury Yields Will Hit 4%” wrote Goldman Sachs. On Wednesday markets awoke to the release of last month’s Fed meeting minutes, revealing that the FOMC was about to slam on the brakes and bring the QE program to a screeching halt, ratcheting up interest rates several percentage points in a single move and crushing the global equity markets.

Well no, that’s not actually what the minutes revealed.

“Several FOMC participants backed the move to begin tapering soon” reports Forbes. So, for the record: “several” is not unanimity – nor even necessarily a majority – and “backing a move to begin tapering” means they will not object if, instead of buying $85 billion worth of bonds next month, Mr. Bernanke were to buy, say, $80 billion worth.

By Wednesday afternoon, the snot-smeared child that is our market was shrieking, kicking and battering its forehead against the floor and Daddy had to rush in muttering “Shush, shush… there, there, no one’s going to take away your nice toys.” The thought of going down in history as The Man Who Allowed The Stock Market To Correct While Driving 30-Year Mortgage Rates Over 4% was apparently enough to turn Bernanke from a Dovish Moderate, to a Moderate Dove(extra credit for readers who can parse the difference).

Bernanke played out his Road to Damascus moment at a National Bureau of Economic Research conference, reassuring anyone within earshot “you can only conclude that highly accommodative monetary policy for the foreseeable future is what’s needed.” The Fed is contemplating winding down its monthly purchases, but Bernanke promises to restore with the Left Hand what he taketh away with the Right.

For a moment it looked like markets were going to have to seek their own levels and trade purely on fundamentals. But not to worry. Americans have never known what it feels like to trade in markets free of government manipulation, and we aren’t going to find out any time soon.

We often hear government economists and policy makers express concern that market turmoil might “spill over and affect the real economy,” an Orwellian locution where the price of oil spiking over $110 is seen as a “market dislocation,” and not as a multi-billion dollar tax on America’s middle class.

There have been measurable benefits from government programs going back to the first responses to the crisis under Treasury Secretary Paulson, though largely of dubious value. The fact that we spent a trillion dollars to keep a bunch of bankers employed, while technically a win for the nation’s employment statistics, was arguably not the application that would have attained the utilitarian goal of the Greatest Good for the Greatest Number.

This week saw a convergence of data points that all point to the likelihood that Chairman Bernanke wants to retain Friends in High Places, assuming that his legacy will be set not by those who write history – and especially not by those who live it – but by those who decide what gets published. (Quoth the Duke of Gloucester, patron of historian Edward Gibbon, upon being presented with the completed Decline and Fall of the Roman Empire, “Another damned thick, square book! Always scribble, scribble, scribble, eh?”)

We don’t mean to scoff at the very real suffering caused by economic collapse, but Hedgeye holds firm to the view that government meddling in the economy is generally not a good thing, and that a long-term program of persistent government meddling in the economy is a decidedly harmful thing. Government intervention has the predictable effect of shortening economic cycles, while also increasing volatility – perhaps two sides of the same coin of time compression. In consequence, it also has the predictable effect of generally not really fixing anything and of battering the middle class, edging them nearer to the abyss with each new policy nudge.

By the Fed’s own reckoning, each successive round of QE has a diminishing impact on the markets. Mind you, that impact is measured in basis points – one-hundredths of a percent – and the twenty-five basis point impact looked for from any future round of QE is not predicted to last. The banks are still not lending, largely because of uncertainty over government policy. But don’t blame the banks. People aren’t borrowing, for much the same reason: no one wants to take a loan to expand a business that might be shot execution style by the Fed suddenly reversing its interest rate policy.

So, if the Fed’s easy money policy is not supporting the “real economy,” who is benefitting from it?

Most excess liquidity seems to be supporting the short-term trading of major financial houses – which helps explain the furor over the Volcker Rule, designed with the sole purpose of walling off risk trading from deposit taking (a proposition that a tenth-grader could clearly articulate in a single sentence – do you know a tenth grader who wants to be President?)

