This note was originally published at 8am on June 21, 2013 for Hedgeye subscribers.

“A government’s first job should be to protect its citizens. But that should be based on informed consent, not blind trust.”

-The Economist

I was flying back from California last night and those few sentences in The Economist article titled “Secrets, lies and America’s spies” got me thinking about the Fed. The article, of course, had nothing to do with Bernanke. But it had everything to do with trust.

How can you trust what you cannot see? I am Canadian, so hard core Americans will have to check my work on this – but didn’t the US Constitution provide a clause for this thing called free elections?

While I hardly doubt Franklin and Jefferson envisioned an America that was hostage to an un-elected and un-accountable central planner’s qualitative views of economic gravity, that doesn’t matter right now – because that’s what you have. The blind trust this country has put in Bernanke’s ability to “smooth” the Waterfall of interconnected risk was a mistake. Now we have to deal with his mess.

Back to the Global Macro Grind…

So how did you like yesterday anyway? Feeling good yet? Want to get Bernanke whispering to Hilsenrath around 320PM EST this afternoon that he didn’t really mean it? Wouldn’t that be cool – then we could do the whole over the Waterfall thing together again!

If you are going to tell me that markets trust how Bernanke is going to manage this going forward, I am going to tell you that you are probably already hammered. It’s always 5 o’clock on a Friday somewhere.

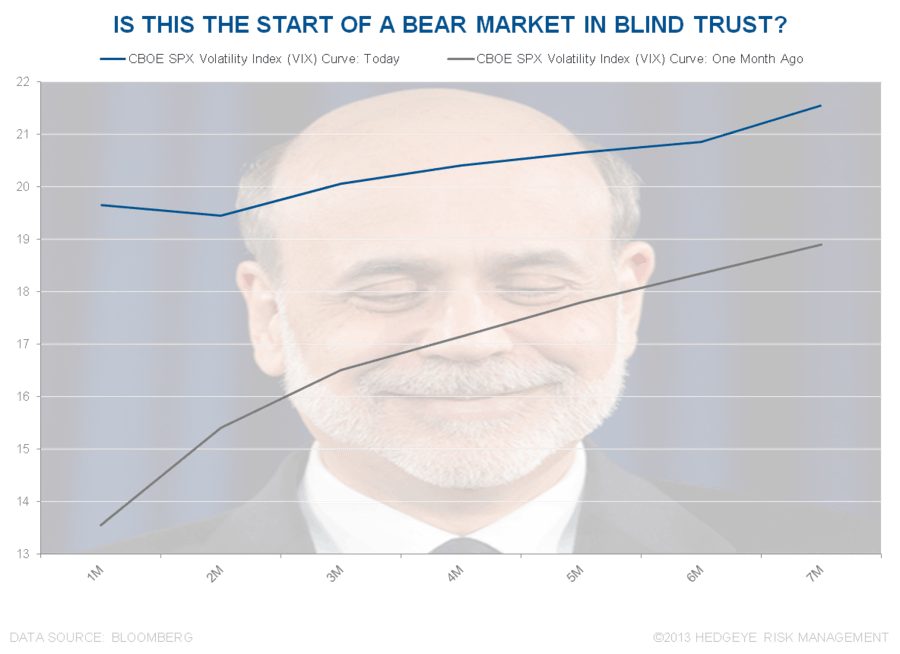

When markets don’t trust something, the forward curve of implied volatility starts to rise. When they really don’t trust something, that volatility rises at a faster rate. It’s called convexity.

In terms of implied volatility in everything that was already crashing (Gold, Treasuries, Emerging Markets, etc), that concept has been pretty straightforward for going on 6 months now. For US Equities, it’s relatively new.

Here are front-month US Equity Volatility’s (VIX) TRADEs and TRENDs:

- Week-to-date, the VIX = +19.4%

- Month-over-month, the VIX = +57.2%

- In the last 3 months, the VIX = +61.6%

In other words, as US consumption, employment, and housing #GrowthAccelerated in the last 3 months, US Equity market expectations went right squirrel. How screwed up is that?

It makes sense though. We have a US Federal Reserve that is A) horrendous in terms of forecasting and B) compromised and conflicted in terms of timing its “communications.” Bernanke made his legacy bed – now we all have to sleep in it.

Another way to think about US growth expectations is bond yields – they love growth:

- Week-to-date UST 10yr Yield = +29 basis points to 2.42%

- Month-over-month UST 10yr Yield = +45 basis points

- In the last 6 months, UST 10yr Yield = +62 basis points

In other words, 10yr Yields ripping yesterday wasn’t new – they’ve been making higher-lows and higher-highs since the November 2012 all-time low. In the last 6 months, 10yr US Treasury Yields are up +35%!

Captain Keynesian is going to say, whoa, whoa, on that Mucker – you are using % moves instead of absolutes. Ah yes, professors, and that’s the precisely the point. Right back at ya – you created an expectation of an absolute zero bound that was reckless and un-precedented.

What else has been front-running Bernanke’s Blind Trust of 0% rates to infinity-and-beyond? Gold:

- Week-to-date Gold = -7.7%! to $1280/oz

- YTD Gold = -23.9% #crashing

- In the last 6 months, Gold = -22.5% #crashing

Gold hates growth and gold loved Bernanke’s anti-consumption growth Policies To Inflate. Period.

Now, to be fair to the community who trades on Washington “consultant” whispers, if you do have a Hilsy rumor in your back pocket this morning, the first thing you’d probably do with that is buy Gold, lever yourself up with some Oil futures, and short Treasuries.

Isn’t that just great for America!

The sad reality is that Americans don’t trust Bernanke’s Fed as far as they can throw Cramer or his buddy’s gnome. The American zeitgeist of distrust in politically driven institutions reaches far beyond the IRS. It’s in your mind each and every market day.

The best thing President Obama can do is say goodbye to Ben S. Bernanke’s concepts of “innovation and communication.” Unless you are all interested in scaling back up the bond-buying Waterfall, ripping a VIX 30 handle, and doing yesterday over and over and over again, that is.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1253-1332, $100.80-103.96, $81.11-82.19, 96.18-97.92, 2.24-2.46%, 17.25-21.56, and 1583-1629, respectively.

Best of luck out there today and enjoy your weekend,

KM

Keith R. McCullough

Chief Executive Officer