TODAY’S S&P 500 SET-UP – June 14, 2013

As we look at today's setup for the S&P 500, the range is 48 points or 1.92% downside to 1605 and 1.02% upside to 1653.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.85 from 1.87

- VIX closed at 16.41 1 day percent change of -11.73%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Producer Price Index, May, est. 0.1% (prior -0.7%)

- 8:30am: Current Acct Bal., 1Q, est. -$110.8b (pr -$110.4b)

- 9:15am: Industrial Production, May, est. 0.2% (prior -0.5%)

- 9:15am: Capacity Utilization, May, est. 77.8% (prior 77.8%)

- 9:15am: Manuf (SIC) Production, May, est. 0.1% (prior -0.4%)

- 9:55am: UMich. cons. sentiment index, June prelim, est. 84.5

- 11am: Fed to buy $1.25b-$1.75b notes in 2036-2043 sector

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Iranian presidential election will be the first since 2009, which sparked street protests amid allegations that MahmoudAhmadinejad’s re-election was the result of ballot fraud

- 8:30am: Sen. Max Baucus, Rep. Dave Camp discuss tax overhaul efforts at CSM breakfast

- IMF Managing Director Christine Lagarde holds press conference on U.S. economy

WHAT TO WATCH

- Exchanges preparing pilot programs for changing tick sizes

- FX rates said to face global regulation after Libor review

- U.S. agencies said to swap intelligence w/thousands of firms

- Johnson & Johnson sells last of 25.4m shares of Elan

- SoftBank, Sprint dismiss Dish claim to FCC of broken pledge

- Visa sues Wal-Mart to stop co. from filing swipe fee claims

- Marchionne said close on Fiat-Chrysler refinancing agreement

- Airbus A350 becomes airborne as test pilots start first flight

- Boeing seen reaping $6b/yr on 787 output rising again

- Senate committee approves $625b defense spending measure

- Wal-Mart says approved Ranbaxy products “safe and effective”

- Gene patent ruling triggers race to mkt cancer risk scans

- Bernanke, G-8 Summit, Paris Air Show, NBA: Wk Ahead June 15-22

EARNINGS

- Smithfield Foods (SFD) 6am, $0.43

- NGL Energy Partners (NGL) Bef-Mkt, $1.03

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Corn Set for Weekly Drop as Demand Slows and U.S. Crop Rebounds

- Gold Bears Return as ETP Rout Extends to 17th Week: Commodities

- Copper Climbs on Indications of Rebounding Economy in the U.S.

- WTI Rises to 10-Week High Amid U.S. Growth, Middle East Tensions

- Aluminum Fees Immune to Abenomics as Japan Buyers Don’t Budge

- Gold Declines as Investors Cut ETP Holdings on Stimulus Outlook

- Thailand Sets Record Sugar Production Target of 13 Million Tons

- Rebar Trades Near Lowest Level in Nine Months on China Concerns

- Lower Crop Prices Seen Erasing Savings in U.S. House Farm Plan

- Nickel Glut Fuels Price Slump for LME Laggard: Chart of the Day

- U.K. Power Price to Double German on Wind, Solar: Energy Markets

- U.S.-Europe Diesel Flow Seen Rising Amid Output at 23-Year High

- Oil Hunted in Mozambique After World’s Largest Gas Discoveries

- Crop Price Decline Top Commodity Opportunity at Goldman Sachs

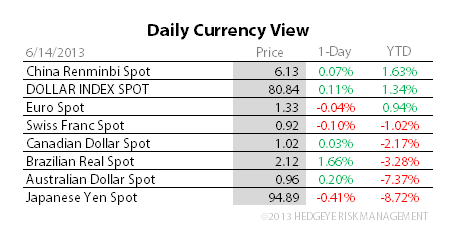

CURRENCIES

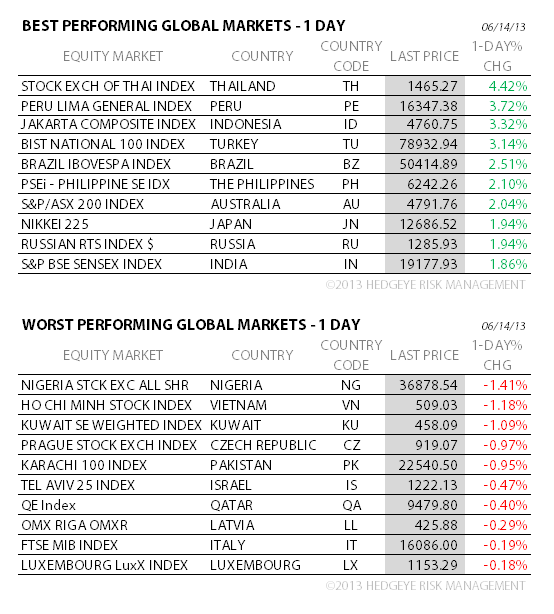

GLOBAL PERFORMANCE

EUROPEAN MARKETS

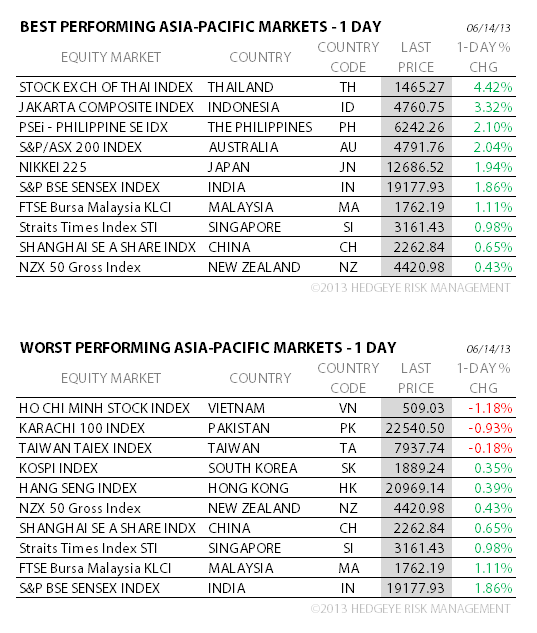

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team