TODAY’S S&P 500 SET-UP – July 2, 2013

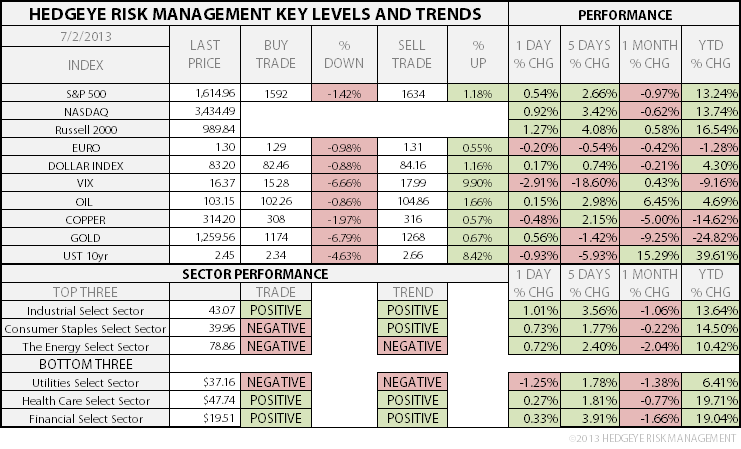

As we look at today's setup for the S&P 500, the range is 42 points or 1.42% downside to 1592 and 1.18% upside to 1634.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.11 from 2.13

- VIX closed at 16.37 1 day percent change of -2.91%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 9:45am: ISM New York, June (prior 54.4)

- 10: Factory Orders, May, est. 2% (prior 1%)

- 10am: IBD/TIPP Economic Optimism, July, est. 50 (prior 49)

- 11am: Fed to buy $1.25b-$1.75b debt in 2/15/36-5/15/43 range

- 11:30am: U.S. to sell 4W bills

- 12:30pm: Fed’s Dudley speaks on economy in Stamford, Conn.

- 4:30pm: API crude, oil product inventories

- 5:45pm: Fed’s Powell speaks on regulation in N.Y.

GOVERNMENT:

- Fed governors meet on final rulemaking for Basel III, 9:30am

- SEC holds closed mtg on enforcement matters, 11am

- House, Senate not in session

- Senate Appropriations Chairman Barbara Mikulski, D-Md.; Commerce Secretary Penny Pritzker hold news conference following tour of NOAA Center for Weather and Climate Prediction. Riverdale, Md., 10:30am

- USTR holds mtg on Japan’s participation in TPP talks, 9:30am

- Kerry participates in ASEAN Regional Forum in Brunei

WHAT TO WATCH

- Federal Reserve set to vote today on Basel capital ratios

- June auto sales; SAAR may be best since Dec. 2007

- Nielsen Holdings to replace Sprint Nextel in S&P 500

- Linn, LinnCo disclose informal SEC inquiry over Berry deal

- Honda, GM to jointly develop fuel-cell systems, Nikkei says

- Tyco gets notices increasing co.’s taxable income by ~$2.9b

- AMR-US Airways deal investigated by 19 state attorneys general

- Immigration bill details to benefit contractors, WP says

- Swiss Re, Lloyd’s examined for possible Iran violations

- L-T care insurance rates rise on fewer providers, WSJ says

EARNINGS:

- Constellation Brands (STZ) 7:30am, $0.40

- Acuity Brands (AYI) 8:25am, $0.89

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Climbs for Third Day to Extend Rebound From 34-Month Low

- Gold Traders Seeking Floor After $66 Billion Rout: Commodities

- WTI Crude Trades Near Two-Week High as Stockpiles Seen Falling

- Wheat Snaps Slump as Egypt Issues First Tender Since February

- India Urges Resisting Gold as Curbs Fail to Stem Currency Slump

- UBS Starts Gold-Vault Service in Singapore Amid Bullion Rout

- Goldman Outlook Right as Brent-WTI Narrows to $5: Energy Markets

- Palm Oil Drops to Six-Week Low as Weak Rupee Curbs Indian Demand

- Rebar Rises on Higher Ore Prices, Town Redevelopment Optimism

- 90% of EU Oil Demand Growth Stems From Outside OECD: Bear Case

- Crude Supplies Fall to Four-Week Low in Survey on Refinery Runs

- Palm Oil Seen Dropping to Lowest Since May: Technical Analysis

- Chinese Aluminum Production at All-Time High in May: BI Chart

- Tin Reaches a Two-Week High Before Report on U.S. Factory Orders

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team