Wealthy folks are going to get wealthier through this artificial inflation in asset prices. This has been the effect of each previous round of money printing, and is likely to continue. But each successive round of QE also takes a moral chunk out of the nation’s Middle Class, not to mention shredding American credibility in the global marketplace. Our markets used to be the gleaming city on the hill. Now they are just the Best House in a Bad Neighborhood. How long before they turn into a slum?

Hedgeye’s institutional clients were treated this week to an exclusive conference call with George Friedman, founder and chairman of Stratfor, the global intelligence and strategic risk assessment consultancy. Friedman says the decimation of the middle class brought about by government neglect and economic malaise has historically been a key indicator of pending social unrest. We think America still has a way to go before chaos strikes, but we remember that Secretary Paulson got Congress to trigger TARP by predicting there would be marshal law within a matter of days – a dire prediction that this nation’s leaders bought into. TARP was passed with a large number of legislators never having even read the bill.

If you were worried that Washington might actually get some control over Bad Actors in the financial sector, you can breathe easy. All that posturing and crying “Sh*t!” in a crowded Senate hearing made for mildly engaging reality TV, but in the end Business As Usual remains the mantra in the City of the Perpetual Extended Palm. (For colorful commentary on the Senate financial crisis hearings, and other Washington-to-Wall-Street low points, see the Hedgeye e-book Fixing A Broken Wall Street). Bernanke’s fiddling in the system has the effect of trashing the Dollar, and of spiking asset prices – the value of stocks in your 401(K) just went up, but so did the price of gas, effectively an instantaneous tax hike. By creating waves of volatility in the markets, Bernanke is doing his utmost to keep the bankers banking and the traders trading.

To return to scary summer movie metaphors, while you are out frolicking in the surf, why are the Central Planners avoiding the sunlight? Are they vampires, or do they just not like being around We The People? Be careful out there: even at low tide you won’t see the shark until it’s upon you.

Sector Spotlight: Industrials – Who’s Stalking FedEx?

“No comment” is a splendid expression. I am using it again and again.

- Winston Churchill

“No comment” says Pershing Square Capital, responding to rumors that activist investor Bill Ackman, was raising funds to take a stake in FedEx (FDX). FDX traded up 6% on Tuesday on over 15 million shares, the biggest single-day trading volume since December 1998.

Hedgeye’s Industrials sector head Jay Van Sciver ran a Hedgeye Flash Call presenting the case for activist intervention. Van Sciver says the right kind of intervention could be a boon to shareholders. But he cautions that an activist would have to work with the Board and management. If an activist pushes for integration of FDX’s Ground and Express networks, Van Sciver says that would be a misguided and dangerous idea.

The Bull Case for FDX

Luck favors the prepared mind.

- Louis Pasteur

Van Sciver has featured FDX in our Investing Ideas newsletter and has been doggedly positive on the stock, sometimes as the lone voice pushing a well-wrought bullish thesis on FDX in the face of analysts who found the stock “Not In The Same League as UPS.”

When the rumor mill sparked a giant day in FDX shares, Van Sciver showed Hedgeye’s institutional clients that the same qualities that make FDX an outstanding investment opportunity also make it attractive to an activist: the company’s stock is cheap and its problems can be fixed. And while waiting for management – or an activist – to implement the fix, FDX continues to be a solid company with one of the world’s great franchises. Analyst ratings on the stock are generally positive, but Van Sciver says they dramatically underestimate the company’s potential.

FDX – A Very Friendly Takeover

Van Sciver looks at the opportunities in FDX the way an activist might see them, and how they could work through in implementation.

Valuation and Timing

The biggest drag on FDX is its Express business. Van Sciver’s earlier work makes the case that, at current valuations, FDX shareholders effectively own the Express business for free. This is due to lack of consistent management focus on profit margins, but also to a misunderstanding in the marketplace, where analysts and investors believe FDX suffers from not integrating its Ground and Express infrastructure. While the Express business does need work, what it doesn’t need is to be rolled in with FDX’s other operations.

Comparing FDX’s valuation metrics to UPS’, one would expect the company that is steadily taking away market share in the higher-margin, higher-growth Ground segment and has the larger Express franchise to carry a higher valuation. But on almost all standard analysts’ metrics, UPS stock is accorded much higher valuations than FDX.

