(Excerpt from this morning's Hedgeye conference call)

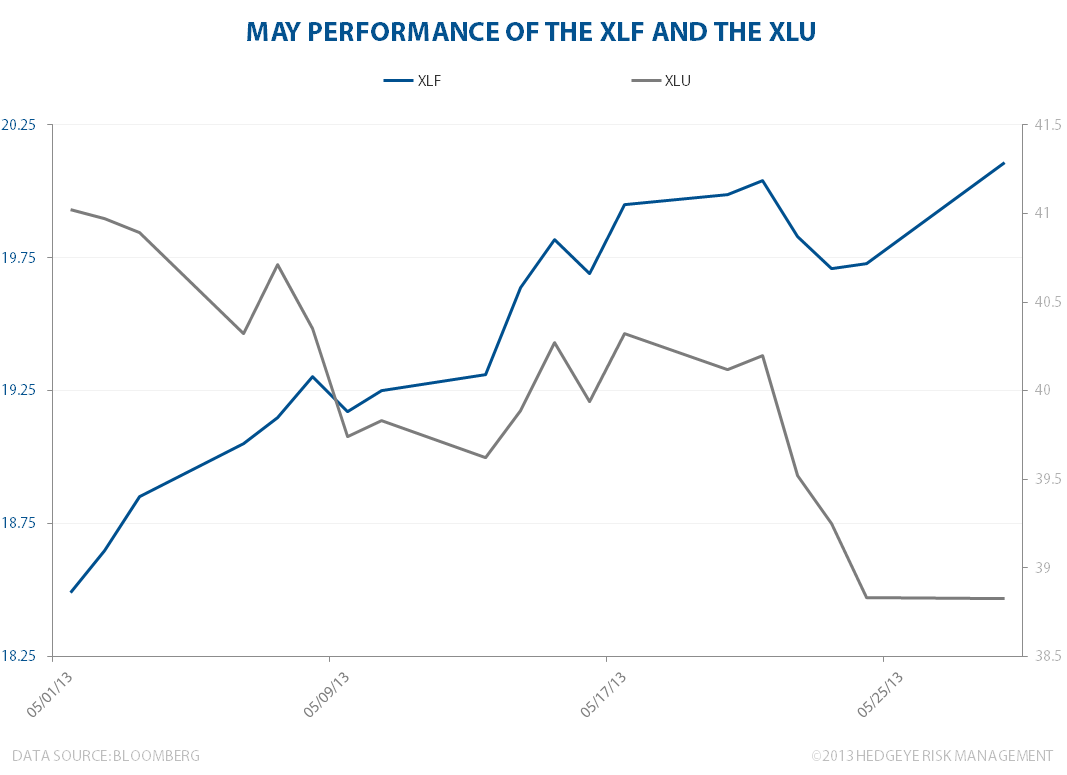

Just to show you how horrendous being long no-growth “yield” is performing, here’s the score:

- Utilities (XLU) are down -6.3% in May

- Financials (XLF) are leading the S&P 500 up +5.5% in May

That is a huge divergence.

So, why are utilities getting crushed, while financials (and US Treasury Yields) are ripping higher? Simple. Because one likes growth, and the other doesn’t like Bernanke.

The market is now – explicitly and implicitly – betting against the Chairman of the Federal Reserve. The bottom line here? Ben Bernanke is not bullish enough on growth.

#GrowthAccelerating