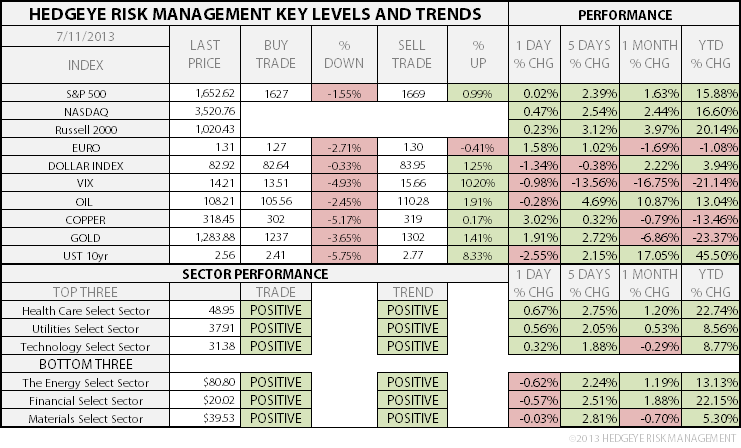

TODAY’S S&P 500 SET-UP – July 11, 2013

As we look at today's setup for the S&P 500, the range is 42 points or 1.55% downside to 1627 and 0.99% upside to 1669.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

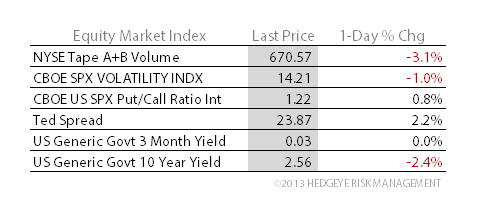

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.22 from 2.27

- VIX closed at 14.21 1 day percent change of -0.98%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Import Price Index, M/m, June, est. 0.0% (pr. -0.6%)

- 8:30am: Init Jobless Claims, week of July 6, est. 340k

- 9:45am: Bloomberg Cons Comfort, week of July 7 (pr. -27.5)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

- 11am: Fed’s Tarullo testifies on regulation to Senate

- 11am: Fed to buy $1b-$1.5b TIPS in 7/15/2017-2/15/2043 sector

- 1pm: U.S. to sell $13b 30Y bonds in reopening

- 2pm: Monthly Budget Statement, June, est. $100b

GOVERNMENT:

- 9am: U.S.-China Economic and Security Review Commission holds roundtable on deterring cyber theft

- 11am: Senate Banking, Housing and Urban Affairs Cmte hearing on “Mitigating Systemic Risk Through Wall Street Reforms,” w/ Fed Governor Daniel Tarullo, FDIC Chairman Martin Gruenberg, Comptroller of the Currency Tom Curry

- 3:30pm: ACLU, Assn for Molecular Pathology briefing on Supreme Court decision to strike down patents on human genes

WHAT TO WATCH

- June U.S. retail sales likely helped by heat, pent-up demand

- Euronext will be spun off in IPO mid-2014, Cerutti says

- Microsoft reorganization to be announced today: AllThings D

- BOJ keeps monetary policy on hold as recovery signs seen

- U.S., Europe said poised to announce agreement on swap rules

- PC shipments fall for 5th quarter even as U.S. decline slows

- Bank Indonesia raises benchmark rate more than forecast to 6.5%

- Luxembourg PM to resign amid security service spying probe

- Heineken sells Hartwall unit to Royal Unibrew for $614m

- Sprint drops Nextel from co. name as SoftBank takes control

EARNINGS:

- Commerce Bancshares (CBSH) 7am, $0.71

- Corus Entertainment (CJR/B CN) 7am, C$0.51

- Progressive (PGR) 8:12am, $0.41

- Bank of the Ozarks (OZRK) 6pm, $0.57

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- IEA Sees 20-Year Supply Peak Outpacing Demand Recovery in 2014

