This note was originally published at 8am on June 06, 2013 for Hedgeye subscribers.

“One main factor in the upward trend of animal life has been the power of wandering.”

-Alfred North Whitehead

Rather than get all googly eyed about modern day central planners who are long of social science dogma and short of math, I tend to wander backwards when looking for direction. History is my contextual guide, and so are her credible sources.

Whitehead was one of the British math guys (1861-1947) who wandered outside of academia’s box. He co-authored Principia Mathematica with one of the world’s premier strategists (Bertrand Russell) and was an early adopter of what we now call Chaos Theory.

From considering the metaphysical global macro market to the process you have developed to absorb it, what is that you do when markets go against you? What do we do when immediate-term TRADEs wander from the intermediate-term TRENDs? Bull or bear? Personally, I am ok with being called an animal.

Back to the Global Macro Grind…

I had a very bad day yesterday. Yes, for those of us who timestamp every move we make, they do happen. But what, precisely, was happening? Was my first move to do more of what wasn’t working? Or was it a better decision to wait and watch?

The good news about today is that Mr Market gives us direct feedback on however we answered those questions. Right or wrong, we are tasked with always questioning the behavioral side of our decision making process. #evolve

To put yesterday’s -1.38% drop (SP500) in context, it was the 5th worst day for US stocks in 2013:

- February 28, 2013 = -1.83%

- April 15, 2013 = -2.30%

- April 17, 2013 = -1.43%

- May 31, 2013 = -1.43%

When I was a younger man trading on simple moving averages and voodoo technical charting systems that my bosses would push down on me, one-factor price moves could really throw me for an emotional loop.

Now I use a baseline 3-factor model that includes PRICE/VOLUME/VOLATILITY parameters and predictive tracking algorithms. And it’s that last little critter (VOLATILITY) that helps me sometimes front-run the proactively predictable behavior of machines.

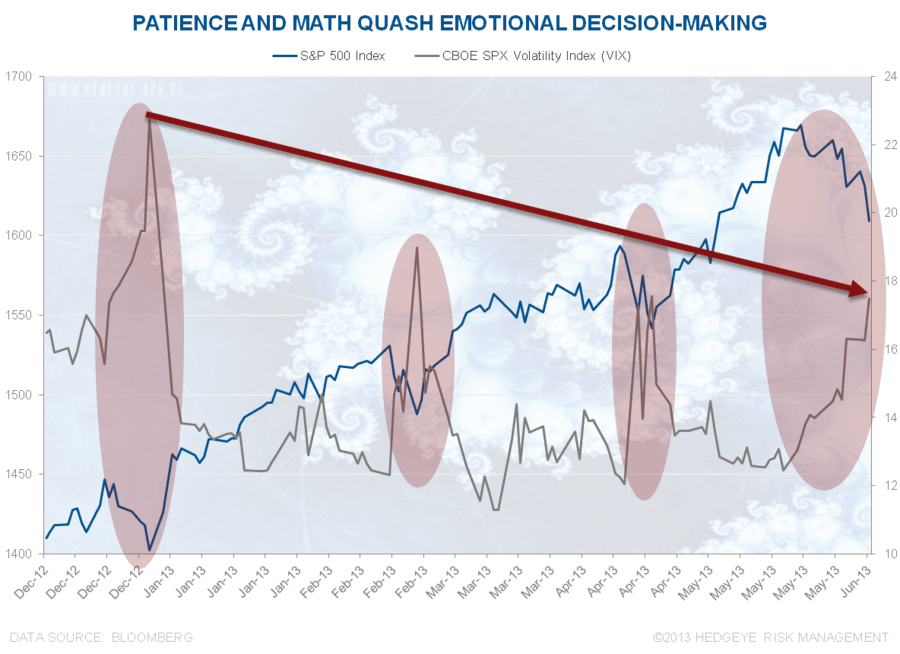

What all 5 of the worst US stock market down days have in common is front-month US Equity volatility (VIX) seeing a very short-term capitulation to lower TREND duration highs. Here’s that history of VIX closing prices:

- February 25, 2013 = 18.99

- April 15, 2013 = 17.27

- April 18, 2013 = 17.56

- May 31, 2013 = 16.30

And yesterday, the VIX closed +7.6% on the day at 17.50.

So, what say you Mr Mucker, TRADE or TREND? That’s easy:

- SP500 = bearish TRADE; bullish TREND

- VIX = bullish TRADE; bearish TREND

For those of you who are new to reading my rants, in our model TRADEs are 3 weeks or less and TRENDs are 3 months or more. I built the model this way so that I don’t let my emotions allow me to wander too far away from fundamental research trends.

Freaking out and selling at every higher-low within a bullish TREND is called losing money. And since that would violate Rule #1 in our risk management process, we don’t want to be like that.

Why is the intermediate-term TREND for US stocks bullish and for fear bearish? I think the fundamental research answer to this quantitatively prefaced question is crystal clear – what everyone lives in fear of (#GrowthSlowing) is now #GrowthAccelerating.

Darius Dale will show you this in our Chart of The Day (6 month TREND duration charts)

- US Equity Volatility is still crashing (-23% from its Johnny Boehner sequestration fear-mongering high in December 2012)

- US Equities (SPY) continue to make a series of higher-lows on selloffs as the VIX makes lower-highs

If the VIX can’t close above 18.99 and the SP500 can’t snap my TREND support line of 1577, what I’ll be doing from here is doing more of what we have been doing for the past 6 months (buying the damn dips in US Consumption and shorting almost everything Commodities).

No, that doesn’t mean I bought all the way down yesterday. It actually meant I did a whole lot of nothing. The SP500’s TRADE line broke, so why hurry when I can either buy lower or buy on another TRADE breakout above 1624 SPX when my convictions are confirmed?

Of all the bubbles Bernanke has helped perpetuate, one of the biggest is fear. The fear of change (rates rising) in this market is pervasive. But don’t wander too far from the TREND here my friends. Shorting fear and buying growth has been right; stay with it until the mathematical signals collide with the fundamentals. If they change, we will.

Our immediate-term Risk Ranges for Gold, Oil (Brent), US Dollar, USD/YEN, UST 10yr Yield, VIX, and the SP500 are now $1361-1419, $100.24-104.42, $82.21-83.32, 98.71-103.02, 2.01-2.23%, 15.31-17.91, and 1601-1624, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer