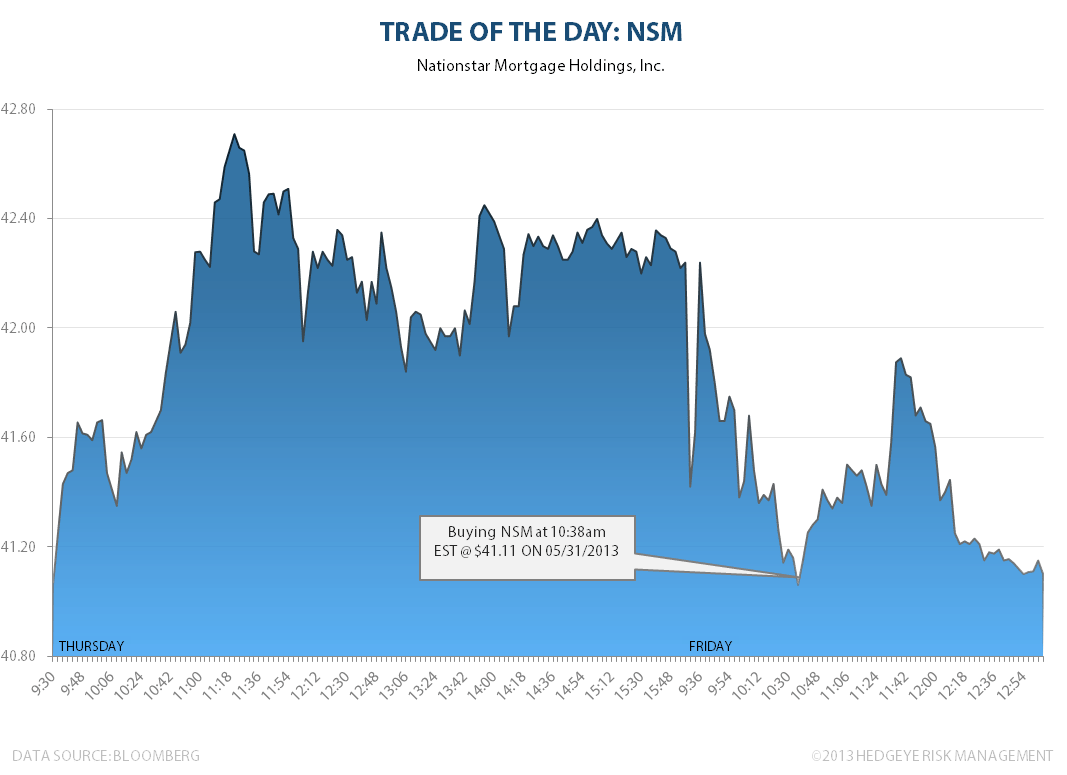

Buying back what we sold yesterday on green (a beauty +5% intraday rip). Hat tip to Hedgeye Jedi Financial Sector Head Josh Steiner. Steiner's bull case hasn't changed here. NSM’s price has. We’re just doing our best to risk manage the range of a high beta stock.