This note was originally published May 30, 2013 at 15:12 in Macro

With the TREND in the economic data continuing to confirm our Research and Risk Management views, the Hedgeye Redundancy Department has been at productive capacity since late November repeatedly highlighting the key factors at work supporting the ongoing improvement in the domestic growth outlook. We’ll keep it tight here in highlighting May’s macro manifestations of domestic #GrowthAccelerating.

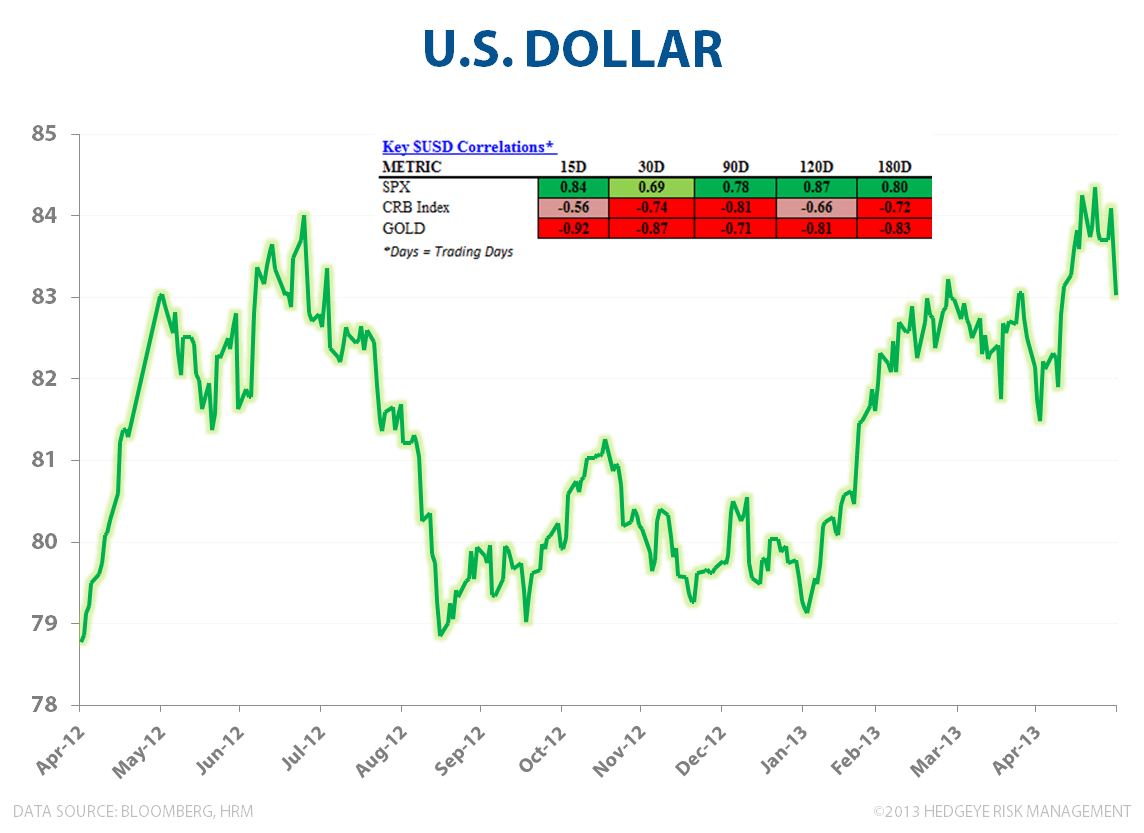

First, to be clear, we don’t like everything at every price but, on balance, with the $USD still in bullish formation (Bullish TRADE, TREND, TAIL), commodity deflation persisting, and Labor, Housing & Confidence (and to a lesser extent Credit and now Real Earnings) working reflexively, we continue to like the Dollar and domestic, consumption oriented equities on the long side and Gold, Yen, and the broader commodity basket on the short side.