Van Sciver says FDX’s dramatically improving profitability and growth, both off a lower base than UPS, should provide a springboard for earnings and stock price, and a focused activist might bring those gains sooner.

Are you listening, Mr. Icahn?

FDX’s Discount to UPS

Here’s where it’s “all over but the shouting.” FDX’s granite-solid Ground franchise is steadily taking share from UPS. Its Express business should enjoy scale advantages over UPS, but the division has suffered from high capital requirements combined with low returns, in part because of aggressive expansion. Van Sciver says Express is the primary opportunity for long-term investors – sooner or later management is likely to work this operation up to much higher profitability. For an activist, the objective would be sooner.

Excellent Industry Structure

FDX competes in an industry that is favorably structured from the perspective of participants. There are only a few major players – DHL, UPS, FDX. Barriers to entry are massive, including such concerns as acquiring your own fleet of trucks and aircraft, and negotiating access at airports all around the world.

In the US, there are two players: FDX and UPS. Outside of the US they share the rest of the globe with DHL and, to a lesser extent, TNT.

One of FDX’s biggest cost advantages is its low cost of labor. Unlike unionized UPS, FDX operates mostly with non-union employees and, increasingly, with outside contractors. Van Sciver believes that the difference in total compensation between UPS and FDX employees should continue to be a significant driver of share gains.

It is in the Express business that FDX’s margins still lag, with excess capacity creating a drag on the whole company. Much of this excess capacity comes from management’s deliberate strategy of capturing market share globally, at the expense of near-term profits. FDX has captured significant share in markets like Asia, but have seen profitability depressed in the process.

What’s An Activist To Do?

Van Sciver’s short To-Do list for an activist includes:

- Inject better discipline into capital allocation

- Improve dialogue with shareholders

- Focus management on profitability

- Don’t integrate Ground and Express.

FDX management has different priorities from shareholders at points, a lack of shareholder focus that has hurt the company’s relations with shareholders. An activist could put pressure on them to stay focused on profitability in their already-robust network. Van Sciver says an acquisition of TNT, for example, might make a lot of sense at this juncture.

CEO Fred Smith is a bona fide corporate titan, a legitimate visionary who has built one of the world’s great businesses. Perhaps not surprisingly for such a high-quality management team, Smith has not stacked the board of directors with his cronies. This is an unusual – maybe a non-obvious – consideration for an activist entering the picture to encourage “self-help” and make the existing company better at what it already does.

Finally, the fly in the analytical ointment has long been perceived inefficiency between the Ground and Express operating parallel infrastructures. FDX is routinely criticized for “inefficiency,” but Van Sciver says integrating these operations may actually kill FDX’s advantages. First, it could open up the Ground business to unionization, and the joint handling of Ground packages could jeopardize Express employees’ Railway Labor Act coverage, also facilitating unionization in that division. This could undermine FDX’s cost advantage, leaving UPS the big winner. FDX’s infrastructure is definitely not broke, says Van Sciver, so please, Mr. Activist, don’t try to fix it.

Conclusion

FDX is one of the world’s great franchises. Van Sciver’s says the sum of today’s parts, with improved margins in its Express business, could yield a stock price more than 50% above where it currently trades. An activist who is willing to cooperate could be just the thing to focus management to get there. It would require someone willing to partner with Fred Smith, rather than going head to head with him.

Any takers?

Investing Term of the Week: Buy Side, Sell Side

If you’ve run out of depressing, disgusting and demeaning voyeuristic options for summer reading, you may want to try the latest Wall Street tell-all book, The Buy Side, the real-life story of a man who was born with it all, made it all, had it all – then smoked, drank and mainlined it all, and is now hoping to get paid seven figures by writing about it all.

The author was formerly a trader at Galleon Group, home of convicted felon Raj Rajaratnam. The book purports to Tell It Like It Was in the halls of one of the most successful financial firms on the planet and a firm that, as court proceedings subsequently showed, took the notion of Wall Street’s “Buy Side” to new levels.

