TODAY’S S&P 500 SET-UP – May 28, 2013

As we look at today's setup for the S&P 500, the range is 30 points or 0.46% downside to 1642 and 1.36% upside to 1672.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.79 from 1.76

- VIX closed at 13.99 1 day percent change of -0.57%

MACRO DATA POINTS (Bloomberg Estimates):

- 9am: S&P/CS Comp-20 City Home Price Index M/m, March, est 1%

- 9am: S&P/Case-Shiller Index, March (prior 146.57)

- 9am: S&P/Case-Shiller U.S. HPI Y/y, 1Q (prior 7.33%)

- 9am: S&P/Case-Shiller U.S. HPI, 1Q (prior 135.22)

- 10am: Richmond Fed Manuf Index, May, est -5 (prior -6)

- 10am: Consumer Confidence, May, est. 70.5 (prior 68.1)

- 10:30am: Dallas Fed Manuf Act., May, est -10 (prior -15.6)

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2043 sector

- 11:30am: U.S. to sell $30b 3M bills, $25b 6M bills

- 1pm: U.S. to sell $35b 2Y notes

- 8pm: Bank of Japan’s Kuroda speaks at BOJ conference

- U.S. Rates Weekly Agenda

GOVERNMENT:

- 10am: House Transportation and Infrastructure panel holds field hearing on oversight of high-speed rail in Calif.

WHAT TO WATCH

- Valeant to Buy Warburg Pincus’s Bausch & Lomb

- KKR, Silver Lake challenge Yahoo for Hulu as bidding escalates

- Yahoo’s Hulu bid said to be $600m-$800m: AllThingsD

- AstraZeneca to buy Omthera Pharma for up to $443m

- Apple’s iPhone distribution still examined by EU regulator

- Freeport mine suspension may be lifted after safety review

- Morgan Stanley said to move Asia hedge-fund event to U.S.

- Jet to buy more Boeing planes as AirAsia enters India market

- Siga may rise on chance to reargue damages in PharmAthene suit

- Chevron lends Venezuelan oil venture $2b for output boost

- Chevron plans to sell more gas from A$52b Gorgon project

- Clarion said to buy NYC tower in midtown south for $225m

- Li says China targets 7% annual growth this decade

- Oil-price manipulation may affect millions, EU official says

- “Fast & Furious 6” is top U.S./Canada film w/ $98.5m

- Bank of Israel lowers rate a second time this month

- U.S. Weekly Agendas: Finance, Industrials, Energy, Health, Consumer, Tech, Media/Ent, Real Estate, Transports

- North American M&A Agenda

- Canada Weekly Agendas: Energy, Mining

- U.S. consumer spending probably little changed: Eco Preview

- BOJ Speakers, Merkel, French Open: Week Ahead May 27-June 1

EARNINGS:

- Canadian Solar (CSIQ) 6am, ($0.78)

- Tiffany (TIF) 7am, $0.53

- Bank of Nova Scotia (BNS CN) 7:30am, C$1.26 - Preview

- United Natural Foods (UNFI) 4pm, $0.64

- EnerSys (ENS) 4:01pm, $0.80

- Guidewire Software (GWRE) 4:01pm, $0.02

- Wet Seal (WTSL) 4:05pm, $0.01

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Premiums Tumble From India to Hong Kong as Demand Wanes

- Refined Sugar Sours as Premium Shrinks Amid Glut: Commodities

- Corn Climbs to Three-Week High as Wet Weather May Slow Planting

- Brent Crude Rises to One-Week High; WTI Halts Four-Day Decline

- Gold Drops With Silver as Dollar Strengthens Before U.S. Data

- Money Managers Boost Bets on Higher Cocoa Prices on NYSE Liffe

- Aluminum Inventories Seen by IAI at 1.22 Million Tons in April

- Gold Futures May Drop to Lowest Since 2010: Technical Analysis

- SHFE Plans to Expand Warehouse Network in Competition With LME

- Rebar in Shanghai Climbs 0.2%, Reversing Earlier Decline

- Australia May Get 10% of New LNG Contracts, Wood Mackenzie Says

- Jet Fuel Sinks in Europe as Slowdown Hits Travel: Energy Markets

- LPG Tanker Rates Rising Near Record in U.S. Shale Surge: Freight

- Copper Swings Between Gains and Declines on China Growth Concern

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

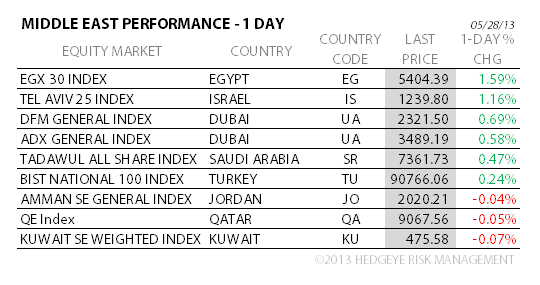

MIDDLE EAST

The Hedgeye Macro Team