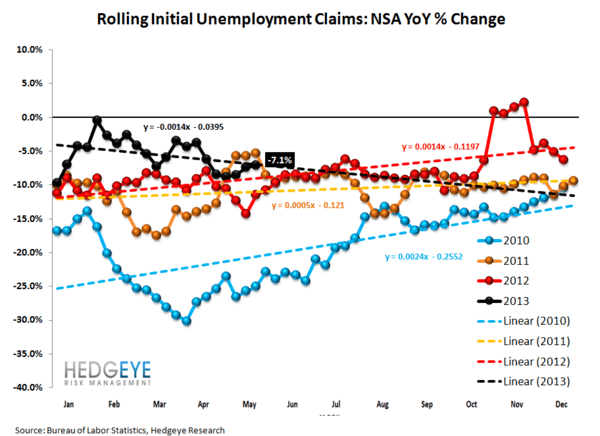

INITIAL CLAIMS: This morning’s Department of Labor data showed NSA claims accelerated to -8.3% y/y growth compared with -8.0% improvement the prior week and -2% two weeks prior. So, not only is the labor market improving, it is doing so at an accelerating rate at present. The organic improvement in the underlying labor market YTD has bucked the trend of the past three years, continuing to overwhelm the negative March-to-August seasonal distortion and any sequestration related drag.

Source: Hedgeye Financials

REAL EARNINGS: Mirroring the broader TREND in nearly every macro chart, real earnings growth troughed and inflected positively back in November. The Trend on both a 1Y and 2Y basis remains one of acceleration and with modest comps and persistent commodity deflation, expectations for sustained positive growth appear reasonable.

We would note that a continued rise in temp and part-time employment growth and corporate attempts to manage worker hours under the 30-hour threshold dictated under Obamacare is a trend we’re monitoring and one which, while positive for employment growth broadly, may serve as a drag to hours worked and weekly earnings growth as we move towards ACA implementation deadlines.

$USD/Commodities: The Dollar remains in bullish formation and with the domestic growth outlook improving on both an absolute and relative basis, deficit spending declining, and monetary policy more hawkish on the margin, we continue to think the dollar holds further upside.

With USD correlations to the SPX (+) and Gold/Commodities (-) remaining strong across durations, #StrongDollar, long stocks, short commodities remains the baseline macro strategy playbook. *Note: Keith bought the dollar via UUP this morning in our Real-time Alerts

CONFIDENCE: The Bloomberg Consumer Comfort Index, Univ. of Michigan Consumer Confidence, and the Conference Board Consumer Confidence Index all accelerated in May while making fresh 5Y highs. As we have highlighted, economic activity relationships with confidence have completely broken down over the last 4 years but, historically, consumer confidence has been a good-to-very good leading indicator for economic activity metrics such as new orders, consumer spending, and money velocity. A sustained breakout of the trough channel we have been in since 2008 may augur a re-tightening in historical confidence-econ correlations.

HOUSING: Purchase Applications continue to accelerate in 2q13TD despite the recent back-up in rates, the NAHB (Home Builder) HMI advanced in May, Existing Home Sales remain strong and the latest New Home Sales, Pending Home Sales and Home Price (FHFA & Case-Shiller) data all accelerated sequentially.

Admittedly, the comps on pricing continue to steepen and a significant, expedited back-up in rates may prove a marginal headwind but we continue to view the housing recovery as a multi-year story and wouldn’t view a move from the current low-double digit parabolic recovery to steady high-single digit HPA growth as a material negative.

Mortgage Application and Pending Home Sales data suggests forward housing activity will remain healthy and, over the next few years, we continue to believe a move towards 2M housing starts represents a high probability scenario.

Yield Spread (10’s-2’s): In so much as a widening in the yield spread = expectations for QE Taper = Improving Domestic Macro is a transitive relationship, the recent expansion in the yield spread would serve as positive confirmation of an improving domestic growth outlook. The positive price divergence from financials (+4%) MTD, negative divergence from Utilities (-8.7%) MTD and ongoing outperformance for Consumer Discretionary would seemingly concur as well.

Christian B. Drake

Senior Analyst