Market pros generally are divided into two camps, known as the Buy Side and the Sell Side. There is a significant difference in the way securities analysts follow and report on the sectors and companies they follow.

As you may divine from the terms, the Sell Side creates products, which it peddles to the Buy Side. What you may not understand is that the Buy Side is generally required to buy, as many portfolio managers have a contractual mandate to be 100% invested at all times. This keeps the Sell side in business, but often jeopardizes your portfolio. Here’s one secret every investor should know: You never have to buy or sell anything. Unlike the manager of a long-only stock mutual fund, you have the option of getting out entirely and going to cash when storm clouds gather on the horizon. “Gee, the water looks kinda choppy today…” “Never mind!” says the mutual fund manager. “In you go! Shark? I don’t see any – !!!”

Sell Side analysts work for brokerage firms and are compensated in trading commissions. The only way for a Sell Side analyst to earn a living is by convincing people to trade. Responding to Bernanke’s latest manipulation of the markets, Hedgeye CEO McCullough said in exasperation, “He’s chopping off the legs of US economic growth. I’m tempted to just sit out the rest of the year!” But on the traditional Sell Side, no one gets paid for issuing a report saying “our markets are psychotic – best not do anything this year.”

Historically, sell side analysts have also been exposed to real conflicts of interest when their firm performs investment banking for a company they cover. It is not uncommon for analysts to “reiterate” a positive recommendation on a company the day after the stock takes a dive. While these figures are not disclosed, it is often a safe bet that major institutional clients of the brokerage firm have sizeable positions in the stocks in question. A reiterated BUY recommendation can help reflate their portfolios – or even provide liquidity for them to get out while the getting’s good.

More subtly, investors believe they get better value from research that comes directly from management (sort of “Inside Information Lite”) so sell side analysts cherish their own relationship with the senior executives of the companies they cover. An analyst who asks uncomfortable questions – or actually writes negative research on a company – will find the CFO no longer returns their phone calls, and they don’t get to ask their questions at analyst day meetings with management.

Sell side firms also do a brisk business in “corporate access” (“Inside Information Not-So-Lite”) arranging one-on-one meetings between the investor and management. Sell side analysts may not even be present at these sit-downs, but their firm racks up a fee, often in the tens of thousands of dollars. Academic studies show that hedge fund managers who regularly obtain corporate access perform several percentage points better than the average. All right, we know: “correlation” is not the same as “causation.” Probably why Congress doesn’t think this form of inside information is important.

The Buy Side is completely different. While Sell Side analysts are assigned a list of companies and told to write maintenance research, to service the accounts that hold these positions, and work the relationships with investors and with corporate managements, Buy Siders have one job only: to be right.

The analytical tools used by both groups are essentially the same, including relying on each other’s work. Buy siders get access to sell side research, but most sell siders have free access to all the other research in their sector anyway, so what is really significant is the order in which they absorb the information, and the weight they give to data points. A sell sider’s value is not in being right on a stock call. More often it is a key bit of information or an unusual data point that gets the buy side client’s interest. If the buy side analyst likes the idea, his firm will put a trade through the sell sider’s trading desk. If the trade works out, the sell sider gets paid a commission, and the buy sider gets told “keep up the good work.” If the trade loses, the sell side analyst still gets paid the commission. But the buy sider might be told “pack up your desk.”

Hedgeye was founded on the principles of Transparency, Accountability and Trust. Our simple objective is to be your personal Buy Side research team. With no trading, no commission sharing, and no money under management, our mission is to democratize investment research by offering individuals the same depth of research and the same quality of insight that we provide to some of the world’s top money managers – and with the same timing.

We believe our structure has removed the inherent conflicts that have plagued Wall Street for so long. Without trying to sound too angelic, we’re battling not merely entrenched opinion, but an industry structure that is inimical to the investor’s best interests. It’s hard trying to be transparent in an industry built on opacity. It’s hard to work in the best interest of the investor in an industry where conflict of interest has been the primary driver of revenues. We don’t criticize our brothers and sisters in the trenches of Finance. Like all true revolutionaries, we invite them to join us.

You are now a Buy Sider. Welcome to the struggle.