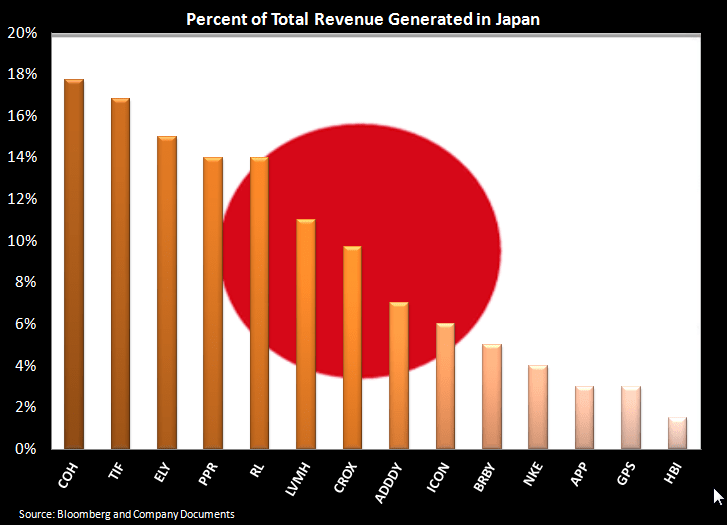

Our Macro team is bearish on Japan from a long-term TAIL perspective (see the latest of Darius Dale's notes below). And yes, it matters for US retailers. Here's a list of brands that have direct exposure to Japan. We've already heard some of the companies (like Ralph Lauren) talk about taking up prices in Japan to help mitigate currency fluctuations, but those actions are not enough to cover the whole deficit. That's when secondary exposure comes into play, as the primary brands look to extract value from other supply chain partners to maintain their margins. We wouldn't consider this as 'critical' for US Retail right now, but with raw material tailwinds coming to an end, and labor costs accelerating to the upside, it is not a welcomed change -- particularly with margins at peak. At a minimum, let's be aware of it.

06/13/13 02:05 PM EDT

JAPAN STRATEGY UPDATE: IS THE ABENOMICS TRADE OVER?

Takeaway: Trading Abenomics from here depends primarily on your specific investment duration.

SUMMARY BULLETS:

- All in, the BOJ’s opting to stand pat as the currency market demands additional easing measures is the primary reason for the recent bout of yen strength (up +9% vs. the USD since its 5/17 YTD low).

- More importantly, the USD/JPY cross has broken our intermediate-term TREND line of support at 95.95.

- To the extent you have been short the yen or playing the Abenomics Trade in ancillary vehicles, it may prove prudent to sell/reduce your exposure upon confirmation (i.e. give it time to breathe) of a breakdown through the TREND line.

- The long-term TAIL line of support is down at 88.67; that would be a good level to put the position back on/increase your exposure (as would a breakout back above the TREND line).

- As one of our core research views, we remain the bears on the Japanese yen with respect to the long-term TAIL. We’re merely attempting to manage the immediate-to-potentially-intermediate-term risk of the position.

