“One of our strategies moving forward is to shift to a balance between our legacy of being family-friendly and adult-focused guest experiences, referencing our legacy. There is no assurance that this shift will be successful or that it will not negatively affect our family guest experience.”

- RRGB 2012 10-K, Risk Factors section

We are adding Red Robin Gourmet Burger to our Best Ideas on the short side. The stock has gotten ahead of the company’s fundamentals and future growth prospects.

Company Overview

- 468 full-service casual dining restaurants – 335 co-op and 133 franchised

- 5 limited service Red Robin Burger Works concepts

- Core concept is “family-focused”

- Seeking to strike balance between family legacy and “adult-focused experiences”

- FY13 estimated revenue growth of 4% to over $1 billion

- Operating margins, ROE, ROA, some of the lowest in casual dining

- 2.99x Debt/EBITDA

- 22% debt/Total Assets

PERFORMANCE VS THE S&P 500

The stock has outperformed by almost 60% over the past year and its strong performance versus peers has continued as earnings growth estimates have stagnated.

Current Setup

- Stock surging on increased expectations for a successful Red Robin “brand transformation”

- Additional investment will be required to secure brand transformation

- Capital spending unit growth is being accelerated in 2013

- Industry is still experiencing a secular declining traffic trends

- Guidance is for EPS an EPS recovery in 2013 and 2014

- Traffic negative in 1Q13 and comparisons get difficult for the balance of 2013

- Restaurant margins have improved 290bps over the last 2 years

Traffic Problem is Biggest Fundamental Red Flag

The company is in desperate need of a “brand transformation” to stem the decline in traffic

Capital Allocation

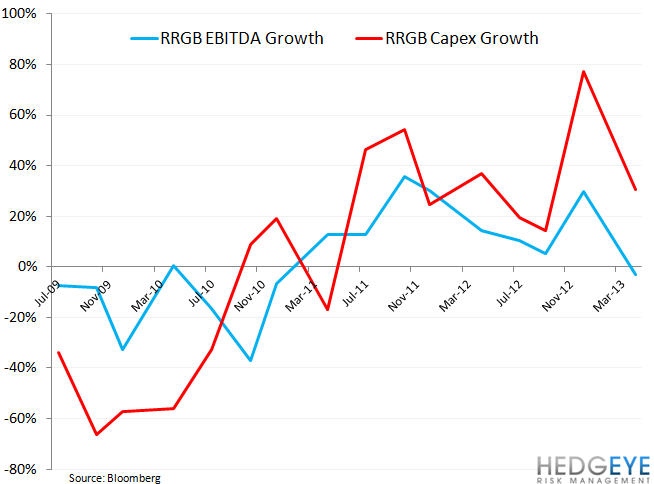

Capital allocation is one of the most important metrics for casual dining companies. In terms of RRGB’s capital spending, the following bullets and charts offer insight into the effectiveness of the company’s capital allocation decisions.

- Capex has been growing for three years

- Expected to increase 17% in 2013

- ROIIC likely to decelerate in 2013

- Unit growth accelerating with Red Robin, mid-size, and new Burger Works concepts

Repeating Others’ Mistakes

The foot print expansion is leading to declining returns for the company. The question that we, and others, have about the strategy is why so many different initiatives need to be pursued at once. Specifically, the company is growing Red Robin in two different sizes, expanding its Burger Works QSR concept which seems to be producing mixed results, and trying to transform the consumer’s perception of Red Robin as a brand. In our view, this amounts to the company taking on more tasks than it can complete effectively while managing its capital prudently.

Brand transformation is difficult to achieve, for several reasons. Below are some of the concerns we have about RRGB’s particular strategy.

- Moving away from core customers carries risk

- Bar remodel had limited impact

- Guiding to strong returns in “full transformed” units (only?)

- Red Robin brand perception is entrenched, significant messaging required to adjust

- Bar Works off to a difficult start as real estate and financial performance refinements ongoing

