With this coupon Chili’s has effectively taken its $7 price point down to $4.50….. I’m having a hard time seeing how this can be good news! If the consumer was inspired by the $7 price point why would you need to provide further incentive!

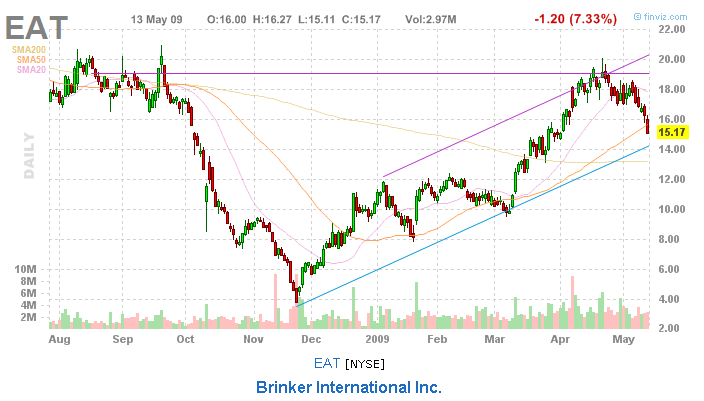

If you noticed yesterday Keith bought EAT for a TRADE. It’s consistent with his view of the Consumer Discretionary (XLY) and the market in general.

I continue to be cautious on the early cycle casual dining names!