- Corn Bets Turn Bearish as Rain Revives U.S. Crops: Commodities

- Thai Sugar Harvest Seen at Record Adding to Global Surplus

- WTI Trades Near 15-Month High as U.S. Crude Inventories Plunge

- Copper Reaches Three-Week High on Outlook for Further Stimulus

- Gold Nears $1,300 After Fed’s Bernanke Backs Sustained Stimulus

- Commodity Traders Face New Squeeze as Storage Congestion Spreads

- Crude-by-Rail Profits Fall as WTI-Brent Narrows: Energy Markets

- Raw Sugar Rebounds in New York After Brazil Raises Interest Rate

- Japan Purchases Alternatives to Oregon Wheat in Tender

- Zinc May Advance to $1,974 on Retracement: Technical Analysis

- South Africa Mine Wage Talks Open With Highest Demands on Record

- Iron Ore Bests Metals as Prices Have Gone Nowhere Since 1913

- Corn Gains as Investors Weigh Stress Risk to Record U.S. Crop

CURRENCIES

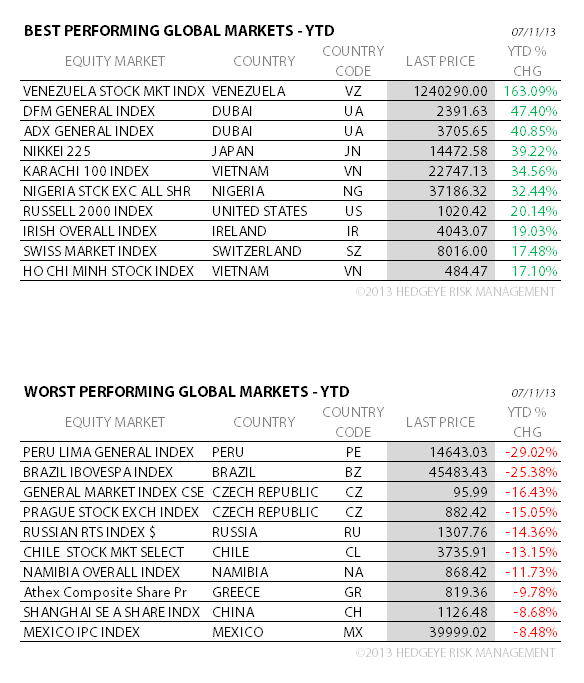

GLOBAL PERFORMANCE

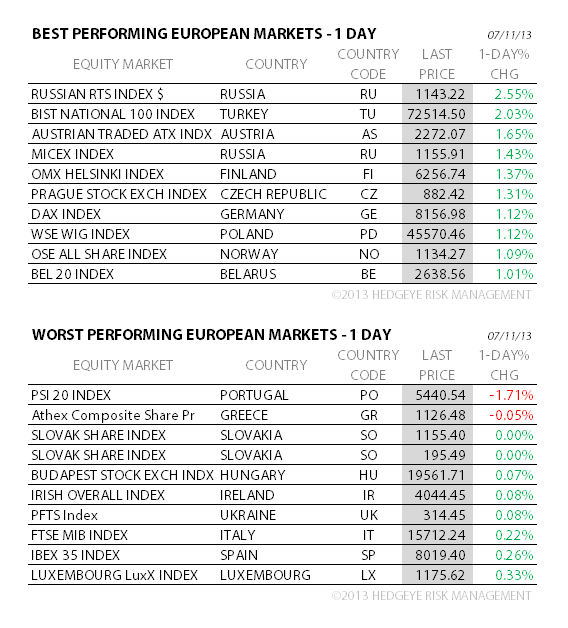

EUROPEAN MARKETS

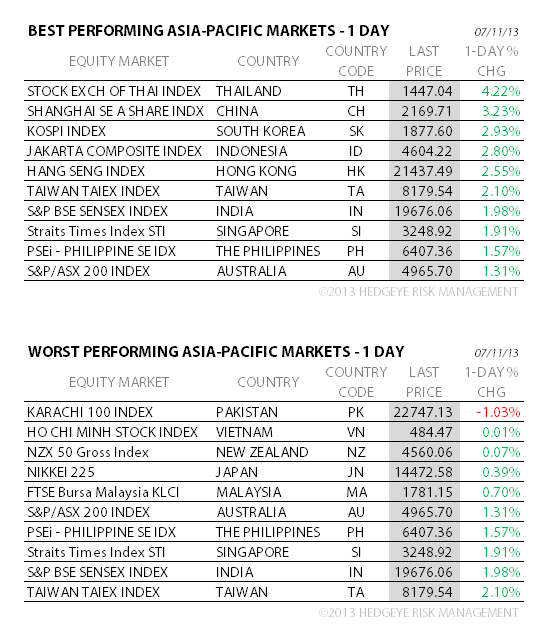

ASIAN MARKETS

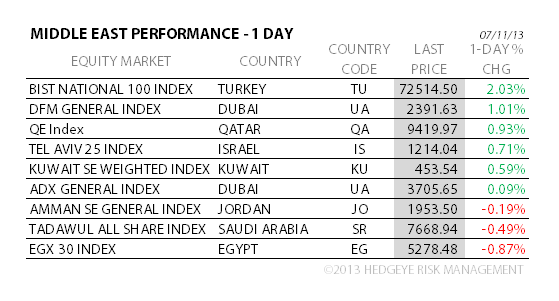

MIDDLE EAST

The Hedgeye Macro Team