3Q12 IS RRGB’S WATERLOO

- Difficult SRS comparisons

- Lowest revenue quarter of the year as incremental expense continues to build

- Expenses in 4Q likely to grow significantly thanks to new costs

- Brand transformation expenses

- Incremental pre-opening expenses for new units

- Beef prices post a risk to margins, particularly in 3Q

- Industry sales benchmarks continue to be sluggish

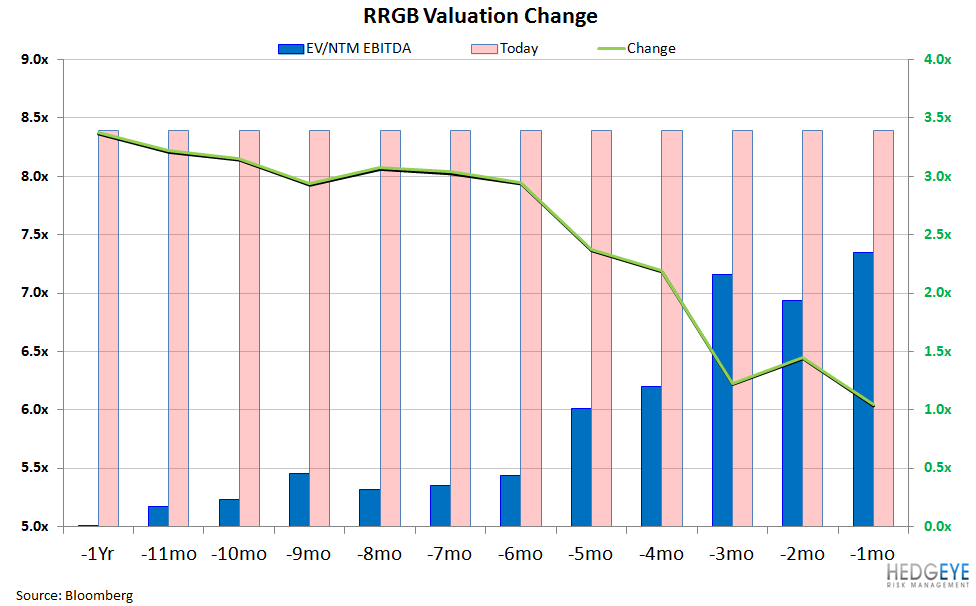

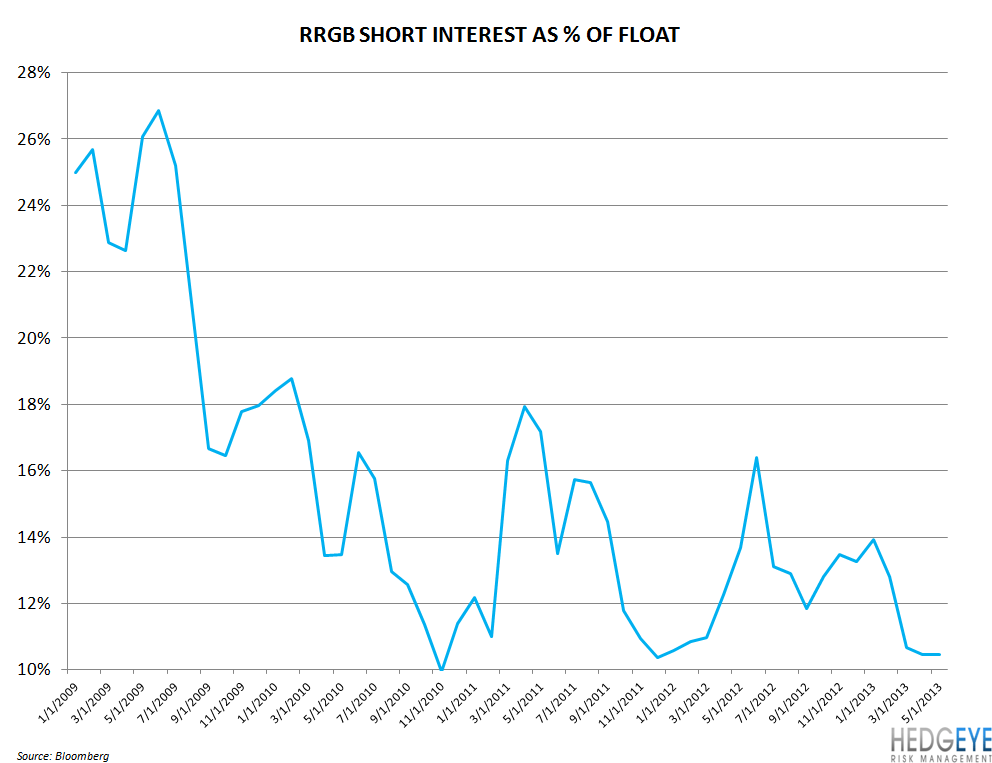

Valuation and Sentiment

Short interest in RRGB has been coming down since 2008 but remains the fourth highest in casual dining at 10.5%. The valuation that consensus is awarding the stock has risen sharply in recent months. The sell-side is fairly cautious on the name with 37.5% of analysts rating the stock a “buy”, 50% “hold”, and 12.5% “sell”.

Howard Penney

Managing Director

Rory Green

Senior Analyst