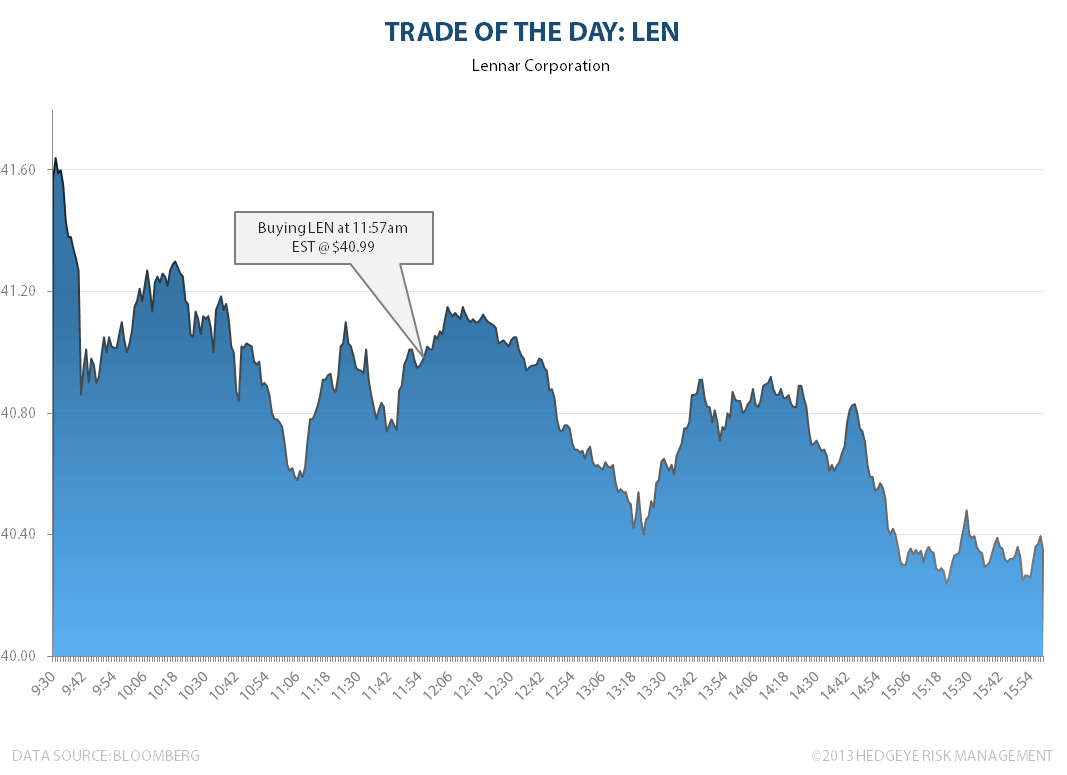

We’re buying back our #HousingsHammer view with this high short interest home-builder. LEN is signaling immediate-term TRADE oversold, within a bullish intermediate-term TREND.

Takeaway: We bought back Lennar (LEN) at 11:57am this morning at $40.99.

We’re buying back our #HousingsHammer view with this high short interest home-builder. LEN is signaling immediate-term TRADE oversold, within a bullish intermediate-term TREND.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.