EV Energy Partners (EVEP) remains a short on our Best Ideas list. We added it on 4/26/13 at $47/unit and have a 26% “unrealized gain” (not the LINN Energy kind) as of yesterday’s close. Our thesis is largely playing out as expected, and with EVEP $12 lower in short order, it is time to reevaluate.

For background information, see our prior work on EVEP:

4/26/13: Short EVEP: New "Best Idea"

5/2/13: EVEP: Beyond the Yield

5/10/13: EVEP is Still a Short

Conclusion: We are not “covering” the short here, but we would “lighten up.” Risk/reward is not what it once was, but we remain negative for two key reasons:

- Leverage/liquidity situation is dire; we believe that EVEP will raise equity in 2H13, and that is not yet a consensus view.

- There is no legitimate valuation support anywhere close to the current price, in our opinion. EVEP is overvalued relative to the intrinsic value of its own assets, as well as its E&P peers.

As of 3/31/13, EVEP had $944MM of long-term debt, $19MM of cash, $925MM of net debt, and a net derivative asset of $48MM (adjusted EV of $2.37B at $35/unit). Net debt increased $74MM sequentially in 1Q13, and assuming no A&D activity and no change in the distribution, net debt will increase ~$77MM every quarter for the next three quarters. If we draw the cash balance down to $0, that gets us to total long-term debt of $1,160MM at YE13. At that level the credit facility would be at $660MM, near its borrowing base limit of $710MM (EVEP has $500MM of senior notes (8.0%, 2019)).

In 2013, we estimate that EVEP will generate $159MM of open EBITDA and $33MM of hedge gains, for EBITDA of $191MM (note: we do not exclude unit-based compensation from EBITDA as EVEP does – that just doesn’t make sense to us). Current adjusted net debt/2013 open EBITDA is at 5.5x (($925MM - $48MM)/$159MM); current net debt/2013 EBITDA is at 4.8x ($944MM/$191MM). Using our YE13 net debt estimate at $1,160MM, leverage ratios will be at 7.1x adjusted net debt/open EBITDA and 6.0x net debt/EBITDA at year end. It’s also worth noting that net debt exceeds the value of the proved reserves (SEC PV-10 of $874MM at YE12). The point is that EVEP is dangerously over-levered – which we do not think is really appreciated – and needs to raise capital.

The levers that EVEP can pull are 1) asset sales and 2) equity raises. We think that we get both this year.

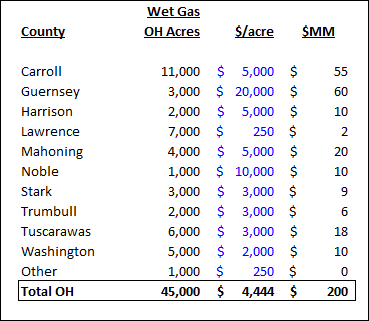

In our view, EVEP can sell down its Utica Ohio wet gas acreage for ~$200MM (45,000 net acres at $4,444/acre) – but it will be in a number of different transactions, and the timing is uncertain. Acreage prices in the Utica are still fluid, but we feel like we’ve given the benefit of the doubt to EVEP in our assumptions below:

We assume that the rest of the Utica acreage (volatile oil window, other OH, and all of PA Utica) does not get monetized (though a JV carry arrangement is possible).

Those proceeds are not enough. If EVEP manages to realize the full $200MM in proceeds in 2013 (unlikely), net debt will down to $960MM at YE13 – still over-levered by any measure – but it would not be long until EVEP is again bumping up against the borrowing base ceiling as in 2014 and 2015 EVEP needs to raise another $100MM and $60MM of capital, respectively, assuming the distribution is not cut.

If EVEP wants to maintain the current distribution – we think they do as cutting it is a death sentence – we think that it raises equity in 2H13 (perverse, but it is what it is). EVEP hasn’t done an equity deal since February 2012 when they sold 4MM shares at $67.95/unit (brilliantly done) for proceeds of $268MM. Suppose that this time around they raise $200MM at $34/unit – that would be 5.8MM new units, diluting exiting unitholders by 14%. That's what we're playing for.

---

As we have written previously, we believe that fair value for EVEP is in the low $20’s. We use traditional E&P valuation approaches (NAV and multiples of cash flow), not a yield target. We do not believe that EVEP’s current distribution is sustainable without consistently funding it with capital raises, so we think that method is inappropriate, and overvalues the enterprise. At the current price – $35/unit – EVEP trades at 2.7x EV/PV-10, 15.0x EV/2013 open EBITDA, and 12.0x EV/2014 open EBITDA. Compare those metrics with E&Ps that have better assets and better growth prospects and trade at 1.5x PV-10 and 5x EBITDA – and most E&Ps have acreage for sale and midstream businesses just as EVEP does.

---

We want to wait for our catalyst – equity raise – before “covering” our position. We don’t think it’s priced in yet, but maybe it’s starting to be. While EVEP is still very overpriced in our eyes, we understand that most investors and analysts do not look at EVEP the same way that we do, and we don’t expect them to “come our way.” We want to keep the position on, but would “lighten up,” as risk/reward is not what it was when we initiated the short at $47, and there are two potential catalysts that could squeeze EVEP higher: an DCF/unit accretive acquisition; and/or EVEP monetizes a small amount of acreage in the Utica for a high price, and investors extrapolate that number across its entire position.

Kevin Kaiser

Senior Analyst