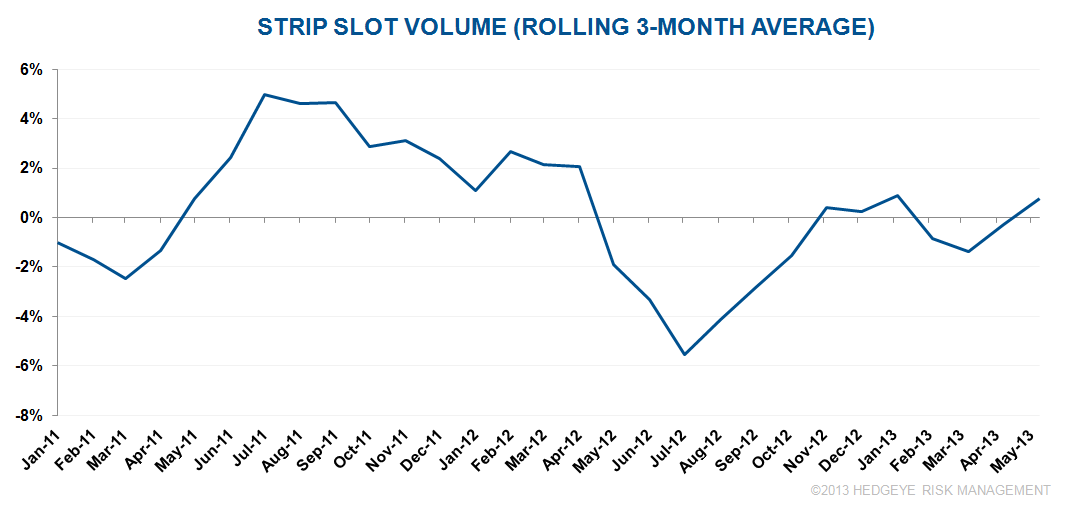

Core metrics were solid in May driving 6% YoY GGR growth. Volatile Baccarat the laggard.

On the surface, May GGR growth of “only” 6% looks disappointing since we were expecting mid-teens growth off of low hold last year. However, the core metric of slot volume was actually strong. Baccarat drop actually declined 13% and hold was a little lower than normal which drove the negative variance from our estimate. We would focus on the strength of slot volume which suggests an increasingly healthier Las Vegas Strip.

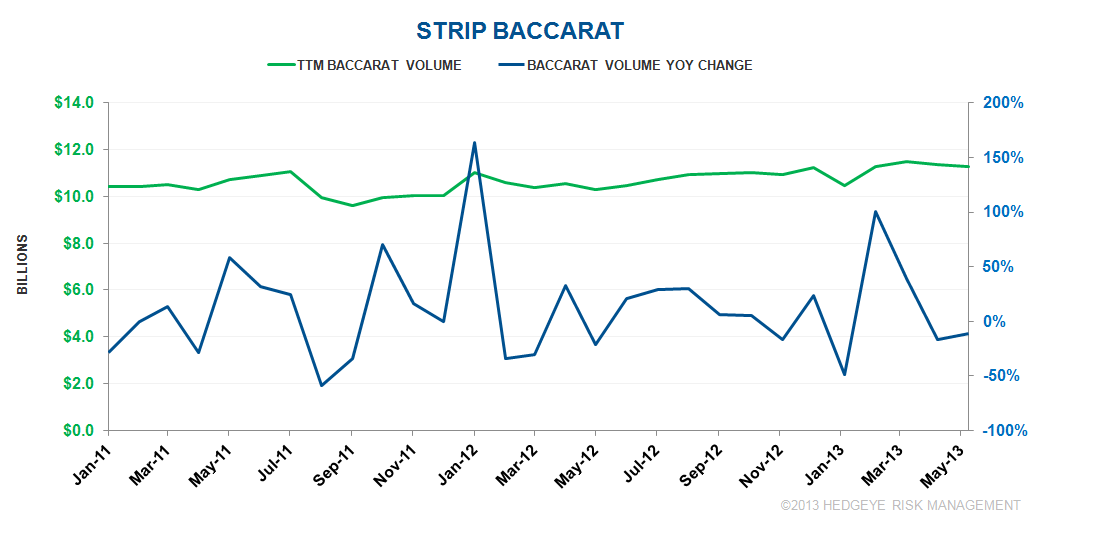

Baccarat drop and revenue are notoriously volatile. Following February and March YoY growth of 100% and 39%, respectively, Baccarat drop fell 17% and 11%, respectively in April and May. History suggests June and/or July should show marked improvement. Typically, negative Baccarat months are followed by strong months due to “whale play” timing. The following chart displays the YoY volatility in monthly volume but also shows that the annual volume is fairly consistent and generally up.