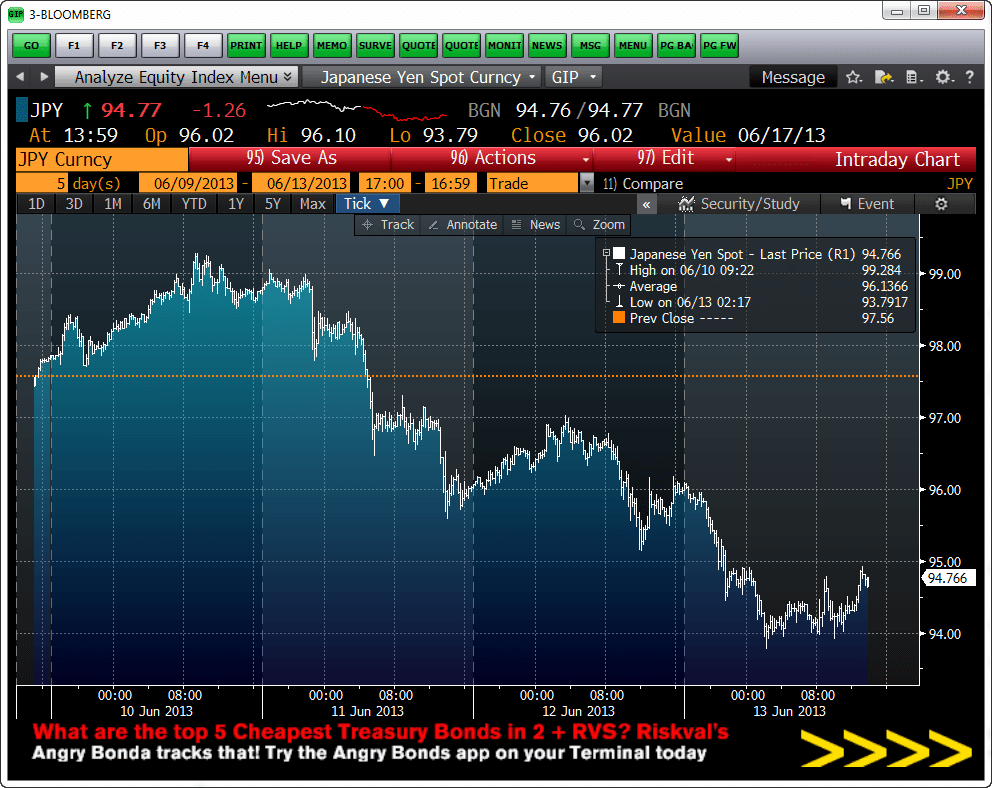

The minute-by-minute week-to-date chart of the dollar-yen tells us all we need to know about the Abenomics trade. Unlike last week’s sharp decline, the stair-step function exhibited in the week-to-date suggests that investors are slowly losing faith in the collective ability of Abe, Aso and Kuroda to deliver on the LDP’s contextually aggressive +3% nominal GDP and +2% inflation targets.

This is primarily due to the trifecta of headwinds that we outlined last Friday in a research note. Perhaps the most critical of those headwinds is the fact that the BOJ appears increasingly content to “play chicken” with market participants, meaning that they continue to stand pat on their previously outlined policies and guidance.

Essentially, they are asking the market to patiently trust that they’ll deliver the results that the Abe administration seeks with regards to not just ending structural deflation expectations, but instituting inflation and the broad-based expectation that inflation will be sustained. As we pointed out in a 3/15 research note titled, “JAPAN’S “INVERSE VOLCKER” MOMENT IS UPON US”, Japan’s monetary policy phase change is not unlike what the US experienced with the transition from Arthur Burns to Paul Volcker in the late 70s/early 80s.

Just today, BOJ policy board member Sayuri Shira warned that: A) it will take considerable time to achieve +2% inflation target given that the economy has been in a deflationary slump for 15 years and B) there needs to be more focus on the downside risks. She also affirmed previous guidance by BOJ Governor Haruhiko Kuroda that the board is not planning to implement additional programs to calm JGB market volatility, stating that “sufficient tools” already exist.

All in, the BOJ’s opting to stand pat as the currency market demands additional easing measures is the primary reason for the recent bout of yen strength (up +9% vs. the USD since its 5/17 YTD low). More importantly, the USD/JPY cross has broken our intermediate-term TREND line of support at 95.95.

To the extent you have been short the yen or playing the Abenomics Trade in ancillary vehicles, it may prove prudent to sell/reduce your exposure upon confirmation (i.e. give it time to breathe) of a breakdown through the TREND line. The long-term TAIL line of support is down at 88.67; that would be a good level to put the position back on/increase your exposure (as would a breakout back above the TREND line).

As one of our core research views, we remain the bears on the Japanese yen with respect to the long-term TAIL. We’re merely attempting to manage the immediate-to-potentially-intermediate-term risk of the position.

Darius Dale

Senior Analyst