Yesterday we highlighted the expedited back-up in mortgage rates as an emergent headwind to the sustainability of housing’s accelerating recovery. While higher rates do represent a drag on affordability, in the more immediate term, housing’s momentum is showing no signs of deceleration.

This morning’s Corelogic Home Price Index showed home prices accelerating to +12.14% Y/Y in April with the Preliminary May estimate reflecting further acceleration to 13.2% Y/Y. Moreover, the M/M Home Price changes observed in April and May represented the fastest rates of appreciation in the last 20 years, inclusive of the 2004-2006 bubble period. In short, the recovery in housing remains almost perfectly parabolic at present.

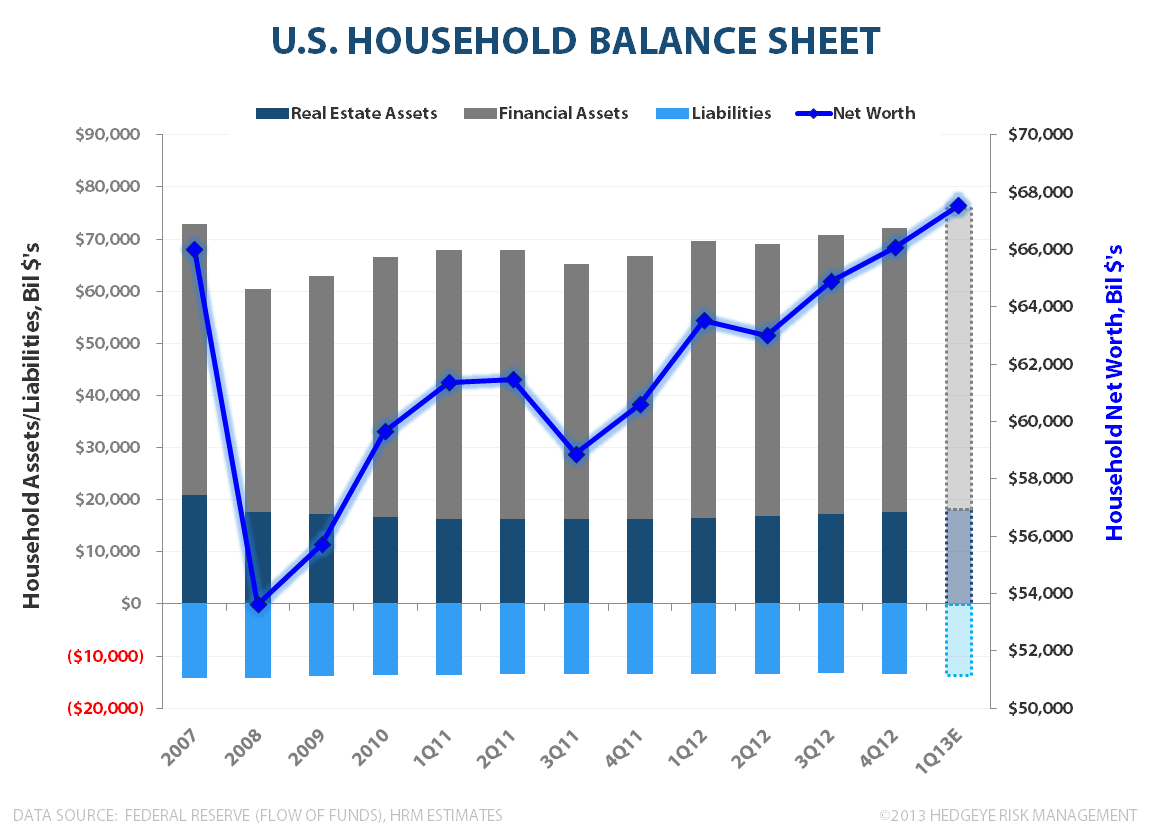

Relatedly, ongoing home and financial asset price re-flation continue to drive the Household balance sheet recovery and should serve to further support consumption as the wealth effect increasingly manifests (see Here for fuller discussion of housing’s wealth effect) alongside rising confidence and domestic labor market strength.

Collectively, Real estate and Equities (Corporate Equities & Mutual Fund shares), represented ~44% of Household assets as of 4Q12 and have appreciated ~10% and ~12% year-over-year in 1Q13, respectively. Given the magnitude of Q/Q and Y/Y real estate and financial asset appreciation, even under aggressive assumptions for growth in Household liabilities, the Fed’s Flow of Funds report scheduled for release on Thursday should reflect further acceleration and another new, nominal high, in Household Net Worth in 1Q13.

In addition to driving some manner of wealth effect, the strengthening of the Household balance sheet and rising net wealth are supportive of credit expansion, on the margin, as household capacity for credit increases alongside rising collateral values. A positive change in the flow of net new credit would provide an incremental tailwind to consumption growth as well.

We’ll follow up with any notable highlights from the Flow of Funds release on Thursday.

Christian B. Drake

Senior Analyst